Armen Alchian successfully identifying lithium as the fissile fuel in the Bikini Atoll atomic bomb using only publicly available financial data. The early 1954 RAND corporation memo by Alchian was classified a few days later.

The Stock Market Speaks: How Dr. Alchian Learned to Build the Bomb by Joseph Michael Newhard, August 27, 2013 at for a replication study of Alchian’s event study of share market reactions to the Bikini Atoll nuclear detonations in 1954 updated with declassified information and modern finance theory.

An extra challenge for Alchian was not only was the component of the bomb classified, whether the explosion was atomic or hydrogen was classified too.

The share price of the supplier of lithium surged within a few days.

The replication study by Newhard found a significant upward movement in the price of Lithium Corporation relative to the other corporations. Within three weeks of the explosion, its shares were up 48% before settling down to a monthly return of 28% despite secrecy, scientific uncertainty, and public confusion surrounding the test; the company saw a return of 461% for the year.

The share market is a surprising efficient tool for discerning new knowledge.

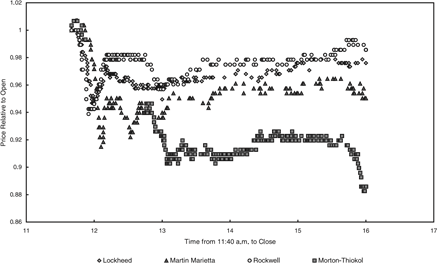

After the Challenger space shuttle disaster in 1986, the share market identified within the hour which component supplier made the faulty part and marked it down accurately as to damages and loss of business. The blue ribbon commission of inquiry took 6-months to find the culprit.

In the period immediately following the crash, securities trading in the four main shuttle contractors singled out Morton Thiokol as having manufactured the faulty component.

Intraday stock price movements following the challenger disaster

At market close, Thiokol’s shares were down nearly 12 per cent. By contrast, the share prices of the three other firms started to creep back up, and by the end of the day their value had fallen only around 3 per cent.

Morton Thiokol shed some $200 million in market value on the day. Over the next several months, the other contractors recovered and outperformed the market while Morton Thiokol lagged.

As a result of the investigation, Morton Thiokol had to pay legal settlements and perform repair work of $409 million at no profit. It also dropped out of bidding for future business.

The $200 million equity decline for Morton Thiokol in hindsight is a reasonable prediction of lost cash flows that came as a result of the judgment of culpability in the crash.

William Brown found that a group of firms that had significant ties to Lyndon Johnson increased in the market value after President Kennedy’s assassination. The share prices of General Dynamics, whose main aircraft plant was located in Fort Worth, Texas, climbed from $23.75 on November 22 to $25.13 on November 26, and by February 1964 was up over $30, a jump of around 30 per cent in three months.

Over the ten trading days following the announcement of Timothy Geithner’s nomination as U.S. Treasury Secretary, financial firms with a connection to Geithner experienced a cumulative abnormal return of about 12% relative to other financial sector firms. This reversed when his nomination ran into trouble due to unexpected tax return issues.

Pat Akey (2013) looked at the abnormal returns in share prices around close U.S. congressional elections. Firms gain on the election of a politician with whom they are connected – and they lost when he or she is defeated. The cumulative abnormal return to be between 1.7% and 6%.

The Right talks of the deserving and undeserving poor. The Left countered with payments to business.

The Right talks of the deserving and undeserving poor. The Left countered with payments to business. Both direct and indirect subsidies to businesses are classified as corporate welfare. The reason is businesses as supposed to make a profit or go out of business.

Both direct and indirect subsidies to businesses are classified as corporate welfare. The reason is businesses as supposed to make a profit or go out of business. A kissing cousin of corporate welfare is farm welfare. These are the countless subsidies that farmers get in Europe and America, and in the past, in New Zealand.

A kissing cousin of corporate welfare is farm welfare. These are the countless subsidies that farmers get in Europe and America, and in the past, in New Zealand. It is pointless to tax the middle-class and then give them their money pretty much straight back as a cash payment for a particular purpose be it child care or for their retirement. Middle-class welfare covers at least in part expenses the middle-class could have covered themselves but for the taxes.

It is pointless to tax the middle-class and then give them their money pretty much straight back as a cash payment for a particular purpose be it child care or for their retirement. Middle-class welfare covers at least in part expenses the middle-class could have covered themselves but for the taxes.

Recent Comments