Thomas Sargent, “Estados Unidos antes, Europa ahora”

08 Oct 2021 Leave a comment

in budget deficits, business cycles, economic history, financial economics, fiscal policy, George Stigler, global financial crisis (GFC), great depression, great recession, history of economic thought, macroeconomics, monetarism, monetary economics Tags: monetary policy, sovereign defaults

Thomas Sargent 2013 MACROECONOMIC THEORY AND THE CRISIS

01 May 2020 Leave a comment

in budget deficits, business cycles, economic growth, economic history, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, Milton Friedman, monetarism, monetary economics, Robert E. Lucas Tags: sovereign debt crises, sovereign defaults

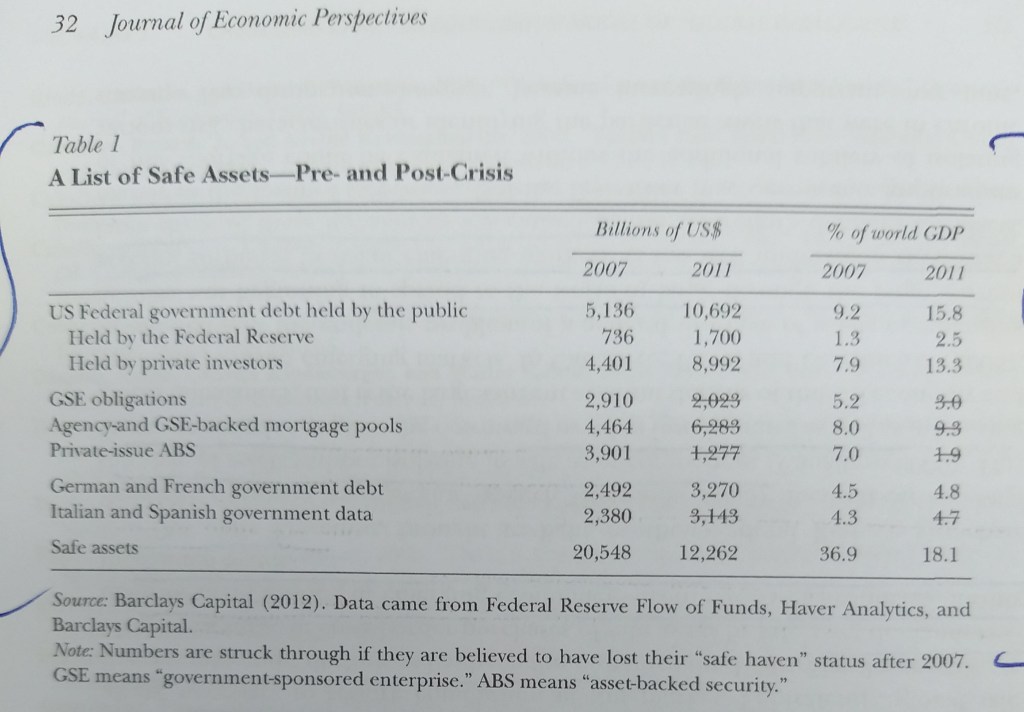

Caballero on the great safe collateral contraction

27 Feb 2020 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, economic history, entrepreneurship, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great recession, international economics, law and economics, macroeconomics, monetary economics, property rights, Public Choice Tags: adverse selection, asymmetric information, monetary policy, moral hazard, self-selection, sovereign debt crises, sovereign defaults

Nobel Symposium Randall Kroszner Lessons from the global financial crisis, and crises past

19 Feb 2020 Leave a comment

in budget deficits, business cycles, economic growth, economic history, economics of information, economics of regulation, Euro crisis, financial economics, global financial crisis (GFC), great depression, great recession, law and economics, macroeconomics, monetary economics, property rights, Public Choice, public economics Tags: sovereign defaults

Nobel Symposium Kenneth Rogoff Indebtedness of governments, firms, and households

09 Feb 2020 Leave a comment

in budget deficits, business cycles, economic growth, economic history, economics of information, financial economics, global financial crisis (GFC), great recession, macroeconomics, monetary economics, Public Choice, public economics Tags: sovereign debt crises, sovereign defaults

Where the real seigniorage is

30 Jan 2020 Leave a comment

in budget deficits, business cycles, economic growth, economics of information, financial economics, fiscal policy, macroeconomics, monetary economics Tags: monetary policy, sovereign defaults

Only rational expectations macroeconomics can explain self-fulfilling crises

01 Nov 2019 Leave a comment

in applied price theory, budget deficits, business cycles, currency unions, economic growth, economic history, economics of bureaucracy, economics of information, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, monetary economics, Public Choice Tags: Euroland, rational expectations, sovereign defaults

Thomas J. Sargent speaks on Euro Crisis

18 May 2019 Leave a comment

in applied price theory, budget deficits, business cycles, currency unions, economic growth, economic history, economics of bureaucracy, economics of information, economics of regulation, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great recession, history of economic thought, international economics, International law, law and economics, macroeconomics, monetary economics, property rights, Public Choice, public economics, rentseeking Tags: moral hazard, sovereign debt crises, sovereign defaults, Thomas Sargent

Thomas Sargent Emergency Economic Summit for Greece: Part 2

18 May 2019 Leave a comment

in applied price theory, budget deficits, business cycles, comparative institutional analysis, constitutional political economy, currency unions, economic growth, economic history, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, income redistribution, law and economics, macroeconomics, monetary economics, politics - USA, property rights, Public Choice, public economics, rentseeking Tags: sovereign defaults, Thomas Sargent

Jonn Cochrane Says Allowing European Defaults `Best’ for Euro

04 Oct 2018 Leave a comment

in budget deficits, business cycles, currency unions, Euro crisis, financial economics, law and economics, macroeconomics, monetary economics, property rights Tags: sovereign defaults

Nobel Symposium Randall Kroszner Lessons from the global financial crisis, and crises past

24 Sep 2018 Leave a comment

in applied price theory, business cycles, economics of information, global financial crisis (GFC), great depression, great recession, law and economics, macroeconomics, monetary economics Tags: banking panics, deposit insurance, sovereign debt crises, sovereign defaults

General government net financial liabilities as % Portuguese, Italian, Greek, Spanish and Irish GDPs

03 Jun 2016 Leave a comment

in budget deficits, business cycles, economic growth, economic history, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), macroeconomics Tags: Greece, Ireland, Italy, Portugal, public debt management, sovereign debt crises, sovereign defaults, Spain

I had borrowed a lot of money from scratch after 2007. Greece borrowed a lot of money of its own accord from 2010. Italy always owed a lot of money. Spanish do not know all that much money considering their dire financial circumstances.

Source: OECD Economic Outlook June 2016 Data extracted on 01 Jun 2016 12:57 UTC (GMT) from OECD.Stat

Greece should have defaulted several years ago rather than have raised taxes

24 Feb 2016 Leave a comment

in currency unions, economic growth, Euro crisis, fiscal policy, macroeconomics Tags: Greece, sovereign debt, sovereign defaults

John Cochrane is the latest to join the list of economists who pointed out that Greece should have defaulted several years ago rather than put up taxes. Tax rises just made everything worse and put off the day when Greece had to reform through deregulation and privatisation.

Source: Renowned U.S. Economist Says High Taxes Squash Greece’s Prospects for Recovery | GreekReporter.com.

As early as 2011 , Jeffrey Miron was arguing the best way forward for Greece was to default and leave the Euro:

If Greece defaults, the country gets immediate relief from the crushing interest payments on its debt, leaving it with a relatively modest primary deficit which excludes the big interest payments Greece is faced with now.

In such a scenario, the pressure for austerity would therefore diminish. This would allow Greece to choose policies that encourage growth, rather than ones that shrink the deficit but retard growth by imposing higher taxes.

By abandoning the euro and adopting a properly valued currency, Greece can restore its international competitiveness. This means greater employment demand from both domestic and foreign sources.

The potential negative of default is that Greece will likely lose access, for a while, to international credit markets (although it will be a much safer investment after default than it is now).

But being cut off from foreign lending for a few years is not a disaster; if anything, it might encourage cuts in the wasteful components of government spending.

A bigger risk of default is that ending the crisis might reduce pressure for Greece to address the economy’s fundamental problems: crony capitalism, a Byzantine tax code, excessive regulation, and a bloated government sector.

If Greece fails to reform, it will suffer slow growth and a new crisis soon, regardless of what it does now.

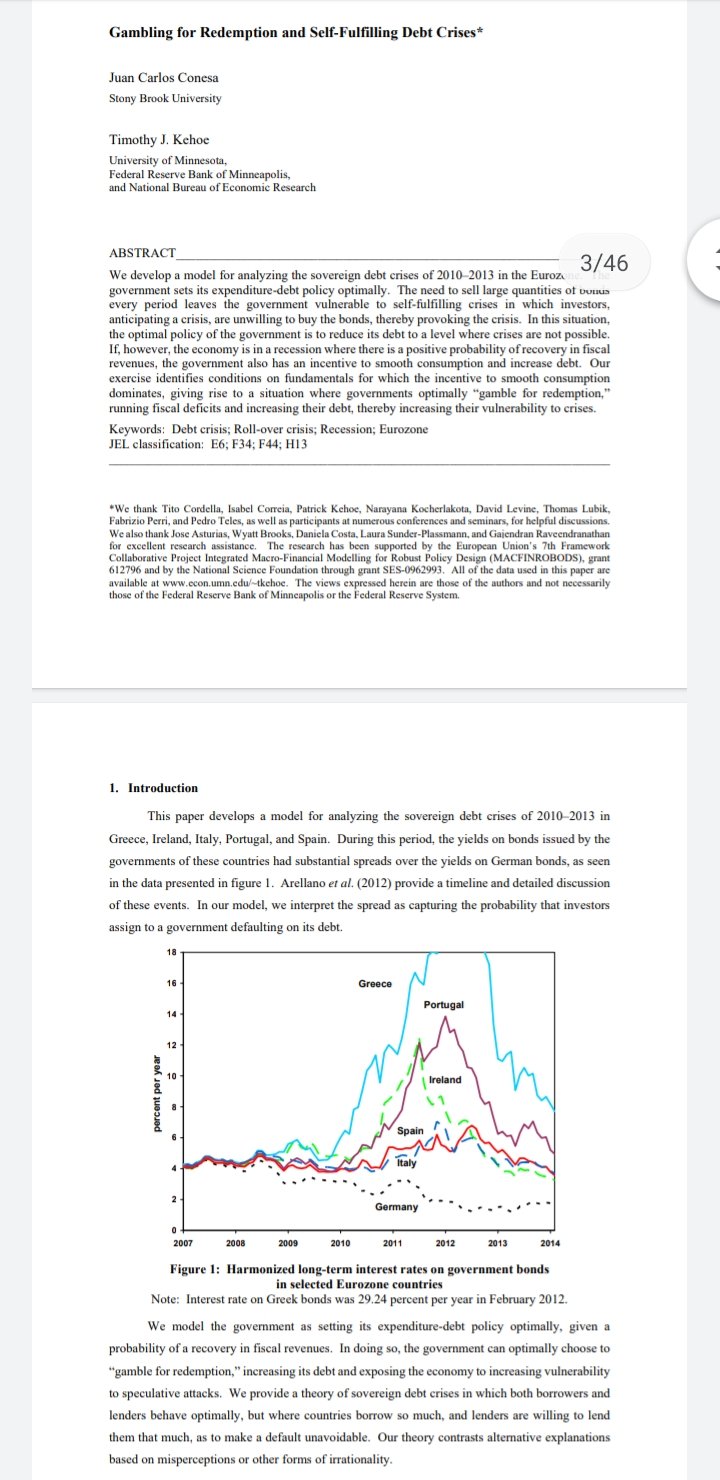

Arellano, Conesa, and Kehoe explained in Chronic Sovereign Debt Crises in the Eurozone, 2010–2012 that the post-GFC recession in many Eurozone countries created an incentive to gamble for redemption. This gamble for redemption is betting that the post-2008 recession will soon end:

- If Greece sold more bonds to smooth government spending in the interim, and if the Greek and EU economies recover, the stronger revenue growth will pay off the enlarged Greek government debt.

- Under some circumstances, this policy is the best that a government can do for its country, but it carries a risk!

- If the recession goes on for too long (and it did in southern Eurozone), a government will either have to stop increasing its debt or default on its bonds.

The global bond markets will anticipate this prospect of default as a country’s government debt accumulates and will seek higher and higher interest for new bonds, and importantly, to roll over existing Greek Government bonds.

EU policies that result in lower interest rates and lower the cost of a sovereign default provide incentives for a government to gamble for redemption. The interventions taken to date by the EU and the IMF – lowering the cost of borrowing and reducing default penalties, the bailouts and the 50% write-off of the existing Greek government debts – encourage southern Eurozone governments to gamble for redemption.

Through history, sovereign defaults come in clusters. Is Greece the start of one? on.wsj.com/1V3XkxR via @WSJ http://t.co/Oy9aMPoHrt—

Greg Ip (@greg_ip) July 15, 2015

Greece and a few others are gambling for redemption by betting that the recession will end soon, selling more bonds to smooth government spending in the interim, and reducing the enlarged debt if their economies recover. The Greeks initially did a fine job in squeezing huge subsidies and debt write-offs!

If the recession continues for too long, the government will have to stop increasing debt or default on its bonds. Greece has been in default in more than 50% of the time since it became independent in 1822.

Greece’s problem is that it is 119th in the 2014 index of economic freedom, just ahead of India. The World Bank ranks Greece 161st in the world for ease of registering property and 91st for enforcing contracts; it takes an average of 1,300 days to enforce a contract through the Greek courts. This low base says something about how Greek politics works and will work for some time to come.

Cristina Arellano in a recent paper pointed out that if default is inevitable, raising taxes just makes everything worse:

Fiscal defaults occur because of the government’s inability to raise tax revenues. Aggregate defaults occur even if the government could raise tax revenues; debt is simply too high to be sustainable.

In a quantitative exercise calibrated to Greece, we find that our model can predict the recent default, but that increasing taxes would not have prevented it. In fact, increasing taxes would have made the recession deeper because of the distortionary effects of taxation.

Share market losses during previous financial crises in the USA and UK

31 Jan 2016 Leave a comment

in business cycles, economic history, fisheries economics, global financial crisis (GFC), great depression, great recession, macroeconomics Tags: banking crises, financial crises, sovereign debt crises, sovereign defaults

Recent Comments