Short version — reforms Greece is being told to make, and what it's getting on debt relief. uk.businessinsider.com/greece-europea… http://t.co/eNrXu47Elc—

Mike Bird (@Birdyword) July 13, 2015

Was the Chinese share market crash rational asset-price movements without news?

14 Jul 2015 1 Comment

in business cycles, entrepreneurship, financial economics, macroeconomics Tags: competition as a discovery procedure, dot.com bubble, entrepreneurial alertness, event studies, learning by doing, sharemarket bubbles, sharemarket crashes

Large share market crashes such as over the recent months in China and the 1987 Wall Street crash do not necessarily imply an economic slowdown.

As the stock market gets rocked, let's remember this one thing about the crash of 1987 businessinsider.com/lets-remember-… http://t.co/BDgy5h5UN0—

Elena Holodny (@elenaholodny) August 21, 2015

The majority of major share market movements occur without any particular news hitting the market. Studies of the 50 largest share market movements in the US stock market between 1946 and 1987 found that the majority of them could not be explained by news. That includes the 1987 share market crash. In October 1987, shares fell by 20% in one day for no obvious reason.

China's stock market selloff explained in 6 charts bloom.bg/1HStJSe http://t.co/0CpoU21RpY—

Bloomberg Business (@business) July 13, 2015

David Romer explained these booms and busts, including the 1987 share market crash in two ways: investor uncertainty about the quality of other investors’ information; and dispersion of information and small costs to trading:

Asset prices can change because initially the market does an imperfect job of revealing the relevant information possessed by different investors and because developments within the market can then somehow cause more of that information to be revealed…

The possibility of imperfect aggregation implies an alternative to external news and irrationality as a potential source of asset-price movements: some price changes may be caused by “internal” news.

That is, asset prices can change because initially the market does an imperfect job of revealing the relevant information possessed by different investors and because developments within the market can then somehow cause more of that information to be revealed.

Either of these models are perfectly plausible. Investors learn from each other through trading and improve their estimations of the value of various shares.

#China Reality Check: #Stocks Are Still Too Expensive for @MarkMobius bloom.bg/1Monzct via @business @frostyhk http://t.co/e3Lv3KwgTZ—

Fion Li (@fion_li) July 13, 2015

As such, through internal learning and discovery within the share market there can be booms and crashes despite no new information, no communication, and no coordination among the participants in trading. Underneath the surface, there is a gradual updating of information by the participants and at a certain point in time, this causes a sudden change of behaviour.

Dow and Gorton made similar points to David Romer about how share market learning is a process of learning, judgement and error correction rather than an instant adjustment:

Strategic interaction and the complexity of the information result in a protracted price response.

Indeed, equilibrium price paths of the model may display reversals in which the two traders rationally revise their beliefs, first in one direction, and then in the opposite direction, even though no new information has entered the system.

A piece of information which is initially thought to be bad news may be revealed, through trading, to be good news.

Bubbles and crashes are consistent with private information held by a few slowly dispersing among market participants until this knowledge was reflected in stock prices as in Hayek’s (1945) analysis of the price mechanism as a means of communicating information.

HT: The one thing you should remember about the stock market crash of 1987 | Business Insider.

Greek and US great depressions compared

14 Jul 2015 Leave a comment

in business cycles, currency unions, economic growth, economic history, Euro crisis, global financial crisis (GFC), great depression, great recession, job search and matching, labour economics, macroeconomics, unemployment Tags: Greece

https://twitter.com/ianbremmer/status/620570062538309632/photo/1

Greek Depression vs US Depression:

Unemployment http://t.co/81efYi5Ajy—

ian bremmer (@ianbremmer) July 13, 2015

Financial crises surprisingly common, but few countries close their banks

10 Jul 2015 Leave a comment

in business cycles, currency unions, economic history, economics of regulation, Euro crisis, financial economics, global financial crisis (GFC), law and economics, macroeconomics, monetary economics, property rights Tags: bank runs, banking crises, banking panic, financial crises, Greece, sovereign default

Financial crises surprisingly common, but few countries close their banks pewrsr.ch/1NQyz2P #Greece http://t.co/pK0sfB49Ka—

PewResearch FactTank (@FactTank) July 09, 2015

Why Greece joined the Euro

06 Jul 2015 Leave a comment

in applied price theory, applied welfare economics, budget deficits, business cycles, comparative institutional analysis, constitutional political economy, currency unions, economic growth, economic history, Euro crisis, fiscal policy, fisheries economics, global financial crisis (GFC), international economics, macroeconomics, Public Choice, rentseeking Tags: Euro sclerosis, Greece, insurance attacks, sovereign defaults, speculative attacks

The roots of Greece’s crisis are simple. Before Greece joined the Eurozone, investors treated it as a middle-income country with poor governance — which is to say, a credit risk.

After Greece joined the Eurozone, investors thought that Greece was no longer a credit risk — they figured, if push came to shove, other Eurozone members like Germany would bail Greece out. They were wrong.

Michael Dooley put forward a theory of speculative attacks on currencies as insurance attacks on currencies for emerging markets after the East Asian financial crisis:

First generation models of speculative attacks show that apparently random speculative attacks on policy regimes can be fully consistent with rational and well-informed speculative behaviour.

Unfortunately, models driven by a conflict between exchange rate policy and other macroeconomic objectives do not seem consistent with important empirical regularities surrounding recent crises in emerging markets. This has generated considerable interest in models that associate crises with self-fulfilling shifts in private expectations.

In this paper we develop a first generation model based on an alternative policy conflict. Credit constrained governments accumulate reserve assets in order to self-insure against shocks to national consumption. Governments also insure poorly regulated domestic financial markets.

Given this policy regime, a variety of internal and external shocks generate capital inflows to emerging markets followed by successful and anticipated speculative attacks.

We argue that a common external shock generated capital inflows to emerging markets in Asia and Latin America after 1989. Country specific factors determined the timing of speculative attacks. Lending policies of industrial country governments and international organizations account for contagion, that is, a bunching of attacks over time.

His model was not within the context of a currency union but his basic theory is correct.

There are speculative attacks on a currency or a bank run after foreign markets revises their estimates of the available central bank reserves and international lines of credit to bail out the banking systems and/or foreign debt.

Michael Dooley was dealing with the emerging economies of Southeast Asia and their official lines of credit that insure their foreign exchange liabilities and domestic banking system. Greece is about lines of credit for similar purposes to other European union member states.

via 12 charts and maps that explain the Greek crisis – Vox and The Most Important Graphs of 2011 – The Atlantic.

The reason why New Zealand should rule out helping Greece!

06 Jul 2015 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), macroeconomics Tags: bank runs, banking panics, Eurosclerosis, Germany, Greece, sovereign defaults

Greece is a tiny part of the European economies so it doesn’t matter that much to the rest of the European Union what happens to Greece. The only people will notice the sovereign default of Greece once the breathless journalism has died down are Greeks themselves as they rebuild their banking and monetary system against a background of a government run by coffee shop Marxists.

Greece in 7 charts

06 Jul 2015 3 Comments

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, fiscal policy, labour economics, labour supply, macroeconomics, unemployment Tags: Eurosclerosis, Greece

The extreme economic outlier that is Greece, in 7 charts: 53eig.ht/1GMgIFU http://t.co/gb3zkgUqqJ—

(@FiveThirtyEight) July 04, 2015

Gambling for Redemption and Self-fulfilling Debt Crises in the Eurozone

29 Jun 2015 Leave a comment

in business cycles, currency unions, economic growth, Euro crisis, fiscal policy, global financial crisis (GFC), international economic law, international economics, macroeconomics Tags: game theory, Greece, Patrick Kehoe, sovereign default

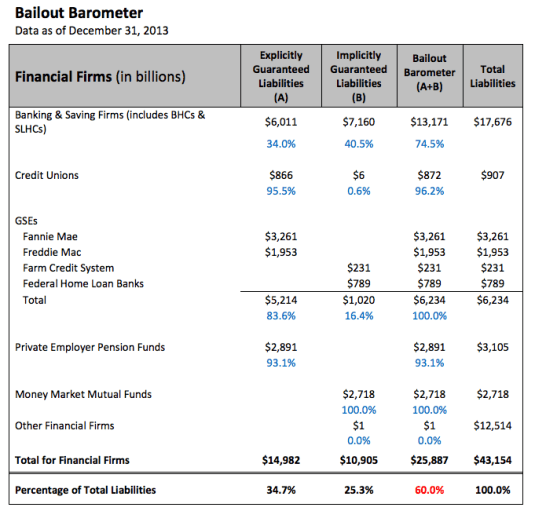

The U.S. bailout barometer.

19 Jun 2015 Leave a comment

in business cycles, financial economics, monetary economics, Public Choice, rentseeking Tags: bailouts, deposit insurance, implicit guarantees, lender of last resort

How great was the Great Depression unemployment? The official and Darby estimates of US unemployment in the 1930s

17 Jun 2015 Leave a comment

in business cycles, economic history, great depression, labour economics, macroeconomics, unemployment Tags: Euro sclerosis, measurement error, Michael Darby

The graph below shows two different series for unemployment in the 1930s in the USA: the official BLS level by Lebergott; and a data series constructed famously by Michael Darby.

Figure 1: US unemployment rate, 1929 – 40: Darby and Lebergott estimates

Source: Robert Margot (1993).

Darby includes workers in the emergency government labour force as employed – the most important being the Civil Works Administration (CWA) and the Works Progress Administration (WPA). Once these workfare programs are accounted for, the level of U.S. unemployment fell from 22.9% in 1932 to 9.1% in 1937, a reduction of 13.8%.

For 1934-1941, the corrected unemployment levels are reduced by two to three-and-a half million people and the unemployment rates by 4 to 7 percentage points after 1933.

Not surprisingly, Darby titled his 1976 Journal of Political Economy article Three-and-a-Half Million U.S. Employees Have Been Mislaid: Or, an Explanation of Unemployment, 1934-1941. The corrected data by Darby shows stronger movement toward the natural unemployment rate after 1933.

From about 1935, the unemployment rate in the Great Depression in the USA is not much different from what it is in Europe in recent decades under Eurosclerosis.

In the 1930s in the USA, many unemployed were employed by the Civil Works Administration and the Works Progress administration. In contemporary Europe, the unemployed are simply paid not to work under their welfare state arrangements.

If You’re A Keynesian Then You Must Believe The Minimum Wage Increases Unemployment

14 Jun 2015 Leave a comment

in business cycles, fiscal policy, labour economics, macroeconomics, minimum wage Tags: Bryan Caplan, economic fallacies, involuntary unemployment, Keynesian macroeconomics, methodology of economics, wage rigidity

Via If You’re A Keynesian Then You Must Believe The Minimum Wage Increases Unemployment and The Myopic Empiricism of the Minimum Wage, Bryan Caplan | EconLog | Library of Economics and Liberty.

The US share market since 1900

10 Jun 2015 Leave a comment

in business cycles, economic growth, economic history, entrepreneurship, financial economics, macroeconomics Tags: active investing, efficient market hypothesis, entrepreneurial alertness, passive investing

Here’s how Warren Buffett sees the stock market read.bi/1HsUe1p http://t.co/Zm6fDTYpf9—

BI Chart of the Day (@chartoftheday) April 23, 2015

The Spanish economic recovery compared

10 Jun 2015 Leave a comment

in business cycles, currency unions, economic growth, Euro crisis, global financial crisis (GFC), great recession, macroeconomics Tags: Eurosclerosis, France, Germany, Italy, Spain

Spain's economic growth is being touted as a success story. Don't tell the Spaniards: on.wsj.com/1M45yzI http://t.co/pm4DAd1qkF—

Nick Timiraos (@NickTimiraos) June 03, 2015

The global business cycle in one chart

05 Jun 2015 Leave a comment

in business cycles, economic growth, macroeconomics Tags: world economy

The entire global economy. In one chart. bloom.bg/1FrXQ1A http://t.co/H07P9n2LkL—

Bloomberg VisualData (@BBGVisualData) May 22, 2015

Growth accounting for the USA in the 1930s

05 Jun 2015 Leave a comment

in business cycles, economic growth, economic history, great depression, macroeconomics Tags: great depression, growth accounting, real business cycles

Notice how productivity recovers but hours worked per working age adults does not.

via The Current Financial Crisis in Spain: What Should We Learn from the ….

Recent Comments