The first words uttered in my first lecture in applied welfare economics by Bob Rutherford were ‘this course starts with an explicit political position – that of liberalism’. I never forgot that.

This leads us to Robert and Zeckhauser’s taxonomy of disagreement:

Positive disagreements can be over questions of:

1. Scope: what elements of the world one is trying to understand?

2. Model: what mechanisms explain the behaviour of the world?

3. Estimate: what estimates of the model’s parameters are thought to obtain in particular contexts?

Values disagreements can be over questions of:

1. Standing: who counts?

2. Criteria: what counts?

3. Weights: how much different individuals and criteria count?

Any positive analysis tends to include elements of scope, model, and estimation, though often these elements intertwine; they frequently feature in debates in an implicit or undifferentiated manner. Likewise, normative analysis will also include elements of standing, criteria, and weights, whether or not these distinctions are recognised.

The origin of political disagreement is a broad church indeed in a liberal democracy. Those you disagree with are not evil, they just disagree with you. As Karl Popper observed:

There are many difficulties impeding the rapid spread of reasonableness. One of the main difficulties is that it always takes two to make a discussion reasonable. Each of the parties must be ready to learn from the other.

We are seeing signs that NFC transaction systems are replacing the current eftpos payment system with its lower fee structure.

This could result in a transaction fee structure monopoly, and increased charges to consumers as traders pass on their increased transaction costs through surcharges or increased prices.

The Commerce Commission seems rather concerned that one form of supply will be displaced by another at a lower price. This is the scourge of lower prices – a major preoccupation of competition authorities. They are yet to accept that lower prices should be always lawful under competition law.

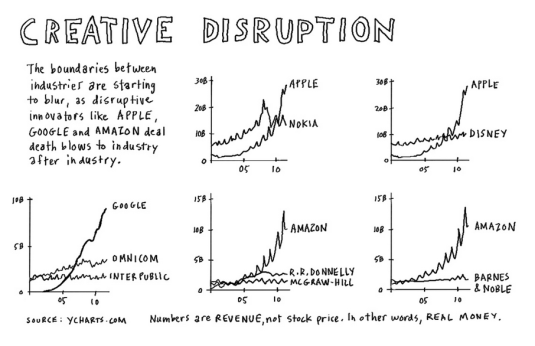

The distribution of firm sizes reflects the rise and fall of firms in a competitive struggle to survive with competition between firms of different sizes sifting out the more efficient firm sizes (Stigler 1958, 1987; Demsetz 1973, 1976; Peltzman 1977; Jovanovic 1982; Jovanovic and MacDonald 1994b). Business vitality and capacity for growth and innovation are only weakly related to cost conditions and often depends on many factors that are subtle and difficult to observe (Stigler 1958, 1987).

The New Zealand Commerce Commission, the competition law enforcement authority, seems to have an infuriatingly simple and out-dated understanding of the meaning of competition. Joseph Schumpeter and Ronald Coase would be turning in their graves.

The efficient firm sizes are the sizes that survived in competition against other sizes. To survive, a firm must rise above all of problems it faces such as employee relations, skills development, innovation, changing regulations, unstable markets, access to finance and new entry. This is the decisive (and Darwinian) meaning of efficiency from the standpoint of the individual firm (Stigler 1958). One method of organisation supplants another when it can supply at a lower price (Marshall 1920, Stigler 1958).

What is even more distressing is the Commerce Commission is applying their archaic concept of competition to an industry subject to rapid innovation. Regulating innovation through competition law is never a good idea. The more efficient sized firms are the firm sizes that are expanding their market shares in the face of competition; the less efficient sized firms are those that are losing market share (Stigler 1958, 1987; Alchian 1950; Demsetz 1973, 1976).

If the firm size distribution in an industry is relatively stable for a time, the firms are their current sizes because there are no more gains from further changes in size in light their underlying demand and cost conditions (Stigler 1983; Alchian 1950; Demsetz 1973, 1976).

Temporary monopoly and rapidly changing market shares with the occasional dominant firm are all characteristics of the early stages of any new or innovating industry. The deadweight social losses from the enforcement of competition law are at their greatest in industries undergoing rapid innovation because of the possibility of error is at its height. Optimum firm sizes continually change over time because of shifts in input and output prices and technological progress (Stigler 1958, 1983).

If large firm size is better at serving consumers, the large firms start to grow and smaller firms will die or be absorbed until the untapped gains from growth in firm size are exhausted. Firms increase in size and decrease in number when this adaptation becomes necessary to survive. If a smaller firm size is now better, smaller firms will multiply and the larger firms will decline in size because they are under-cut on price and quality.

The life cycle of many industries starts with a burst of new entrants with similar products. These new or upgraded products often use ideas that cross-fertilise. In time, there is an industry shakeout where a few leapfrog the rest with cost savings and design breakthroughs to yield the mature product (Jovanovic and MacDonald 1994a; Boldrin and Levine 2008, 2013). Fast-seconds and practical minded latecomers often imitate and successfully commercialise ideas seeded by the market pioneers using prior ideas as knowledge spillovers. Their large market shares are their prizes for winning the latest product races, not the basis of their initial victories.

New entrants regard a large firm size as a premature risk rather than an advantage of incumbency they should mimic as soon as they can. New firms set-up on a scale that is well below the minimum efficient production scale for their industry (Bartelsman, Haltiwanger, and Scarpetta 2009). New entrants choose to start so small to test the waters regarding their true productivity and the market’s acceptance of their products and to minimise losses in the event of failure (Jovanovic 1982; Ericson and Pakes 1995; Dhawan 2001; Audretsch, Prince and Thurik 1998; Audretsch and Mahmood 1994).

Competition law can subvert competition by stymieing the introduction of new goods and the temporary monopoly often necessary to recoup their invention costs and induce innovation. The puzzlingly large productivity differences across firms even in narrowly defined industries producing standard products lead to doubts about the efficiency of some firms, often the smaller firms in an industry. Some firms produce half as much output from the same measured inputs as their market rivals and still survive in competition (Syverson 2011). This diversity reflects inter-firm differences in managerial ability, organisational practices, choice of technology, the age of the business and its capital, location, workforce skills, intangible assets and changes in demand and productivity that are idiosyncratic to each individual firm (Stigler 1958, 1976, 1987; De Alessi 1983).

Technological progress comes from innovations that are the result of profit orientated research and development in the course of market competition. The two main inputs into innovation are the private expenditures of prospective innovators on R&D workers and equipment and the publicly available stock of knowledge on which they hope to build (Aghion and Howitt 2008). Any profits of successful innovators last until others innovate to supersede previous innovations (Aghion and Howitt 2008).

Harold Demsetz argued that competition does not take place upon a single margin, such as price competition. Competition instead has several dimensions often inversely correlated with each other. Because of this, a competition law disparaging one form of competition will result in more of another. There are trade-offs between innovation and current price competition. Manne and Wright noted in the paper, Innovation and the Limits of Antitrust that:

Both product and business innovations involve novel practices, and such practices generally result in monopoly explanations from the economics profession followed by hostility from the courts (though sometimes in reverse order) and then a subsequent, more nuanced economic understanding of the business practice usually recognizing its pro-competitive virtues.

A competition law enforcement authority should never pretend to know which trade-off between innovation and price competition and between competition and temporary monopoly are optimal. Every competition authority should simplify the regulatory environment by simply saying lower prices are per always lawful. The New Zealand Commerce Commission should do this but it has not.

I have not even touched on the use of competition law to subvert competition such is the pursuit of Microsoft and Google by its business rivals through competition law.

The easiest way to tell if a merger is pro-competition is if the remaining firms in the market oppose it. If it was anti-competitive, they could match the higher prices of the merged firm. The reason they oppose the merger is the merged firm will start undercutting them on price. When was the last time a competitor complained about their rivals putting their prices up? Either they hold their prices and take their business or follow their pricing lead: can’t lose.

We are constantly told that “everyone has a right to their opinion” and “there are two sides to every story.” Our entire news system is predicated on the notion that we need to give fair time to both sides of every situation. The problem with this type of thinking is that it leads to the misconception that both sides are equally valid, or, at the very least, that there must be some truth to both sides, but in many cases, only one side has any merit. In other words, it’s often not opinion #1 vs. opinion #2, rather, it is fact vs. fiction. One “side” is reality, while the other “side” is a fairy tail. For example, if you want to say that the island of Jamaica is being carried around on the back of giant sea turtle, that’s not your opinion, you’re just wrong. There wouldn’t be two legitimate…

One measure of the scale of austerity in Greece…and other advanced economies. http://t.co/PxCLagdd3L— RBS Economics (@RBS_Economics) July 06, 2015

The employment level in #Greece is back to where it was in 1985. It's the equivalent of the UK losing 6 million jobs. http://t.co/AAWHMEFwfK— RBS Economics (@RBS_Economics) July 06, 2015

The term ‘human capital’ was initially controversial, but the analytical concept was not. The analysis of human capital has many famous parents and grandparents (Kiker 1966).

Sir William Petty published the first analysis of the value of human capital in 1690. There were sophisticated analyses of investments in education and training and their implications for wage differentials, labour productivity and occupational choice by Adam Smith in 1776, Alfred Marshall in 1890 and Milton Friedman and Simon Kuznets in 1945.

Richard Cantillon, John Locke, John Stuart Mill, Adam Smith and Karl Marx all proposed that training rather than natural ability was more important in understanding occupational wage differentials. Adam Smith and Alfred Marshall referred to education and training as capital investments in human beings.

Irving Fisher in 1912 and Arthur Pigou in 1928 pioneered the explicit use of the term ‘human capital’. Jacob Mincer, Theodore Shultz and Gary Becker popularised the use of the term in the mid-20th century. See Kiker (1966) for a history of the concept of human capital.

This first screenshot is from the New York Times today of Paul Krugman’s current recollection of his interpretation of the Card – Kruger study of minimum wages in restaurants when that study was published all those years ago.

Paul Krugman in his review of Living Wage: What It Is and Why We Need It By Robert Pollin and Stephanie Luce in 1998 was far wiser.

So what are the effects of increasing minimum wages? Any Econ 101 student can tell you the answer: The higher wage reduces the quantity of labour demanded, and hence leads to unemployment. This theoretical prediction has, however, been hard to confirm with actual data.

Indeed, much-cited studies by two well-regarded labour economists, David Card and Alan Krueger, find that where there have been more or less controlled experiments, for example when New Jersey raised minimum wages but Pennsylvania did not, the effects of the increase on employment have been negligible or even positive.

Exactly what to make of this result is a source of great dispute. Card and Krueger offered some complex theoretical rationales, but most of their colleagues are unconvinced; the centrist view is probably that minimum wages “do,” in fact, reduce employment, but that the effects are small and swamped by other forces.

What is remarkable, however, is how this rather iffy result has been seized upon by some liberals as a rationale for making large minimum wage increases a core component of the liberal agenda–for arguing that living wages “can play an important role in reversing the 25-year decline in wages experienced by most working people in America” (as this book’s back cover has it).

Clearly these advocates very much want to believe that the price of labour–unlike that of gasoline, or Manhattan apartments–can be set based on considerations of justice, not supply and demand, without unpleasant side effects.

This will to believe is obvious in this book: The authors not only take the Card-Krueger results as gospel, but advance a number of other arguments that just do not hold up under examination.

The Card– Kruger results have gone from rather iffy in the mind of Paul Krugman to the basis of public policy that, if wrong, costs a lot of low paid workers their jobs. Krugman was well aware in 1998 what a risky path minimum wage increases were:

Now to me, at least, the obvious question is, why take this route? Why increase the cost of labour to employers so sharply, which–Card/Krueger notwithstanding–must pose a significant risk of pricing some workers out of the market, in order to give those workers so little extra income?

Why not give them the money directly, say, via an increase in the tax credit?

Studies of tiny increases in the minimum wage are being used to justify far larger increases in the minimum wage. Krugman was right to be suspect of that in 1998.

Krugman’s statements today in the New York Times about the low starting point in modern America for any minimum wage increases is still keeping that slightly cautious tone in his analysis. Few who read his analysis will carry that passing nuance into their own policy advocacy.

Paul Krugman in 1998 was quite astute as to why people want to believe the minimum wage can be increased without any cost to jobs:

One answer is political: What a shift from income supports to living wage legislation does is to move the costs of income redistribution off-budget. And this may be a smart move if you believe that America should do more for its working poor, but that if it comes down to spending money on-budget it won’t.

Indeed, this is a popular view among economists who favour national minimum-wage increases: They will admit to their colleagues that such increases are not the best way to help the poor, but argue that it is the only politically feasible option.

Nor in 1998 was Krugman blind to the expressive politics, the ideological blindness of those who advocate minimum wage increases and living wages:

But I suspect there is another, deeper issue here–namely, that even without political constraints, advocates of a living wage would not be satisfied with any plan that relies on after-market redistribution.

They don’t want people to “have” a decent income, they want them to “earn” it, not be dependent on demeaning hand-outs…

In short, what the living wage is really about is not living standards, or even economics, but morality. Its advocates are basically opposed to the idea that wages are a market price–determined by supply and demand, the same as the price of apples or coal.

It is most unwise to say there is no evidence of minimum wage increases causing unemployment. That sets a low bar of having to find only one or two studies to refute the claim:

1. Taking his claims as true, why do small businesses lobby against raising the minimum wage?

2. Why did Tom Holmes find in his seminal 1999 JPE paper that manufacturing clusters on the Right to Work Side of state borders and avoids the union side of the border?

3. Why did Erin Mansur and I find the same result in our 2013 paper where we build on Holmes’ paper and show that labour intensive manufacturing industries are even more likely to avoid the union side of the border as they are more likely to locate in the adjacent county in the Right to Work State?

4. The Card-Krueger study is certainly important but the variation they used to estimate their effect is tiny relative to the upcoming doubling of the minimum wage up to $15 in cities such as LA and San Fran. How is Dr. Krugman so sure that he can “extrapolate out of sample” to a policy that has never been tried before? Does he have a valid structural model that he can use to conduct such extreme policy counter-factuals?

Karl Popper would be proud of Krugman’s bold and risky prediction that strictly forbids the existence of any studies showing adverse unemployment effects of minimum wage increases.

The thing to remember is, if there is not doubt in the literature, if there are not some mixed results, the econometricians are simply not trying hard enough to win tenure, secure promotion and be published on the top journals.

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

/cdn0.vox-cdn.com/uploads/chorus_asset/file/3966560/11754389_920572351334762_1285855543300283646_o.jpg)

Recent Comments