Tirole on the economics of crises

05 Nov 2019 Leave a comment

in applied price theory, budget deficits, business cycles, currency unions, development economics, economics of information, entrepreneurship, Euro crisis, global financial crisis (GFC), industrial organisation, international economics, macroeconomics, market efficiency, monetary economics, Public Choice, rentseeking Tags: bank panics

Only rational expectations macroeconomics can explain self-fulfilling crises

01 Nov 2019 Leave a comment

in applied price theory, budget deficits, business cycles, currency unions, economic growth, economic history, economics of bureaucracy, economics of information, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, monetary economics, Public Choice Tags: Euroland, rational expectations, sovereign defaults

Quinto Congreso Internacional FIAP – Asofondos – Edward Prescott

03 Aug 2019 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, Edward Prescott, Euro crisis, fiscal policy, global financial crisis (GFC), macroeconomics, monetary economics Tags: real business cycles

Uncertainty and Ambiguity in American Fiscal and Monetary Policies Thomas Sargent

28 May 2019 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, economic history, economics of information, Euro crisis, financial economics, fiscal policy, geography, global financial crisis (GFC), great depression, great recession, law and economics, macroeconomics, monetary economics Tags: Thomas Sargent

Thomas J. Sargent speaks on Euro Crisis

18 May 2019 Leave a comment

in applied price theory, budget deficits, business cycles, currency unions, economic growth, economic history, economics of bureaucracy, economics of information, economics of regulation, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great recession, history of economic thought, international economics, International law, law and economics, macroeconomics, monetary economics, property rights, Public Choice, public economics, rentseeking Tags: moral hazard, sovereign debt crises, sovereign defaults, Thomas Sargent

Thomas Sargent Emergency Economic Summit for Greece: Part 2

18 May 2019 Leave a comment

in applied price theory, budget deficits, business cycles, comparative institutional analysis, constitutional political economy, currency unions, economic growth, economic history, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, income redistribution, law and economics, macroeconomics, monetary economics, politics - USA, property rights, Public Choice, public economics, rentseeking Tags: sovereign defaults, Thomas Sargent

Tom Sargent Honorary Degree Lecture on the Eurocrisis

16 May 2019 Leave a comment

in budget deficits, business cycles, comparative institutional analysis, currency unions, economic growth, economic history, economics of bureaucracy, Euro crisis, financial economics, global financial crisis (GFC), great recession, history of economic thought, law and economics, macroeconomics, monetary economics, politics - USA, Public Choice, public economics, rentseeking Tags: banking panics, moral hazard

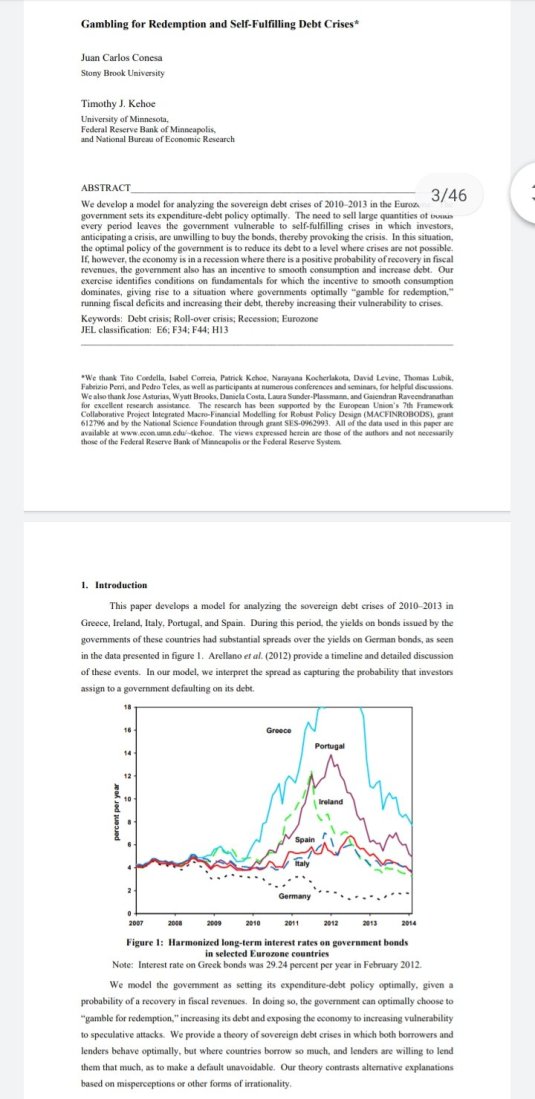

Gambling for Redemption and Self-fulfilling Debt Crises

06 May 2019 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, economic history, Euro crisis, financial economics, global financial crisis (GFC), great depression, great recession, international economic law, International law, law and economics, macroeconomics, monetary economics, Public Choice, rentseeking Tags: banking panics, sovereign debt crises

The temptation — and perils — of inconsistent policy: Finn Kydland at TEDxCibeles

29 Oct 2018 Leave a comment

in applied price theory, budget deficits, business cycles, comparative institutional analysis, currency unions, economic growth, macroeconomics

Jonn Cochrane Says Allowing European Defaults `Best’ for Euro

04 Oct 2018 Leave a comment

in budget deficits, business cycles, currency unions, Euro crisis, financial economics, law and economics, macroeconomics, monetary economics, property rights Tags: sovereign defaults

Recent Comments