Baby Busts and Bank Crashes: A Conversation with Demographer Nicholas Eb…

20 Aug 2023 Leave a comment

in applied price theory, economic history, financial economics, industrial organisation, international economics, macroeconomics, monetary economics, population economics Tags: baby bust, economics of banking

Charles Calomiris-“Thinking Historically about Banking Crises and Bailouts”

16 Aug 2023 Leave a comment

in business cycles, economic history, macroeconomics, monetary economics Tags: economics of banking

Does Fractional Reserve Banking Endanger the Economy? A Debate

23 May 2020 Leave a comment

in business cycles, financial economics, law and economics, macroeconomics, monetary economics, property rights Tags: economics of banking, monetary policy

The Destabilizing Consequences of Central Banking

27 Apr 2020 Leave a comment

in Austrian economics, business cycles, economic history, financial economics, macroeconomics, monetary economics Tags: economics of banking, free banking, monetary policy

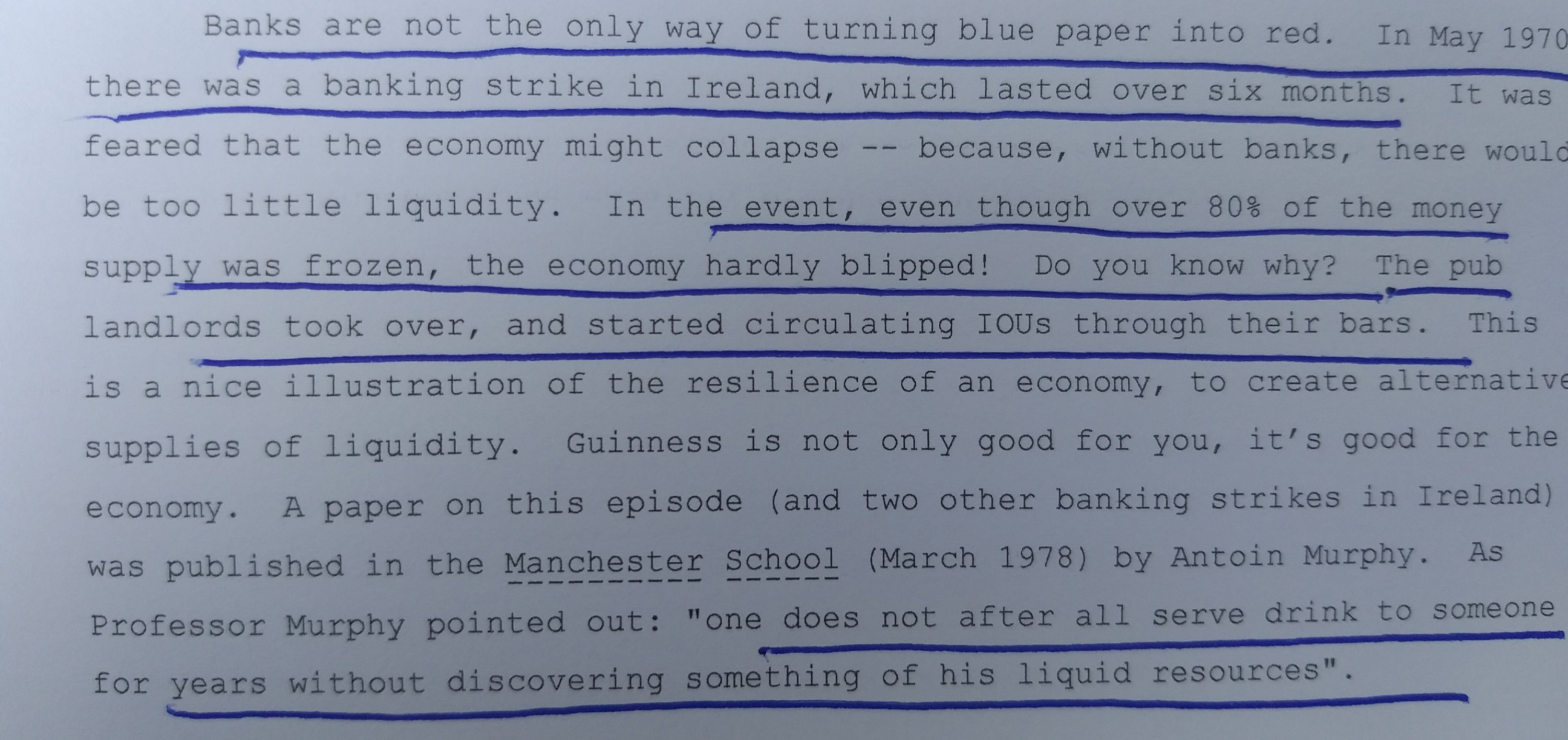

Ireland’s worst bank strike lasted 6-months

20 Mar 2020 Leave a comment

in economic history, financial economics, labour economics, labour supply, macroeconomics, monetary economics, unions Tags: economics of banking, union power

Does Fractional Reserve Banking Endanger the Economy? A Debate

02 Mar 2020 Leave a comment

in applied price theory, Austrian economics, business cycles, comparative institutional analysis, economic history, economics of information, economics of regulation, law and economics, macroeconomics, monetary economics, property rights Tags: economics of banking, monetary policy

Can banks create money at will?

28 Feb 2020 Leave a comment

in applied price theory, business cycles, economics of bureaucracy, economics of crime, financial economics, law and economics, macroeconomics, managerial economics, monetary economics, organisational economics, property rights, Public Choice Tags: economics of banking

Champ and Freeman on banks printing money

28 Feb 2020 Leave a comment

in economics of crime, financial economics, law and economics, macroeconomics, monetary economics, property rights Tags: economics of banking, monetary policy

Is Kiwibank profitable enough to take on the big banks?

09 Apr 2016 Leave a comment

in applied price theory, economic history, entrepreneurship, financial economics, George Stigler, industrial organisation, law and economics, politics - New Zealand, survivor principle Tags: anti-trust economics, antimarket bias, competition law, economics of banking, New Zealand Greens

if Kiwibank is part of the competitive fringe of an oligopoly made up of the 4 Australian banks, it is not very profitable for a competitive fringe of a cartel as the chart below shows. The other New Zealand owned small banks in that competitive fringe are not that profitable at all. Undercutting an oligopoly and its high prices and above-average cost and above marginal cost pricing is not what it used to be for the competitive fringe in New Zealand banking, if there ever was a cartel.

Source: G1 Summary information for locally incorporated banks – Reserve Bank of New Zealand.

Bank customers can choose between four major banks and a competitive fringe. If those major banks are indeed overcharging because of price-fixing by a cartel or an oligopoly, that competitive fringe which includes Kiwibank has a real opportunity to expand profitably and with little risk.

The prospect of expansion by the competitive fringe that includes Kiwibank only increases the incentives on each of the four big banks to cheat on the cartel price. The first bank to cheat on the cartel will profit the most; the other banks who are colluding know this. As George Stigler concluded in his 1964 paper “The Theory of Oligopoly” as Peltzman and Carlton explain:

…once a price is somehow agreed upon, there will be incentives for individual rivals to cheat on the [collusive] agreement. Whether cheating occurs depends on weighing the profits from not cheating against the profits from cheating and then being detected and having competition break out…

any agreement among sellers cannot ignore the incentives to cheat provided by lags in detection. So understanding when a price elevated above the competitive level can be an equilibrium requires an analysis of the dynamic consequences of cheating versus not cheating…

Collusion over retail banking services and prices faces major hurdles that will lead to most attempts at price-fixing having a short life. These barriers to successful collusion include:

- numerous competitors,

- expansion by the smaller banks were not part of the cartel or cheat on the cartel

- the entry and expansion of new banks,

- the lack of a standard product, and

- a rapidly changing business environment.

Implicit understandings among the colluding banks may break down owing to conflicts over the most suitable price, the complexities of co-ordinating pricing across a diverse range of banking products, or the simple presence of a maverick bank.

As time passes, destabilising pressures within a banking cartel or oligopoly will build due to long-run substitution and the threat or actuality of entry by new banks and expansion by banks In the competitive fringe, which includes Kiwibank.

The first firm in any market may charge a high price relative to costs, but the entry of one or two more firms usually results in effective competition. Once there are three to five suppliers in a market, an additional entrant has little impact on prices because pricing is already as competitive as it can be.

When ANZ sought to acquire the National Bank of New Zealand in 2003, the Commerce Commission did not oppose this merger. The Commission did not consider that a substantial lessening of competition would follow this merger. The Commission said:

…the merger is unlikely to increase the likelihood of co-ordinated market power in the supply of transaction accounts because the fringe players are likely to provide some competition, the banks have different strengths and weaknesses and in particular ASB is unlikely to have the incentive to participate in co-ordinated power at the expense of its recent growth and customer satisfaction levels.

This analysis of co-ordinated market power applies to each of the relevant markets. Therefore the Commission concludes that the merger is unlikely to result in a substantial lessening of competition in the supply of transaction accounts.

In the supply of mortgages, savings accounts and credit cards the merger is unlikely to lead to a substantial lessening of competition, as in each of these markets, ASB, Westpac and BNZ are likely to provide sufficient competition to the combined entity.

An important driver of a competition in the mortgage market in 2003 was a high incidence of fixed-rate mortgages and the tendency of these fixed rate mortgagees to reconsider all their options at the end of each fixed rate term.

The Commission Commission noted that there was a large re-mortgaging market in New Zealand. Banks offer to do all the work for customers wishing to switch over bank accounts and direct debit arrangements.

In a very atypical move for a purported cartel, in 2010 the bank owned Payments New Zealand agreed to change over direct debits over automatically when a customer switched banks, which made switching banks even more easier.

At the time of the ANZ and National Bank merger, the Commerce Commission noted that Kiwibank was offering lower rates on its mortgages as a way of gaining a foothold in the market.

The Commerce Commission could not have been more right about the vigour in competition in retail banking with regard to re-mortgaging and switching between fixed and floating mortgages in New Zealand.

As the chart below of fixed and floating mortgage shares a New Zealand bank balance sheets shows, there is a rapid exodus from fixed rate mortgages at the time of the Global Financial Crisis.

Source: S8 Banks: Mortgage lending ($m) – Reserve Bank of New Zealand.

I cannot see how any cartel or oligopoly could sustain price-fixing against such dynamic changes in market shares and product switching.

Cartels are is much more difficult to agree when there are many products about which to fix prices and market shares. At a minimum, this rapid movement of customers between mortgage products will sow suspicions that one or more rival banks is stealing customers thereby cheating on the cartel agreement. Not surprisingly, the history of cartels is a history of double-crossing. Banking is no exception.

@GarethMP @jamespeshaw need message discipline on @NZGreens as honest brokers

08 Apr 2016 Leave a comment

in economics of media and culture, industrial organisation, politics - New Zealand, survivor principle Tags: anti-trust economics, cartel theory, competition law, conspiracy theories, economics of banking, New Zealand Greens, privatisation, state owned enterprises

Yesterday morning, Green MP Gareth Hughes posted a British Greens’ video about how other politicians are a bunch of squabbling children but the Greens are above that. It’s only the Greens who offer a “true alternative to the establishment parties” and their “same childish Punch & Judy politics”.

Later that same day Greens co-leader James Shaw posted a video that shaded the truth about the history of dividends from Kiwibank as a way of scoring points of the National Party led government.

Shaw claimed that the government is extracting more and more dividends from Kiwibank rather than letting it keep those profits as capital on which the government owned bank can be a more aggressive competitor.

Source: Kiwibank pays its first dividend of $21 million to Government | Stuff.co.nz.

Shaw is vaguely correct in that it is dividends plural when referring to Kiwibank’s dividends. Kiwibank paid dividends of $21 million last year; and $750,000 the year before. Kiwibank has paid two dividends to New Zealand Post in its entire history since 2002.

It shades the truth to say that the government is extracting more and more dividends from Kiwibank when when it has only paid one dividend worth mentioning, which was last year.

Source: New Zealand Treasury – data released under the Official Information Act.

As for James Shaw’s claim that the entry of Kiwibank made banking in New Zealand much more competitive, Michael Reddell disposed of that by linking to a 2013 Treasury assessment of competition in retail banking.

Source: New Zealand Treasury Official Information Act Releases.

There are no excess profits in the New Zealand banking market for Kiwibank to undercut. Entry barriers are low, banking products are easy substitutes for each other between the competing banks, and the banks compete for market share by advertising of, for example, special packages to switch banks.

Adding to the analysis of the Treasury, Posner and Easterbrook suggest that these industry behaviours together are suspicious.

- Fixed relative market shares among top firms over time.

- Declining absolute market shares of the industry leaders.

- Persistent price discrimination.

- Certain types of exchanges of price information.

- Regional price variations.

- Identical sealed bids for tenders.

- Price, output, and capacity changes at the time of the suspected initiation of collusion.

- Industry-wide resale price maintenance or non-price vertical restraints.

- Relatively infrequent price changes; smaller price reactions as a result of known cost changes.

- Demand is highly responsive to price changes at market price.

- Level and pattern of profits relatively favourable to smaller firms.

- Particular pricing and marketing strategies.

As the Treasury noted in its analysis, there are several small banks offering competitive rates that would allow them to expand if they offered value for money over the existing offerings. Returns on equity of the big banks are not discernibly higher than for the smaller ones.

To add again to the Treasury analysis, it is not easy to organize a cartel. There are markets to divide, prices to set, and production quotas to assign. The best place to be in a cartel is outside of it undercutting the higher price and selling as much as you can before the cartel inevitably collapses. Brozen and Posner suggest the following pre-conditions to collusion:

- market concentration on the supply side;

- no fringe of small sellers;

- high transport costs from neighbouring markets;

- small variations in production costs between firms;

- readily available information on prices;

- inelastic demand at the competitive price;

- low pre-collusion industry profits;

- long lags on new entry;

- many buyers (otherwise selective discounting to big buyers will be too tempting while monitoring adherence to the agreement will be difficult);

- no significant product differentiation;

- large suppliers selling at the same level in the distribution chain;

- a simple price, credit and distribution structure;

- price competition is more important than other forms of competition;

- demand is static or declining over time; and

- stagnant technological innovation and product redesign.

Stable collusive arrangements are thus likely to be rare because the absence of any of the above conditions will tend to undermine the potential for successful collusion.

Successful cartel operation is even harder than its initial formation. Members of the cartel must continue to believe that they enjoy net profits from participating in the collusion.

The more profitable the collusive price fixing, the greater the incentive for outsiders to seek entry to compete. In cartel theory, these new entrants are known as interlopers.

The more numerous the participants in the cartel and the more lucrative the collusion, the greater the temptation for individual members to cheat and the greater the fear of each that some other member will cheat first.

Cartel members that cheat early profit the most from the cartel price before it collapses. That is why the history of cartels is a history of double-crossing. Long-term survival of the cartel has two fundamental requirements:

- cheating by a member on the cartel prices, outputs and market shares must be detectable; and

-

detected cheating must be adequately punishable without breaking-up of the cartel.

If banking was a cartel, you would not see advertising on the TV every night inducing customers to switch but you do. That advertising is cheating on the banking cartel the New Zealand Greens want to break up.

There is an infallible rule in competition law enforcement. It arises mostly crisply in merger law enforcement. If competitors oppose a merger, the merger must be pro-consumer. If the merger is anti-competitive, that merger will increase prices. The competing firms can follow those prices up and profit from the weakening of competition subsequent to the merger.

Will @JulieAnneGenter’s KiwiBank plan bankrupt KiwiPost? @JordNZ

03 Apr 2016 Leave a comment

in financial economics, industrial organisation, politics - New Zealand, privatisation, survivor principle Tags: economics of banking, government ownership, KiwiBank, New Zealand Greens, offsetting behaviour, rational irrationality, state owned enterprises, The fatal conceit

The Greens are followed up on an earlier suggestion by Julie Anne Genter, the Green’s Shadow Minister of Finance, that KiwiBank should be refocused to keeping interest rates low. To that end, it would not be required to pay dividends to the government to help fund the effort. KiwiBank has only just started paying dividends to its parent, KiwiPost.

If that were to be the case, that KiwiBank was no longer be required to pay dividends, that would blow quite a hole in the balance sheet of its parent company KiwiPost.

KiwiPost owns the share capital of KiwiBank, which must be valued on a commercial basis to pass auditing as a state owned enterprise which is commercially orientated.

Source: Historic $21 million dividend paid by state owned bank Kiwibank | interest.co.nz.

That share capital owned by KiwiPost in KiwiBank would be have to be written off if KiwiBank were to pay no further dividends because it is no longer commercially orientated entity. Such a write-off of its investment in KiwiBank would write off most of Kiwi Post’s equity capital.

The reason why state owned enterprises are required to be valued on commercial principles is to ensure that any subsidies or other favours sought by politicians show up in the profit and loss statement or the balance sheet through asset write-offs. Section 7 of the State-Owned Enterprises Act 1986 non-commercial activities states that:

Where the Crown wishes a State enterprise to provide goods or services to any persons, the Crown and the State enterprise shall enter into an agreement under which the State enterprise will provide the goods or services in return for the payment by the Crown of the whole or part of the price thereof.

This statutory safeguard ensures that the cost of any policies proposed by ministers, and the Greens are very keen on transparency and independent costing of political promises, are plain to all.

@NZGreens expand KiwiBank into wrong market to cut mortgage rates @JulieAnneGenter

03 Apr 2016 1 Comment

in industrial organisation, monetary economics, politics - New Zealand, survivor principle Tags: economics of banking, government ownership, KiwiBank, New Zealand Greens, offsetting behaviour, privatisation, rational irrationality, state owned enterprises, The fatal conceit

The Greens want to cut mortgage rates by having KiwiBank expand in business lending. Wrong market.

This expansion into a market that is not the mortgage market is to be underwritten by a capital injection as the Greens explain:

- Inject a further $100 million of capital in KiwiBank to speed its expansion into commercial banking;

- Allow KiwiBank to keep more of its profits to help it grow faster; and,

- Give KiwiBank a clear public purpose to lead the market in passing on interest rate cuts.

Note well that the $100 million capital injection is to expand in to commercial banking. More aggressive passing on of interest rate cuts may jeopardise credit ratings if this lowers the profitability of KiwiBank. KiwiBank has an A- rating

The bigger hole in the policy is the more aggressive mortgage rate setting by KiwiBank will be done by keeping more of its profits and paying fewer dividends to its parent company Kiwi Post and through that to the taxpayer. There are next to no dividends currently to stop distributing to fund a more aggressive mortgage rate setting policy.

Source: KiwiBank pays its first dividend of $21 million to Government | Stuff.co.nz.

KiwiBank paid its first dividend last year. Prior to that, the bank kept all profits to allow it to expand its lending base. $20 million in foregone dividends does not go far given the actual size of all lending markets in New Zealand.

Source: G1 Summary information for locally incorporated banks – Reserve Bank of New Zealand.

KiwiBank is minnow in the mortgage market and a pimple in commercial lending. Rapid business expansion is risky in any market, much less in banking.

The government has declined further capital injections so profits were retained to meet capital adequacy ratios. The government in 2010 earmarked NZ$300 million for an uncalled capital facility for NZ Post to help maintain its credit rating and KiwiBank’s growth.

Saving the best for last, KiwiBank last year announced plans to borrow up to $150 million through an issue of BB- perpetual capital notes to be used to bolster the bank’s regulatory capital position.

The Margin for the Perpetual Capital Notes has been set at 3.65% per annum and the interest rate will be 7.25% per annum for the first five years until the first reset date of 27 May 2020. Kiwi Capital Funding Limited is not guaranteed by KiwiBank, New Zealand Post nor the New Zealand Government.

The Perpetual Capital Notes have a BB- credit rating compared to KiwiBank which has an A- rating. These capital notes were issued in addition to prior subordinate debt in the form of CHF175 million (about NZ$233 million) worth of 5-year bonds.

I doubt that KiwiBank can raise capital through subordinated debt under normal commercial conditions if it does not plan to seek profits in the same way as other commercial banks do. The current issue of Perpetual Capital Notes are already rated as junk bonds:

An issue of $150 million of perpetual capital notes from KiwiBank with a speculative, or "junk", credit rating have been priced at the bottom of their indicative margin range.

The closest the prospectus for these Perpetual Capital Notes got to complementing KiwiBank changing from a normal business to being a public good is the following risk statement:

Kiwibank’s banking activities are subject to extensive regulation, mainly relating to capital, liquidity levels, solvency and provisioning.

Its business and earnings are also affected by the fiscal or other policies that are adopted by various regulatory authorities of the New Zealand Government.

The interest rate on this subordinate debt will go up to offset the additional risk of aggressive lending and aggressive expansion, which will cancel out many of the advantages of not having to pay for dividends and the capital injection.

That discipline is one of the purposes of subordinate debt in the regulatory capital of banks. This is to provide another pair of eyes and ears to watch the performance of the bank and through rising costs of lending and risk ratings, signal trouble of imprudent lending and lack of cost control.

The proposal to use KiwiBank to lower mortgage rates does not add up. KiwiBank does not pay much in the way of dividends to fund such a foray. KiwiBank is already far more leveraged than any other New Zealand major bank.

Recent Comments