How the Oil Bust Could Reshape Global Markets | @WSJ

24 Apr 2020 Leave a comment

in energy economics Tags: cartel theory, economics of pandemics, Oil prices

After only 227 pages does @NZComCom reveal its criteria for markets predisposed to collusion

21 Aug 2019 Leave a comment

in applied price theory, history of economic thought, industrial organisation, law and economics, politics - New Zealand Tags: cartel theory, competition law, oligopoly

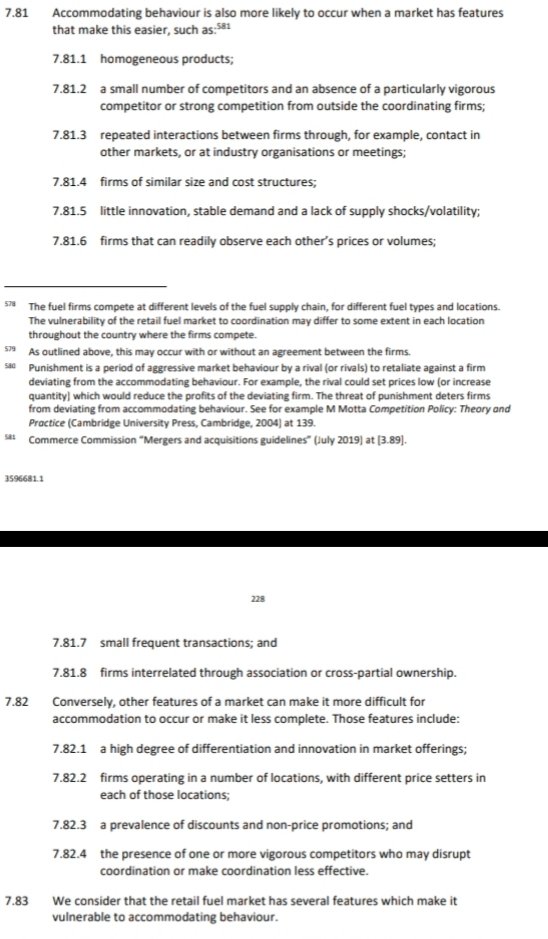

@NZComCom sees this price discounting as evidence of a stable cartel or tight oligopoly

21 Aug 2019 Leave a comment

in applied price theory, energy economics, industrial organisation, politics - New Zealand Tags: cartel theory, competition law

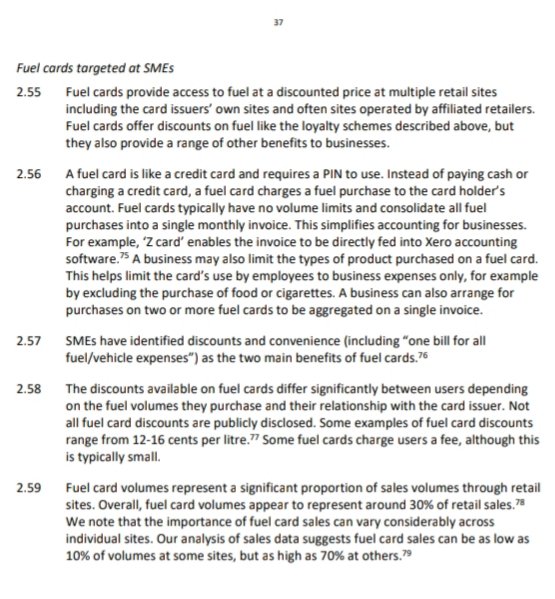

Despite itself, @nzcomcom reveals rampant secret price discounting in the petrol cartel/oligopoly

21 Aug 2019 Leave a comment

in applied price theory, economics of bureaucracy, energy economics, entrepreneurship, industrial organisation, law and economics, politics - New Zealand, Public Choice, survivor principle Tags: cartel enforcement, cartel theory, competition law

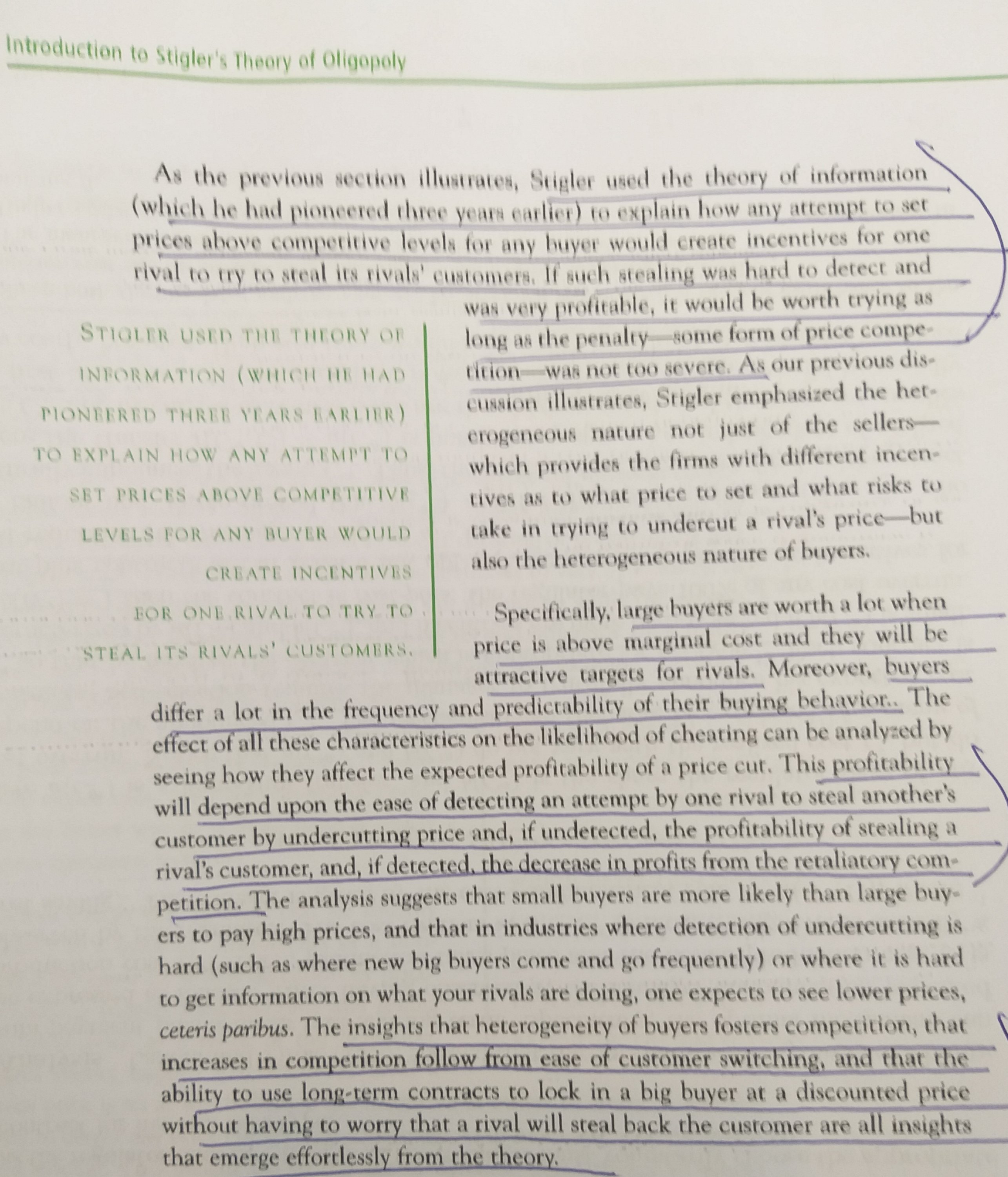

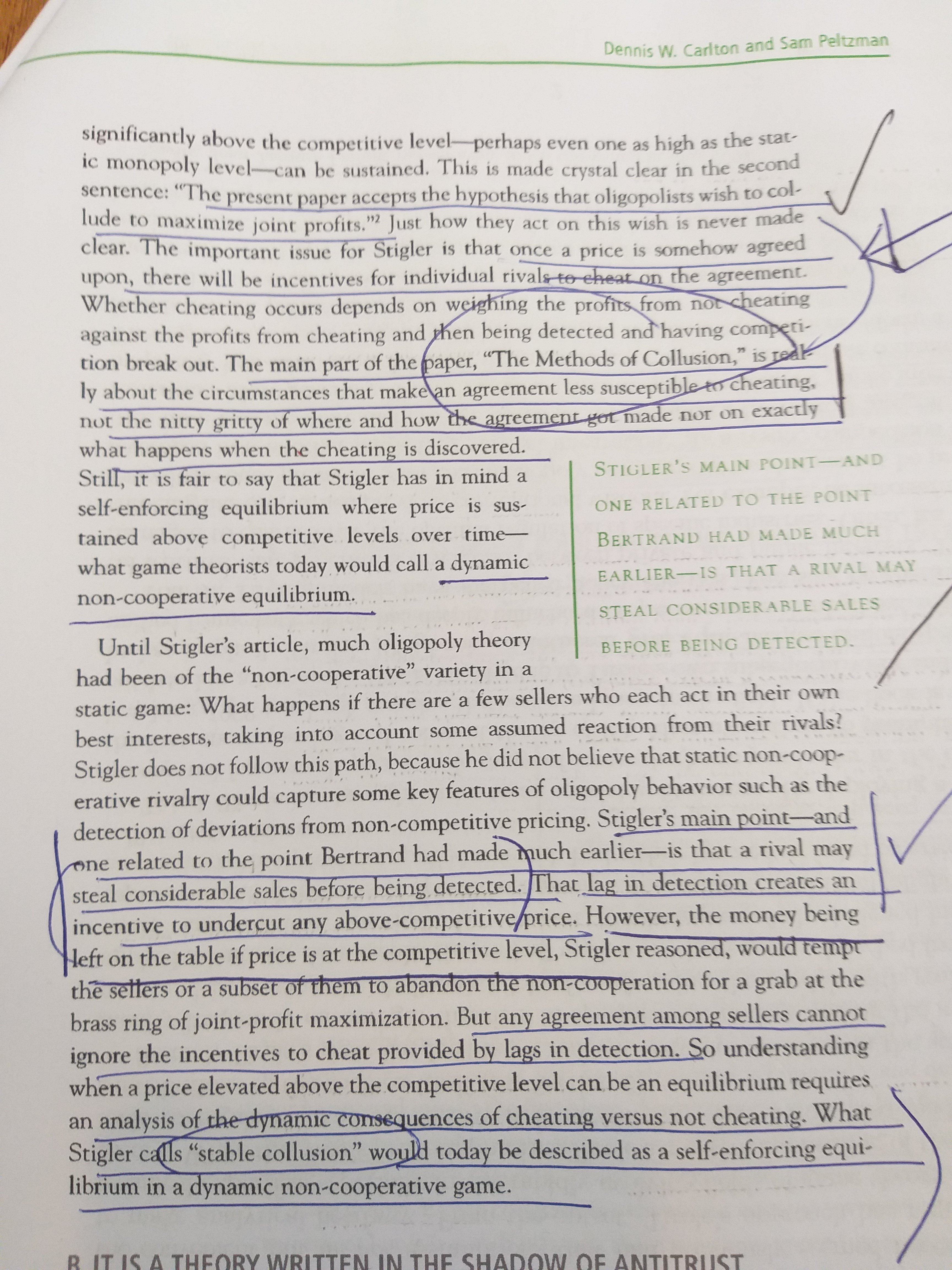

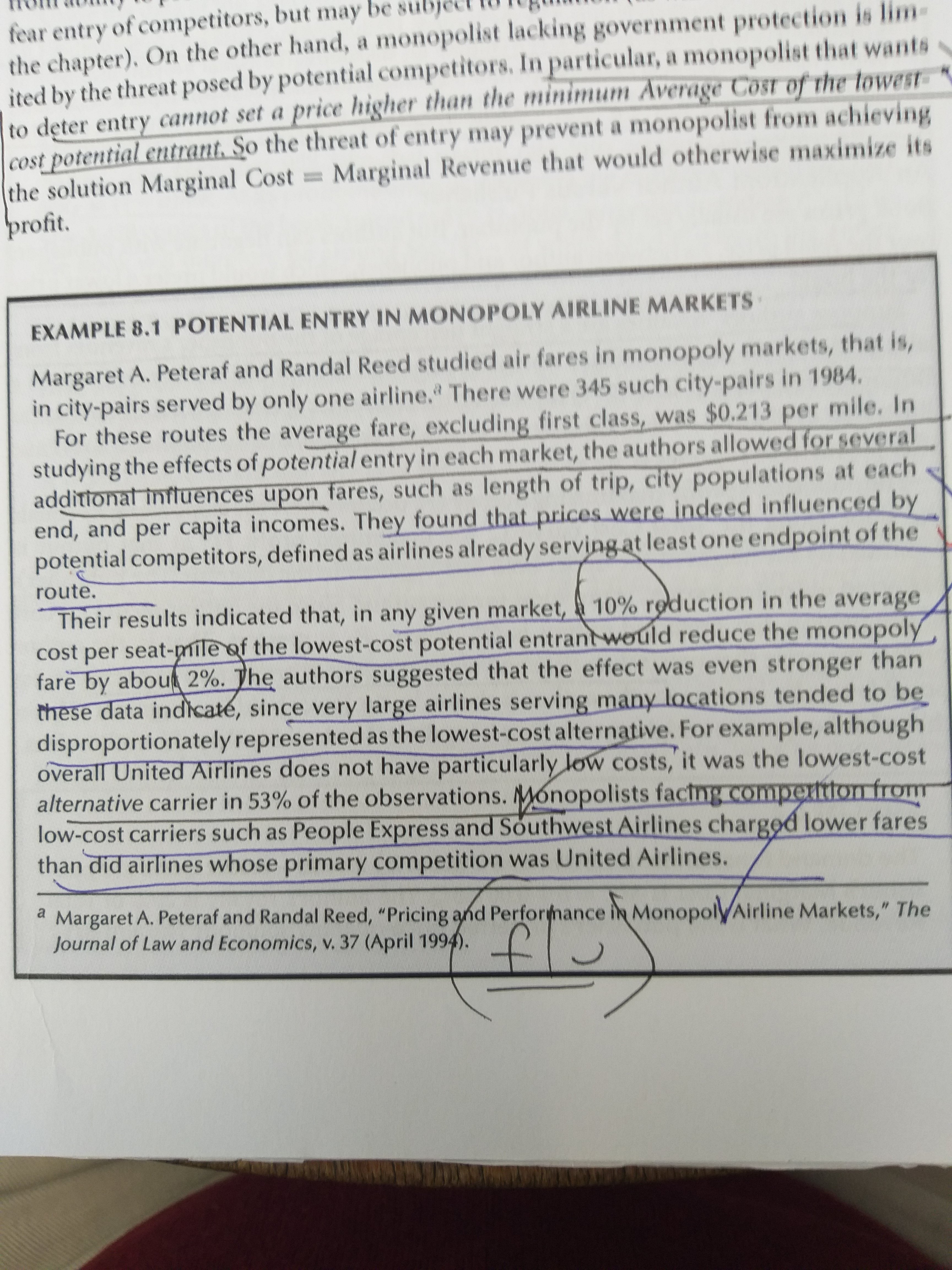

Carlton and Peltzman on who founded the modern theory of competition and oligopoly

20 Jul 2019 Leave a comment

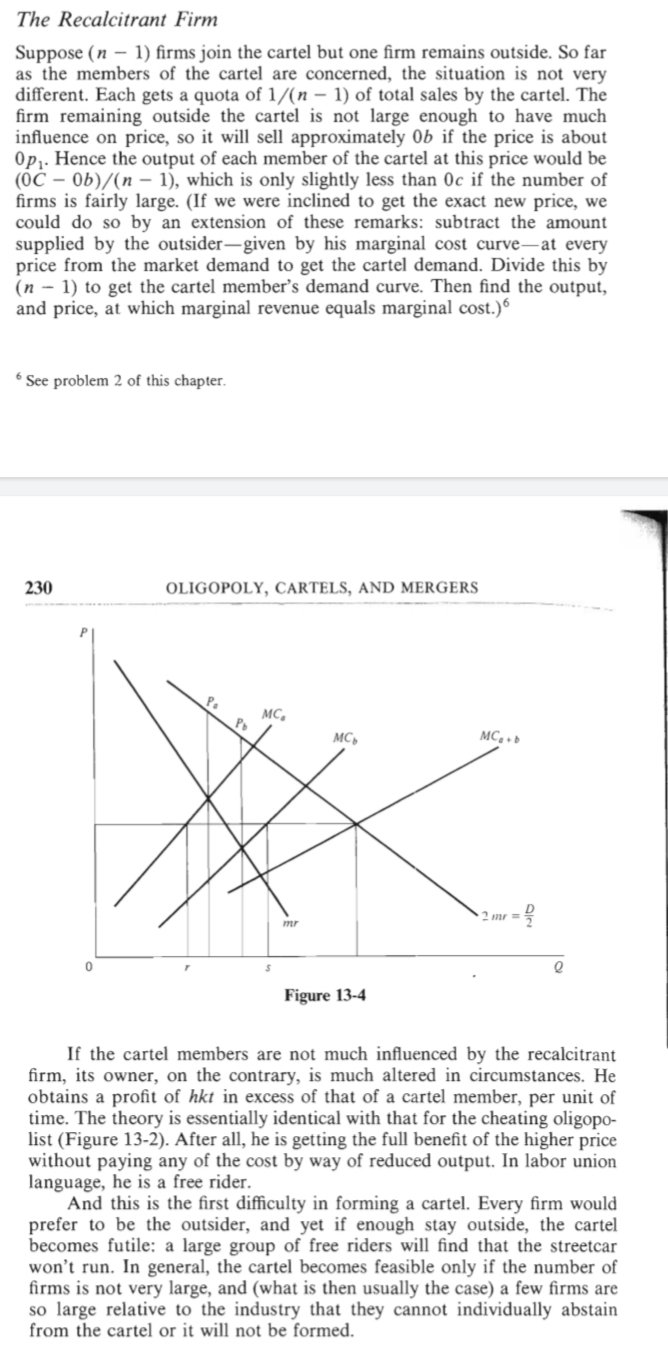

Why some bastard will always cheat on the agreement. Get your retaliation in first too.

17 Jul 2019 Leave a comment

in applied price theory, economics of information, industrial organisation, law and economics Tags: cartel enforcement, cartel theory, competition law, game theory, oligopoly

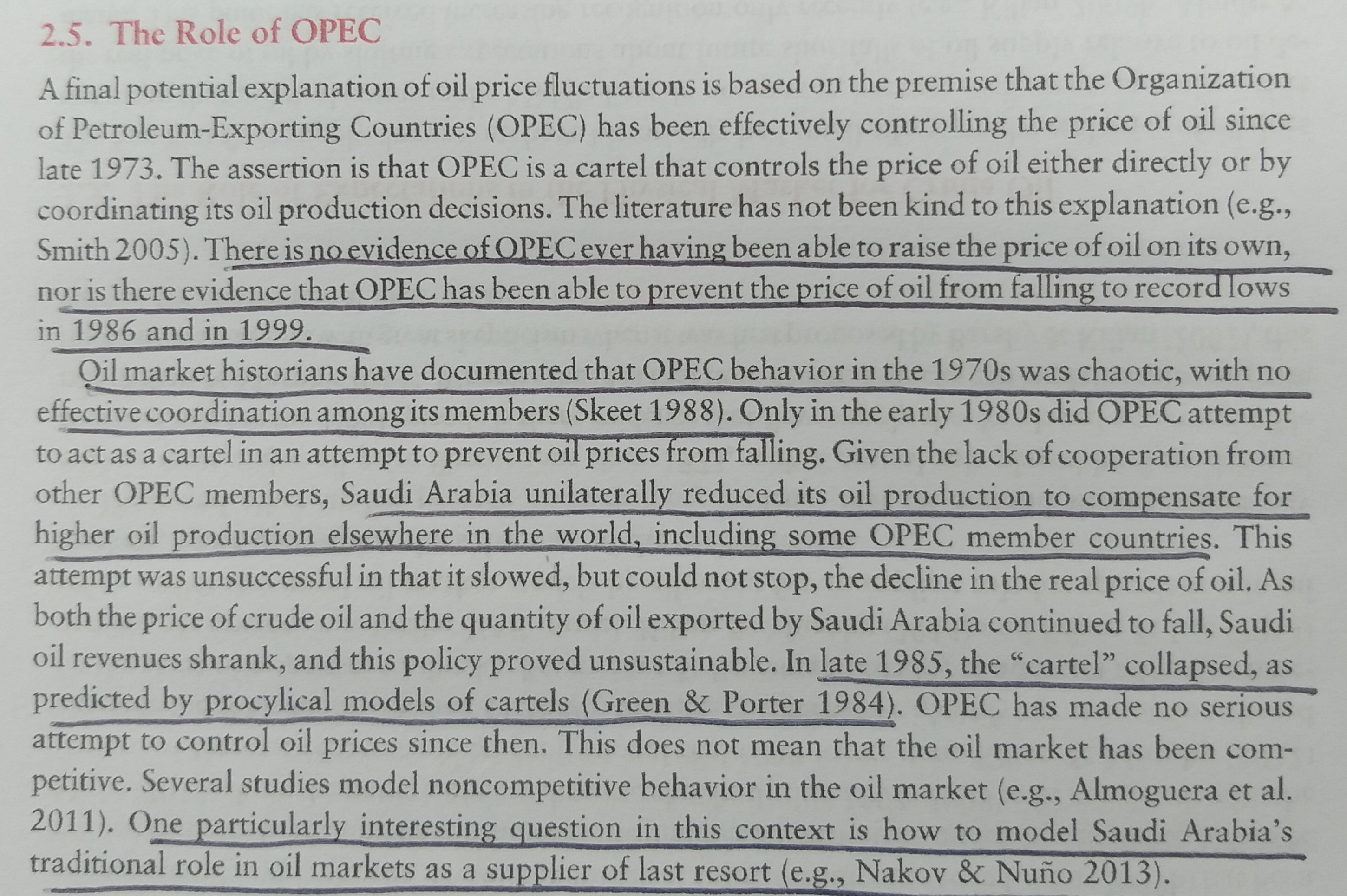

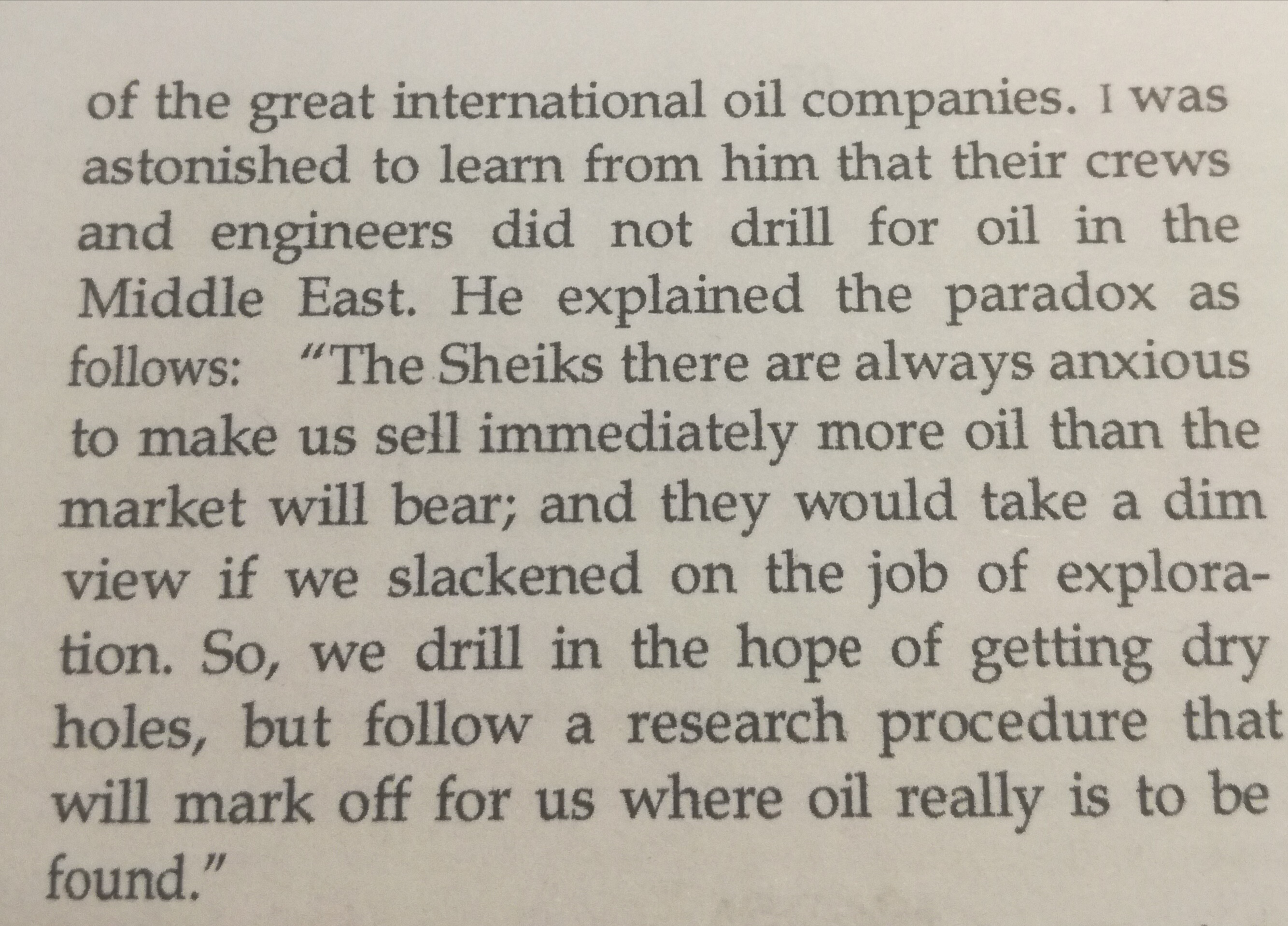

Paul Samuelson (1963) on oil cartel stability and cheating

23 Jun 2018 Leave a comment

in applied price theory, development economics, economic history, economics of bureaucracy, energy economics, industrial organisation, Public Choice, public economics Tags: cartel theory, OPEC

Recent Comments