The Economics of #Brexit – Richard Baldwin

18 Apr 2016 Leave a comment

in applied price theory, applied welfare economics, economics of regulation, international economics Tags: Brexit

Water Policies for People, by David Zetland

18 Apr 2016 Leave a comment

in economics, economics of regulation, environmental economics, industrial organisation, law and economics, privatisation, property rights, survivor principle Tags: Economics of water

The contradictions of decriminalising marijuana and banning tobacco

12 Apr 2016 Leave a comment

in economics of regulation, health economics Tags: economics are smoking, Left-wing hypocrisy, marijuana decriminalisation

Deposit insurance

11 Apr 2016 Leave a comment

in applied price theory, business cycles, economic history, economics, economics of regulation, global financial crisis (GFC), macroeconomics, monetary economics, Public Choice, rentseeking Tags: bank runs, banking crises, banking panics, deposit insurance, Thomas Sargent

Many of the key issues about what modern macroeconomics has to say on global financial crises and deposit insurance are discussed in a 2010 interview with Thomas Sargent

Sargent said that two polar models of bank crises and what government lender-of-last-resort and deposit insurance do to arrest or promote them were used to understand the GFC. They are polar models because:

- in the Diamond-Dybvig and Bryant model of banking runs, deposit insurance and other bailouts are purely a good thing stopping panic-induced bank runs from ever starting; and

- in the Kareken and Wallace model, deposit insurance by governments and the lender-of-last-resort function of a central bank are purely a bad thing because moral hazard encourages risk taking unless there is regulation or there is proper surveillance and accurate risk-based pricing of the deposit insurance.

In the Diamond-Dybvig and Bryant model, if there is government-supplied deposit insurance, people do not initiate bank runs because they trust their deposits to be safe. There is no cost to the government for offering the deposit insurance because there are no bank runs! A major free lunch.

Tom Sargent considers that the Bryant-Diamond-Dybvig model has been very influential, in general, and among policy makers in 2008, in particular.

Governments saw Bryant-Diamond-Dybvig bank runs everywhere. The logic of this model persuaded many governments that if they could arrest the actual or potential runs by convincing creditors that their loans were insured, that could be done at little or no eventual cost to taxpayers.

In 2008, the Australian and New Zealand governments announced emergency bank deposit insurance guarantees. In Bryant-Diamond-Dybvig style bank panics, these guarantees ward off the bank run and thus should cost nothing fiscally because the deposit insurance is not called upon. These guarantees and lender of last resort function were seen as key stabilising measures. These guarantees were called upon in NZ to the tune of $2 billion.

- 1. The Diamond-Dybvig and Bryant model makes you sensitive to runs and optimistic about the ability of deposit insurance to cure them.

- The Kareken and Wallace model’s prediction is that if a government sets up deposit insurance and doesn’t regulate bank portfolios to prevent them from taking too much risk, the government is setting the stage for a financial crisis.

- The Kareken-Wallace model makes you very cautious about lender-of-last-resort facilities and very sensitive to the risk-taking activities of banks.

Kareken and Wallace called for much higher capital reserves for banks and more regulation to avoid future crises. This is not a new idea.

Sam Peltzman in the mid-1960s found that U.S. banks in the 1930s halved their capital ratios after the introduction of federal deposit insurance. FDR was initially opposed to deposit insurance because it would encourage greater risk taking by banks.

Late on Friday afternoon, Stuff posted an op-ed piece calling for the introduction of a (funded) deposit insurance scheme in New Zealand. It was written by Geof Mortlock, a former colleague of mine at the Reserve Bank, who has spent most of his career on banking risk issues, including having been heavily involved in the handling of the failure, and resulting statutory management, of DFC.

As the IMF recently reported, all European countries (advanced or emerging) and all advanced economies have deposit insurance, with the exception of San Marino, Israel and New Zealand. An increasing number of people have been calling for our politicians to rethink New Zealand’s stance in opposition to deposit insurance. I wrote about the issue myself just a couple of months ago, in response to some new material from the Reserve Bank which continues to oppose deposit insurance.

Different people emphasise different arguments in making the case for New Zealand to…

View original post 1,963 more words

Bjorn Lomborg: How to fix global warming smartly

08 Apr 2016 Leave a comment

in applied price theory, applied welfare economics, climate change, economics of regulation, environmental economics, global warming

In 1922 Princeton banned students from owning automobiles

07 Apr 2016 1 Comment

in economic history, economics of information, economics of media and culture, economics of regulation, technological progress Tags: doomsday prophets, good old days

The 1st @PaulKrugman on @GrantRobertson1’s #futureofwork?

21 Mar 2016 Leave a comment

in economics of regulation, labour economics, minimum wage, politics - USA, poverty and inequality, unemployment Tags: employment law, employment protection laws, France, labour market regulation, New Zealand Labour Party, rent control, social insurance, The fatal conceit, unintended consequences

Source: Paul Krugman (1997) Unmitigated Gauls.

@mattyglesias on why greedy drug companies are heroes

20 Mar 2016 Leave a comment

in economics of regulation, health economics, law and economics, politics - New Zealand, politics - USA, property rights Tags: avoiding difficult choices, drug lags, generic drugs, intellectual monopolies, invisible graveyard, patents and copyrights

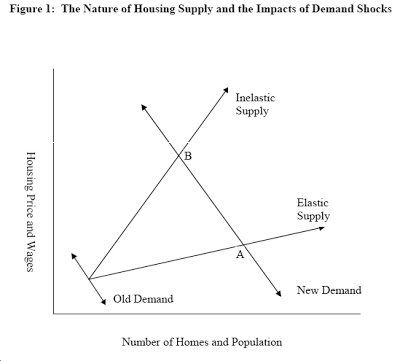

Las Vegas population since 1900

18 Mar 2016 Leave a comment

in economic history, economics of regulation, population economics, urban economics Tags: land supply, land use planning, Las Vegas, zoning

The Las Vegas population doubled in the 60s doubled again between 1970 and 1990 and almost doubled again by 2000.

Source: Insiderviewpoint.com Las Vegas Population.

Between 1990 and 2000 despite the doubling of population, housing prices only increased by 25%.

Source: Insiderviewpoint.com S&P/Case-Shiller Las Vegas Home Price Index – S&P Dow Jones Indices.

Land supply must be pretty easy in Las Vegas at least up until 2000.

Source: Economics of Contempt: Land Use Regulations and the Housing Bubble.

The share market speaks on the UK #sugartax @JulieAnneGenter @GreenCatherine

18 Mar 2016 Leave a comment

in economics of regulation, financial economics, health economics Tags: British economy, libertarian paternalism, meddlesome preferences, nanny state, sugar tax

The biggest drop was in a company that sold its sugar interests in 2009 so that was a rather within the day affair once traders realised their error.

% of New Zealand mortgages that were fixed and floating since 2004

16 Mar 2016 Leave a comment

in economic history, economics of information, economics of regulation, monetary economics, politics - USA Tags: antimarket bias, libertarian paternalism, monetary policy, mortgage interest rates, New Zealand Labour Party, Other people are stupid fallacy, rational irrationality, The fatal conceit, The pretence to knowledge

Despite the best efforts of the libertarian paternalists to sell the other people are stupid fallacy, ordinary New Zealanders are quite nimble at moving between fixed and floating rates depending upon their forecasts of the future of interest rates. Price controls on floating rate mortgages, as suggested by the New Zealand Labour Party, would make this more difficult, not easier.

Source: S8 Banks: Mortgage lending ($m) – Reserve Bank of New Zealand.

Percentage of fixed and floating mortgages in New Zealand

16 Mar 2016 Leave a comment

in economics of regulation, industrial organisation, monetary economics, politics - New Zealand Tags: antimarket bias, mortgage interest rates, New Zealand Greens, New Zealand Labour Party, price controls, rational irrationality

I did not know so many people were on a fixed rate mortgage. Labour is risking its economic credibility on regulating the rates for a minority of mortgages.

Source: S8 Banks: Mortgage lending ($m) – Reserve Bank of New Zealand.

Capped mortgages cannot be linked to the current official cash rate of the Reserve Bank of New Zealand because they are based on expected future interest rates over an up to 5 year span, not current interest rates.

An important motivation for going onto a floating rate is you can repay faster. Fixed rate mortgages have penalties for early repayment.

Source: Price Controls: Price Floors and Ceilings, Illustrated.

In consequence, price controls linking floating rate mortgages to the official cash rate of the Reserve Bank would benefit better off mortgagees expecting to repay quickly. A typical policy of the modern Labour Party.

Fruits and vegetables, wild vs. domesticated

12 Mar 2016 Leave a comment

in economic history, economics of information, economics of media and culture, economics of regulation, environmental economics, health economics Tags: agricultural economics, antiscience left, food snobs, GMOs, organic food

Solution aversion and the anti-science Left

11 Mar 2016 1 Comment

in applied price theory, applied welfare economics, comparative institutional analysis, constitutional political economy, economics of regulation, energy economics, environmental economics, global warming, health economics, law and economics, politics - Australia, politics - New Zealand, politics - USA, property rights, Public Choice Tags: antiscience left, climate alarmism, geo-engineering, GMOs, growth of knowledge, gun control, motivated reasoning, nuclear power, political persuasion, solar power, solution aversion, wind power

Climate science is the latest manifestation of solution aversion: denying a problem because it has a costly solution. The Right does this on climate science, the Left does it on gun control, GMOs, and plenty more. Cass Sunstein explains:

It is often said that people who don’t want to solve the problem of climate change reject the underlying science, and hence don’t think there’s any problem to solve.

But consider a different possibility: Because they reject the proposed solution, they dismiss the science. If this is right, our whole picture of the politics of climate change is off.

Some psychologists wasted grant money on lab experiments to show that people that think the solution to a problem is costly tend to rubbish every aspect of the argument. Any politician will tell you you do not concede anything. Sunstein again:

Campbell and Kay asked the participants whether they agreed with the IPCC. And in both, about 80 percent of Democrats did agree; the policy solutions made no difference.

Republicans, in contrast, were far more likely to agree with the IPCC when the proposed solution didn’t involve regulatory restrictions…

Here, then, is powerful evidence that many people (of course not all) who purport to be skeptical about climate science are motivated by their hostility to costly regulation.

The Left is equally prone to motivated readings. For example, it was found that those on the left are much more concerned about home invasions when gun control can reduce them rather than increase them.

The Left picks and chooses which scientific consensus as it accepts. The overwhelming consensus among researchers is biotech crops are safe for humans and the environment. This is a conclusion that is rejected by the very environmentalist organisations that loudly insist on the policy relevance of the scientific consensus on global warming.

Previously the precautionary principle was used to introduce doubt when there was no doubt. But when climate science turned in their favour, environmentalists wanted public policy to be based on the latest science.

The Right is welcoming of the science of nuclear energy or geo-engineering. The Left rejects it point-blank. Their refusal to consider nuclear energy as a solution to global warming is a classic example of solution aversion. Let he who is without sin cast the first stone.

How did German, Italian, French, British and American billionaires make their money?

26 Feb 2016 Leave a comment

in economic history, economics of regulation, entrepreneurship, industrial organisation, survivor principle Tags: billionaires, British economy, entrepreneurial alertness, France, Germany, Italy, superstar wages, superstars

Recent Comments