Gambling for Redemption and Self-fulfilling Debt Crises

06 May 2019 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, economic history, Euro crisis, financial economics, global financial crisis (GFC), great depression, great recession, international economic law, International law, law and economics, macroeconomics, monetary economics, Public Choice, rentseeking Tags: banking panics, sovereign debt crises

Lucas on moral hazard and banking crises

15 Feb 2019 Leave a comment

in applied price theory, business cycles, economics of regulation, Euro crisis, global financial crisis (GFC), great depression, great recession, industrial organisation, law and economics, macroeconomics, monetary economics, Robert E. Lucas Tags: banking panics, moral hazard

Nobel Symposium Randall Kroszner Lessons from the global financial crisis, and crises past

24 Sep 2018 Leave a comment

in applied price theory, business cycles, economics of information, global financial crisis (GFC), great depression, great recession, law and economics, macroeconomics, monetary economics Tags: banking panics, deposit insurance, sovereign debt crises, sovereign defaults

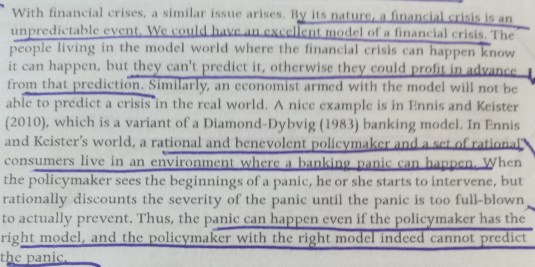

Stephen Williamson on how good economic models of financial crises can’t predict them

22 Sep 2018 Leave a comment

in applied price theory, business cycles, economics of information, economics of regulation, global financial crisis (GFC), great recession, macroeconomics, monetary economics Tags: banking panics

Deposit insurance

11 Apr 2016 Leave a comment

in applied price theory, business cycles, economic history, economics, economics of regulation, global financial crisis (GFC), macroeconomics, monetary economics, Public Choice, rentseeking Tags: bank runs, banking crises, banking panics, deposit insurance, Thomas Sargent

Many of the key issues about what modern macroeconomics has to say on global financial crises and deposit insurance are discussed in a 2010 interview with Thomas Sargent

Sargent said that two polar models of bank crises and what government lender-of-last-resort and deposit insurance do to arrest or promote them were used to understand the GFC. They are polar models because:

- in the Diamond-Dybvig and Bryant model of banking runs, deposit insurance and other bailouts are purely a good thing stopping panic-induced bank runs from ever starting; and

- in the Kareken and Wallace model, deposit insurance by governments and the lender-of-last-resort function of a central bank are purely a bad thing because moral hazard encourages risk taking unless there is regulation or there is proper surveillance and accurate risk-based pricing of the deposit insurance.

In the Diamond-Dybvig and Bryant model, if there is government-supplied deposit insurance, people do not initiate bank runs because they trust their deposits to be safe. There is no cost to the government for offering the deposit insurance because there are no bank runs! A major free lunch.

Tom Sargent considers that the Bryant-Diamond-Dybvig model has been very influential, in general, and among policy makers in 2008, in particular.

Governments saw Bryant-Diamond-Dybvig bank runs everywhere. The logic of this model persuaded many governments that if they could arrest the actual or potential runs by convincing creditors that their loans were insured, that could be done at little or no eventual cost to taxpayers.

In 2008, the Australian and New Zealand governments announced emergency bank deposit insurance guarantees. In Bryant-Diamond-Dybvig style bank panics, these guarantees ward off the bank run and thus should cost nothing fiscally because the deposit insurance is not called upon. These guarantees and lender of last resort function were seen as key stabilising measures. These guarantees were called upon in NZ to the tune of $2 billion.

- 1. The Diamond-Dybvig and Bryant model makes you sensitive to runs and optimistic about the ability of deposit insurance to cure them.

- The Kareken and Wallace model’s prediction is that if a government sets up deposit insurance and doesn’t regulate bank portfolios to prevent them from taking too much risk, the government is setting the stage for a financial crisis.

- The Kareken-Wallace model makes you very cautious about lender-of-last-resort facilities and very sensitive to the risk-taking activities of banks.

Kareken and Wallace called for much higher capital reserves for banks and more regulation to avoid future crises. This is not a new idea.

Sam Peltzman in the mid-1960s found that U.S. banks in the 1930s halved their capital ratios after the introduction of federal deposit insurance. FDR was initially opposed to deposit insurance because it would encourage greater risk taking by banks.

Late on Friday afternoon, Stuff posted an op-ed piece calling for the introduction of a (funded) deposit insurance scheme in New Zealand. It was written by Geof Mortlock, a former colleague of mine at the Reserve Bank, who has spent most of his career on banking risk issues, including having been heavily involved in the handling of the failure, and resulting statutory management, of DFC.

As the IMF recently reported, all European countries (advanced or emerging) and all advanced economies have deposit insurance, with the exception of San Marino, Israel and New Zealand. An increasing number of people have been calling for our politicians to rethink New Zealand’s stance in opposition to deposit insurance. I wrote about the issue myself just a couple of months ago, in response to some new material from the Reserve Bank which continues to oppose deposit insurance.

Different people emphasise different arguments in making the case for New Zealand to…

View original post 1,963 more words

Banking crises are more common than you think

16 Nov 2015 Leave a comment

in currency unions, economic history, economics of regulation, Euro crisis, macroeconomics, monetary economics Tags: bank run, banking crises, banking panics, economics of banking, financial crises

How frequent are simultaneous financial crises in one country?

04 Sep 2015 Leave a comment

in business cycles, currency unions, development economics, economic growth, economic history, Euro crisis, financial economics, global financial crisis (GFC), great depression, great recession, growth disasters, growth miracles, law and economics, macroeconomics, monetary economics, property rights Tags: bank runs, banking crises, banking panics, currency crises, current account crises, debt crises, pseudo financial crises, real financial crises, sovereign debt crises, sovereign default

John Cochrane on a big hole in the Greek bailout (and media analysis of the bailout)

15 Jul 2015 Leave a comment

in currency unions, Euro crisis, global financial crisis (GFC), great recession, macroeconomics, monetary economics Tags: bank runs, banking panics, Greece, John Cochrane, lender of last resort, sovereign bailouts, sovereign default

An average of 41% of Greek bank assets are non-performing, with loan repayments 90 days overdue or more (Barclays). http://t.co/HfXV8uapkj—

Mike Bird (@Birdyword) July 13, 2015

Real and Pseudo-Financial Crises, the Chinese share market crash and Anna Schwartz

09 Jul 2015 Leave a comment

in economic history, financial economics, fiscal policy, international economics, macroeconomics, monetarism, monetary economics Tags: Anna Schwartz, bank runs, banking panics, China, contagion, evidence-based policy, financial crises, financial stability, inflation targeting, international systemic risk, Michael Bordo, monetary history, pseudo financial crises, pseudo international systemic risk

If we could take time out from the breathless journalism about the Chinese stock market, which some people may have heard of before this week, it’s crash should be seen through the lens that Anna Schwartz developed in 1987 of a pseudo financial crisis and a financial crisis.

This is why so many Chinese companies are suspended bloom.bg/1UA7TbA http://t.co/5awEt6B23u—

Bloomberg Business (@business) July 08, 2015

Her paper is written at the same time as the 1987 stock market crash. On financial crises, Anna Schwartz said:

As for those pseudo financial crises, she said:

Schwartz’s principal concern with regard to pseudo financial crisis was:

proposals to deal with pseudo-financial crises is the perpetuation of policies that promote inflation and waste of economic resources

As we are talking about the Chinese stock market, Anna Schwartz also wrote about the concepts of real systemic international risk and and pseudo international systemic risk.

Once again, and as with pseudo financial crises and real financial crises, what distinguishes real systemic international risk and pseudo international systemic risk is a threat to the payment system. The threat of bank runs, which can easily be eliminated through lender of last resort facilities:

As always it is about the security of the payments system – of avoiding bank runs, not private losses:

The lesson for the day is that when people start panicking about the economy or the stock market or international markets, don’t go to a macroeconomist for advice, go to a monetary historian. They have seen it all before.

The reason why New Zealand should rule out helping Greece!

06 Jul 2015 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), macroeconomics Tags: bank runs, banking panics, Eurosclerosis, Germany, Greece, sovereign defaults

Greece is a tiny part of the European economies so it doesn’t matter that much to the rest of the European Union what happens to Greece. The only people will notice the sovereign default of Greece once the breathless journalism has died down are Greeks themselves as they rebuild their banking and monetary system against a background of a government run by coffee shop Marxists.

Recent Comments