Antitrust, Explained

14 Mar 2019 Leave a comment

in applied price theory, Austrian economics, industrial organisation, law and economics Tags: competition as a discovery procedure, competition law, creative destruction

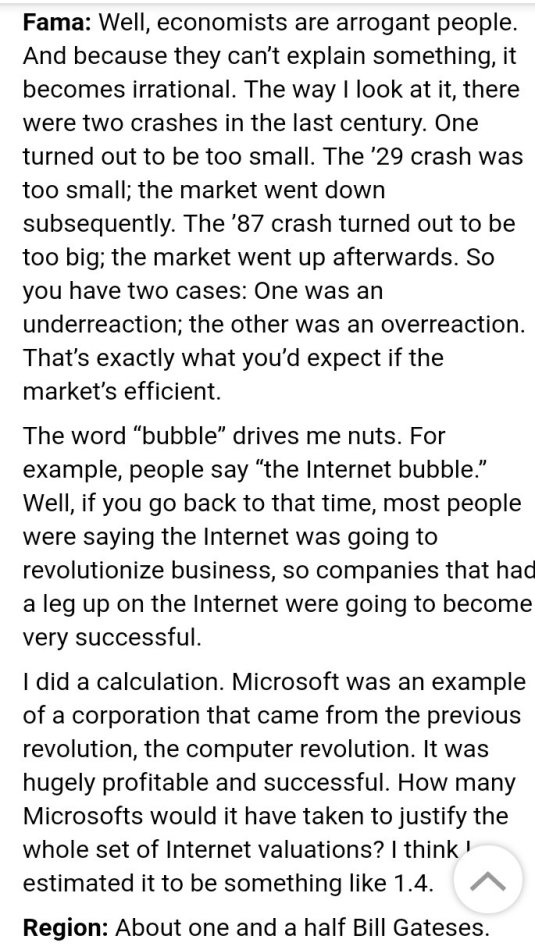

Watching a show about the dot com bubble: learning by investing

23 Jan 2019 Leave a comment

in financial economics, industrial organisation, survivor principle Tags: competition as a discovery procedure, efficient markets hypothesis

Market-based assurance of quality and performance alert

12 May 2017 Leave a comment

in economics of information, industrial organisation, survivor principle Tags: competition as a discovery procedure, experience goods, The meaning of competition experience goods

Why does an industry need regulation when incidents of malfeasance are front page news that closes the offending business for good? Social media is another market discipline of quality.

Adam Smith on entrepreneurial drive

02 Jan 2016 Leave a comment

in Adam Smith, applied price theory, applied welfare economics, entrepreneurship, history of economic thought, industrial organisation, survivor principle Tags: competition as a discovery procedure, creative destruction, entrepreneurial alertness, market selection, The meaning of competition

What is the only source of profit?

02 Dec 2015 Leave a comment

in applied price theory, Austrian economics, entrepreneurship, history of economic thought, industrial organisation, Ludwig von Mises, survivor principle Tags: competition as a discovery procedure, consumer sovereignty, entrepreneurial alertness, market process, market selection, profit and loss, The meaning of competition

Hayek’s use of knowledge in society

02 Oct 2015 Leave a comment

in applied price theory, economics of information, entrepreneurship, F.A. Hayek, industrial organisation, survivor principle Tags: competition as a discovery procedure, entrepreneurial alertness, market process, The meaning of competition

Hayek on the division of knowledge

15 Sep 2015 Leave a comment

in applied price theory, Austrian economics, economics of information, F.A. Hayek, industrial organisation, survivor principle Tags: capitalism and freedom, competition as a discovery procedure, The meaning of competition, The pretence to knowledge

Creative destruction in Silicon Valley

29 Aug 2015 Leave a comment

in economic history, economics of media and culture, entrepreneurship, financial economics, industrial organisation, survivor principle Tags: competition as a discovery procedure, creative destruction, efficient markets hypothesis, entrepreneurial alertness, ICT, Silicon Valley

Surging #SiliconValley — in 5 charts ow.ly/Qftvp http://t.co/1bGCz8G1dB—

(@AEI) July 29, 2015

@comcom Commerce Commission understands neither creative destruction nor the scourge of lower prices

24 Aug 2015 2 Comments

in applied price theory, economic history, economics of bureaucracy, history of economic thought, industrial organisation, Joseph Schumpeter, Public Choice, rentseeking, Ronald Coase, survivor principle Tags: antitrust law, competition as a discovery procedure, competition law, competition law enforcement, creative destruction, Harold Demsetz, special interests, The meaning of competition

In its 2014 Consumer Issues report, released under the Official Information Act, the New Zealand Commerce Commission said:

We are seeing signs that NFC transaction systems are replacing the current eftpos payment system with its lower fee structure.

This could result in a transaction fee structure monopoly, and increased charges to consumers as traders pass on their increased transaction costs through surcharges or increased prices.

The Commerce Commission seems rather concerned that one form of supply will be displaced by another at a lower price. This is the scourge of lower prices – a major preoccupation of competition authorities. They are yet to accept that lower prices should be always lawful under competition law.

The distribution of firm sizes reflects the rise and fall of firms in a competitive struggle to survive with competition between firms of different sizes sifting out the more efficient firm sizes (Stigler 1958, 1987; Demsetz 1973, 1976; Peltzman 1977; Jovanovic 1982; Jovanovic and MacDonald 1994b). Business vitality and capacity for growth and innovation are only weakly related to cost conditions and often depends on many factors that are subtle and difficult to observe (Stigler 1958, 1987).

The New Zealand Commerce Commission, the competition law enforcement authority, seems to have an infuriatingly simple and out-dated understanding of the meaning of competition. Joseph Schumpeter and Ronald Coase would be turning in their graves.

The efficient firm sizes are the sizes that survived in competition against other sizes. To survive, a firm must rise above all of problems it faces such as employee relations, skills development, innovation, changing regulations, unstable markets, access to finance and new entry. This is the decisive (and Darwinian) meaning of efficiency from the standpoint of the individual firm (Stigler 1958). One method of organisation supplants another when it can supply at a lower price (Marshall 1920, Stigler 1958).

What is even more distressing is the Commerce Commission is applying their archaic concept of competition to an industry subject to rapid innovation. Regulating innovation through competition law is never a good idea. The more efficient sized firms are the firm sizes that are expanding their market shares in the face of competition; the less efficient sized firms are those that are losing market share (Stigler 1958, 1987; Alchian 1950; Demsetz 1973, 1976).

https://twitter.com/balajis/status/465585152584716289

If the firm size distribution in an industry is relatively stable for a time, the firms are their current sizes because there are no more gains from further changes in size in light their underlying demand and cost conditions (Stigler 1983; Alchian 1950; Demsetz 1973, 1976).

Temporary monopoly and rapidly changing market shares with the occasional dominant firm are all characteristics of the early stages of any new or innovating industry. The deadweight social losses from the enforcement of competition law are at their greatest in industries undergoing rapid innovation because of the possibility of error is at its height. Optimum firm sizes continually change over time because of shifts in input and output prices and technological progress (Stigler 1958, 1983).

The Netflix Effect (via @Mark_J_Perry) http://t.co/LkDjfarRZa—

Michael Hendrix (@michael_hendrix) August 11, 2015

If large firm size is better at serving consumers, the large firms start to grow and smaller firms will die or be absorbed until the untapped gains from growth in firm size are exhausted. Firms increase in size and decrease in number when this adaptation becomes necessary to survive. If a smaller firm size is now better, smaller firms will multiply and the larger firms will decline in size because they are under-cut on price and quality.

The life cycle of many industries starts with a burst of new entrants with similar products. These new or upgraded products often use ideas that cross-fertilise. In time, there is an industry shakeout where a few leapfrog the rest with cost savings and design breakthroughs to yield the mature product (Jovanovic and MacDonald 1994a; Boldrin and Levine 2008, 2013). Fast-seconds and practical minded latecomers often imitate and successfully commercialise ideas seeded by the market pioneers using prior ideas as knowledge spillovers. Their large market shares are their prizes for winning the latest product races, not the basis of their initial victories.

New entrants regard a large firm size as a premature risk rather than an advantage of incumbency they should mimic as soon as they can. New firms set-up on a scale that is well below the minimum efficient production scale for their industry (Bartelsman, Haltiwanger, and Scarpetta 2009). New entrants choose to start so small to test the waters regarding their true productivity and the market’s acceptance of their products and to minimise losses in the event of failure (Jovanovic 1982; Ericson and Pakes 1995; Dhawan 2001; Audretsch, Prince and Thurik 1998; Audretsch and Mahmood 1994).

Competition law can subvert competition by stymieing the introduction of new goods and the temporary monopoly often necessary to recoup their invention costs and induce innovation. The puzzlingly large productivity differences across firms even in narrowly defined industries producing standard products lead to doubts about the efficiency of some firms, often the smaller firms in an industry. Some firms produce half as much output from the same measured inputs as their market rivals and still survive in competition (Syverson 2011). This diversity reflects inter-firm differences in managerial ability, organisational practices, choice of technology, the age of the business and its capital, location, workforce skills, intangible assets and changes in demand and productivity that are idiosyncratic to each individual firm (Stigler 1958, 1976, 1987; De Alessi 1983).

Technological progress comes from innovations that are the result of profit orientated research and development in the course of market competition. The two main inputs into innovation are the private expenditures of prospective innovators on R&D workers and equipment and the publicly available stock of knowledge on which they hope to build (Aghion and Howitt 2008). Any profits of successful innovators last until others innovate to supersede previous innovations (Aghion and Howitt 2008).

Harold Demsetz argued that competition does not take place upon a single margin, such as price competition. Competition instead has several dimensions often inversely correlated with each other. Because of this, a competition law disparaging one form of competition will result in more of another. There are trade-offs between innovation and current price competition. Manne and Wright noted in the paper, Innovation and the Limits of Antitrust that:

Both product and business innovations involve novel practices, and such practices generally result in monopoly explanations from the economics profession followed by hostility from the courts (though sometimes in reverse order) and then a subsequent, more nuanced economic understanding of the business practice usually recognizing its pro-competitive virtues.

A competition law enforcement authority should never pretend to know which trade-off between innovation and price competition and between competition and temporary monopoly are optimal. Every competition authority should simplify the regulatory environment by simply saying lower prices are per always lawful. The New Zealand Commerce Commission should do this but it has not.

I have not even touched on the use of competition law to subvert competition such is the pursuit of Microsoft and Google by its business rivals through competition law.

The easiest way to tell if a merger is pro-competition is if the remaining firms in the market oppose it. If it was anti-competitive, they could match the higher prices of the merged firm. The reason they oppose the merger is the merged firm will start undercutting them on price. When was the last time a competitor complained about their rivals putting their prices up? Either they hold their prices and take their business or follow their pricing lead: can’t lose.

Should We Subsidize Scientific Research?

18 Aug 2015 Leave a comment

in applied price theory, applied welfare economics, entrepreneurship, industrial organisation, Public Choice, rentseeking, survivor principle Tags: competition as a discovery procedure, economics of science, industry policy, losers, picking winners, R&D, The meaning of competition, The pretence the knowledge

Recent Comments