Celebrating humanity's flourishing through the spread of capitalism and the rule of law

13 Jan 2015 Leave a comment

in economic growth, liberalism, macroeconomics Tags: Eurosclerosis

13 Jan 2015 2 Comments

in business cycles, economic growth, economic history, labour economics, labour supply, macroeconomics, monetarism Tags: Japan, Japanese banking system, Lost Decade

When I lived in Japan between 1995 and 1997, they are undergoing the transition from a six-day week to a five day week. At the time, workers at my University had to show up on Saturday morning. They then went home at lunchtime. Saturday morning at the office was phased out a few years later.

In explanations of the Lost Decade of growth in Japan dating from the early 1990s, with the exception of Ed Prescott, the explanation that the Japanese simply chose to produce less per worker over the course of the 1990s does not figure highly.

The Japanese working week was reduced by law from 48 to 44 hours per week in 1988 and further reduced by the same labour standards law to 40 hours per week from 1993 (Prescott 1999; Hayashi and Prescott 2002). The Japanese stopped routinely working on Saturdays over the 1990s. The number of national holidays was increased by three and an extra day of annual leave was also prescribed by law.

Figure 1 shows this regulatory change about the length of the standard working week that started in 1987 was followed by a sharp drop in hours worked per working per working age Japanese over the period 1988 to 1993. The Japanese working age population is defined as those aged 20 to 69 (Hayashi and Prescott 2002).

Figure 1: Weekly hours worked per Japanese aged 20 to 69, 1970-2000

Source: Hayashi and Prescott 2002.

The regulatory process to end the standard six day working week in Japan straddled the start of the Lost Decade. This major change in the regulation of the supply of labour per week in the number of hours worked and the stagnation of GDP growth soon after could be more than a coincidence (Prescott 1999; Hayashi and Prescott 2002).

Americans work more hours a year than workers in Japan. But both work less than before. Data: buff.ly/1LhU5gH http://t.co/7oaGYKLRmk—

HumanProgress.org (@humanprogress) August 18, 2015

More employment did not fill the short-fall in weekly labour supply per worker after the introduction of the 44 hour week and then the 40 hour week in Japan. Many offices and factories closed on Saturday rather than employ more to make up the hours. The regulatory change was a clear cut constraint on the length of the working week that was hard to get around because of the need to recruit a separate set of workers to come in on Saturday afternoon and then all day Saturday.

During the transition to a five day working week, Japanese real GDP growth should slow down because output levels must taper during a transitional period because one day per week less in labour is supplied in production and capital is being worked for one day a week less than before (Prescott 1999; Hayashi and Prescott 2002).

Output per working age person depends on capital-labour ratios, on hours worked per week and on changes in total factor productivity due to factors such as technological progress and changes in institutions and economic policies.

The effects of the change in the length of the working week on output per working age Japanese will persist for a significant time because investment plans and the capital stock must also adjust to a shorter working week. This is another example of a highly persistent shock that can partly account for the Lost Decade. As Prescott (1999) observed:

Given the change in Japanese law and the resulting drop in normal market hours, growth theory predicts the almost stagnant output of the Japanese economy in the 1990s. This reduction in market hours lowered the marginal product of capital, making investment unprofitable.

Given the lack of profitable domestic investment opportunities, the Japanese began saving by investing abroad. This explains Japan’s large trade surpluses

…The Japanese economy in the 1990s is not as depressed as the U.S. economy was in the 1930s. Market hours in Japan in the 1990s have fallen only half as much as market hours fell in the United States during the Great Depression.

More importantly, the reduction in market hours in Japan in the 1990s was the stated objective of policy.

The reduction in weekly hours worked will also reduce the working week of capital because labour and capital are usually complementary inputs. The reduced length of the working week will see some existing capital producing less, some capital will go spare, and the rate of wear and depreciation will fall.

The drop in weekly hours worked will lower the marginal productivity of existing and new capital which will make new capital investments in Japan less profitable than before. Net investment will be less while the Japanese capital stock is adjusting down to the reduced working week for capital and labour.

Measured total factor productivity will fall because of an under-utilisation of a capital stock that is now larger than required for the available labour force. Net investment will decline by a large amount because investment demand is a small yearly addition to the capital stock.

For example, if annual investment demand is 5 per cent of the capital stock, and the desired capital stock becomes 1 per cent smaller than previous, annual net investment will fall 20 per cent. GDP growth will resume at the trend rate once the lower level of output per working age person is reached.

For those that still doubt, consider the contrary, what would you expect to happen in your country moved from five day week before day working week? Do you expect workers to produce as much as before? Britain was on a three day working week during the coal miners’ strike. As expected, output fell because the working week was shorter.

The main gap in the English language literature about the reduction in the working week in Japan is a lack of publications I can find by Japanese economists discussing what predictions of a made about the likely consequences for output, investment and productivity before the reduction in the length of working week was legislated. Did the reduction in the length of the working week in Japan turn out as planned and predicted before it was implemented?

France introduced a 35 hour week some years ago. Although there were various options for over time, albeit strictly regulated, a uniform prediction was that the 35 hour week would reduce productivity. The new workweek was phased in slowly, with large firms adopting it in February 2000 and smaller firms doing so only in January 2002.

French employees were expected to bear only a small part of the cost of the working-time reduction, continuing to earn roughly the same monthly income – in line with the unions’ slogan ’35 hours pays. To ease that transition, the law reduced the overtime premium for small firms and increased their annual limit on overtime work compared with large firms.

The reduction in the length of the French working week failed as work sharing strategy and reduced productivity. This was a fair summary by the IMF:

The 35-hour workweek appears to have had a mainly negative impact. It failed to create more jobs and generated a significant—and mostly negative—reaction both from companies and workers as they tried to neutralize the law’s effect on hours of work and monthly wages.

While it cannot be ruled out that individuals who did not change their behaviour because of the law became more satisfied with their work hours, simple survey measures do not show increased satisfaction.

Between 1997 and 2000, Quebec reduced its standard workweek from 44 to 40 hours to stimulate jobs growth – the old work sharing ideal. The Quebec policy contained no suggestion or requirement that employers provide wage increases to compensate workers for lost hours.

Despite a 20% reduction among full-time workers in weekly hours worked beyond 40, the policy failed to raise employment at the provincial level or within industries. If anything, there were job losses.

Japan was the only case where a reduction in the length of the working week met with wide approval by the public and people simply stopped working on Saturdays. The law succeeded simply because it did but it was designed to do: reduce the number of days existing workers worked. Japan was undergoing mild deflation at the time, so the need to reduce wages was minimal.

Annual hours worked per employed Japanese has continued to slowly taper down since the late 1990s, which may be a further explanation of its continual slow growth.

David Andolfatto wrote a nice paper explaining the consequences for the financial and monetary sectors of this reduction in the length of the Japanese working week:

In his analysis, David Andolfatto referred generally to a productivity slowdown as discussed by Prescott rather than to the specifically to the reduction in the length of the Japanese working week. Nothing detracts in his analysis, as Andolfatto said, that Japan has a problem: lagging productivity growth and as Andolfatto concluded:

…monetary and fiscal policies, or reforms directed exclusively at the banking sector, are unlikely to re-establish productivity growth. What is likely needed are economy-wide reforms that enhance the willingness and ability of individuals to adopt potentially disruptive technological advancements and work practices.

20 Dec 2014 1 Comment

in economic growth, macroeconomics, politics - New Zealand Tags: lost decades

The World Bank published a major 300 odd page report that discussed puzzles of economic growth around the world included a chapter on New Zealand’s slow economic growth relative to Australia.

The World Bank publication is copyrighted 2015, so I assume that it has been published very recently. However, the data analysis in the chapter on New Zealand stop in 2002.

The conclusions of the World Bank with regard to the emergence of the trans-Tasman income gap were as follows:

The extent of economic freedom—as determined by propelling institutions—evolved in a similar manner in both countries.

The small differences in propelling institutions in both countries mostly netted out and as such cannot account for the differences in economic performance.

One exception was the fiscal position of the state—a rise in public expenditure after the first oil crisis entailed increased tax burdens in both countries.

A particularly sharp rise in taxation in New Zealand (in comparison to Australia) occurred during the country’s second downturn.

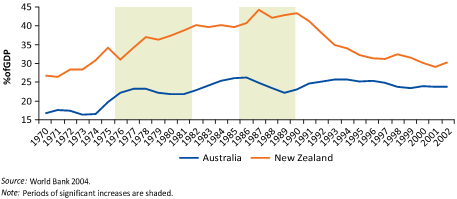

Differences in the size of the public sector figure prominently in the analysis of the World Bank of the emergence of the trans-Tasman income gap. The measure by the World Bank of the size of the public sector in New Zealand and Australia is reproduced below – its figure 3.3.

Figure 3.3 Government expenditure in Australia and New Zealand, 1970–2002

In particular, the World Bank was concerned about the rapid growth in the size of the public sector in New Zealand while the size of the public sector was shrinking in Australia:

In 1977–82 Australia’s government expenditure rose more slowly than that of New Zealand (and in 1975–80 Australia’s expenditure was smaller than New Zealand’s by 13 percent of GDP.

Then, as relative economic growth declined in New Zealand, between 1987 and 1990 public expenditure increased by around 5 percent of GDP from the 1982–86 level. In the meantime, public expenditure in Australia fell by 4 percent of GDP.

As a result, the difference in the general government expenditure level between New Zealand and Australia increased to over 18 percent of GDP in 1987–90.

After 1990 and until 2002 government spending in New Zealand decreased steadily—from approximately 44 percent of GDP in 1990 to roughly 30 percent of in 2002.

In Australia this expenditure was maintained at an average of 25 percent of GDP over the same period (see figure 3.3 with highlighted periods of significant increases of government expenditures in New Zealand).

A spike in the size of state sector in the 1980s may explain a delay in productivity growing rapidly again, but the state sector in New Zealand is now smaller.

Indeed, figure 3.3 above shows that the public sector in New Zealand as measured by general government expenditure has fallen by a quarter in size, by 10 percentage points of GDP in a matter of seven years between 1990 and 1996. There should be rapid growth because of the greatly reduced crowding out by the state sector but that rapid growth is not there.

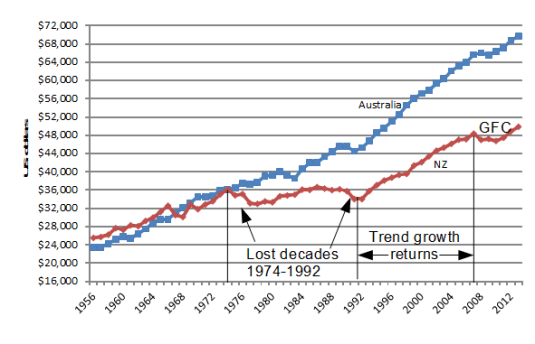

Figure 2 shows that GDP growth per working age New Zealander resumed at its trend rate of 2% after 1992. This resumption of growth was in conjunction with the decline in the size of public sector tax burden rather than after it. Figure 2 shows that there was no significant growth in real GDP per working age New Zealander from 1974 to 1992. New Zealand lost almost two decades of productivity growth. Real GDP per New Zealander aged 15-64 on a purchasing power parity basis dropped from equality with Australia up until 1974 to a 30 per cent gap by 1992.

Figure 2: Real GDP per New Zealander and Australian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1956-2012

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

There was no growth rebound when the burden of an oversized public sector was lifted. That is the greater puzzle. The World Bank did not address that greater puzzle. If there is a global pool of useful technological knowledge accessible at a low cost by suitably prepared people, what stops New Zealand from using this knowledge to grow faster until it catches-up with Australia and the USA?

Another puzzle for the World Bank is that it is using general government expenditure estimates by the OECD.

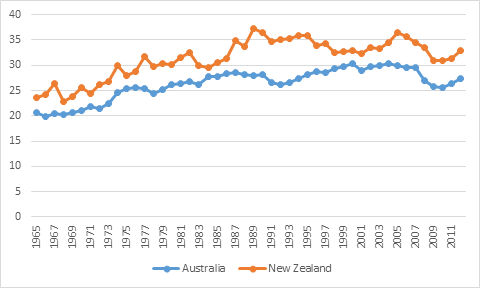

When tax revenue as a percentage of GDP is used to measure the size of the public sector and the burden on private sector initiative, figure 3 shows that the tax burden in the two countries is not that different and is in the low 30% range, not the 40% plus range as is suggested by the general government expenditure data in Figure 3.3.

Figure 3: tax revenue as a percentage of New Zealand and Australian GDP, 1965-2011

Source: OECD Stats

There are no 14 point gaps in tax burdens in figure 3 as suggested in the World Bank’s analysis. This is because the World Bank’s using general government expenditure shown in its figure 3.3 reproduced above.

A major conclusion about the causes of New Zealand’s poor growth performance in the last few decades should be robust to different measures of the size of the public sector, but it is not.

Economic reforms returned real GDP growth per New Zealander aged 15-64 from no growth from 1974 to 1992 to the previous two per cent trend rate from 1993. There was no sustained productivity growth rebound beyond 2 per cent growth a year for New Zealand to recover the lost ground in the 1980s and 1970s. That is the great puzzle that the World Bank did not address, much less solve.

18 Dec 2014 Leave a comment

in business cycles, economic growth, entrepreneurship, job search and matching, macroeconomics Tags: real business cycles

Revisions in investor beliefs about productivity prospects can partly account for business expansions and contractions. If favourable news about future technological opportunities can seed a boom today in consumption and investment before the actual technological improvement arrives and is realised, news that future productivity growth may not be as good as was previously expected can induce a recession without any actual change in productivity ever occurring.

Investors build in anticipation, starting new projects and recruiting more staff. Their forecasts can turn out to be too optimistic. When entrepreneurial expectations of future productivity are revised, investment demand can fall because of an excess in capital accumulation – recent investments were made under more optimistic beliefs about productivity (Beaudry and Portier 2004).

Investment demand must be muted for a time until the excess capital accumulation is brought into use, refitted or scraped. There also will be layoffs and a lull in recruitment. Job search strategies must also change as job seekers redirect their careers in light of the news about their revised prospects in different firms, industries and competing occupations.

The optimism and pessimism of investors are rational profit-seeking responses to new entrepreneurial knowledge. Profit expectations reflect consumer preferences, resource constraints and technological factors as they exist and are forecast to change and actual and forecasted opportunities and constraints in the investment sector. Entrepreneurs are dynamic risk takers who profit from anticipating shifts in consumer demand, input costs and technology.

Recessions and booms can arise due to the challenges facing entrepreneurs in forecasting the uncertain and ever-changing future demand for new capital that is implied by their forecasts of consumer demand and technological opportunities as Beaudry and Portier (2004) explain:

The view that recession and booms may arise as the result of investment swings generated by agents’ difficulties to properly forecast the economy’s need in terms of capital has a long tradition in economics.

For example, this difficulty was seen by Pigou as being an inherent feature of any economy with technological progress.

As emphasized in Pigou (1926), when agents are optimistic about the future and decide to build up capital in expectation of future demand then, in the case where their expectations are not met, there will be a period of retrenched investment which is likely to cause a recession.

Revisions in entrepreneurial beliefs and investment plans can be required when new information is uncovered (Beaudry and Portier 2004; Sill 2009). There can be lulls in investment demand following these revisions to entrepreneurial forecasts leading to recessions. As Pigou noted in 1927:

The varying expectations of business men … constitute the immediate cause and direct causes or antecedents of industrial fluctuations

17 Dec 2014 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, monetarism, monetary economics Tags: bank runs, GFC, great depression, great recession, Robert E. Lucas

15 Dec 2014 Leave a comment

Source: Edward Prescott

15 Dec 2014 Leave a comment

in economic growth, macroeconomics, politics, Public Choice Tags: Edward Prescott, Japan

the ruling bloc secured a two-thirds supermajority in the 475-seat House of Representatives, giving it the power to override the Upper House.

When I arrived in Japan in 1995, the LDP was out of power and written off.

The LDP were true stayers in politics. They managed to get back into power soon after the 1995 general election by forming a coalition with the Socialist party.

The Socialist party leader was initially the Prime Minister then he resigned later and was replaced by an LDP Prime Minister.

The grip on power of the LDP was consolidated by the great competence of the Koizumi administration.

Source: Edward Prescott

The LDP lost power again in about 2007 but regained power in the next election through the extreme incompetence of their opposition.

In the current election, the main opposition party were unable even to put up enough candidates to actually win a majority.

The key contribution of the main opposition parties in Japan was well stated when they last won an election in 2007. They have shown that they can actually win an election when the LDP performs poorly. That is an important discipline that may not have been there in the 1980s.

via Abe’s snap election pays off with big win for LDP | The Japan Times.

13 Dec 2014 Leave a comment

in business cycles, economic growth, global financial crisis (GFC), great recession, macroeconomics Tags: GFC, top 1%

Figure 1. Change in loans versus changes in top 1% income shares, 14 countries, 1972–2008

via Does inequality lead to a financial crisis? | VOX, CEPR’s Policy Portal.

12 Dec 2014 1 Comment

in economic growth, fiscal policy, macroeconomics, Robert E. Lucas Tags: ideas and growth, Robert E. Lucas

12 Dec 2014 Leave a comment

10 Dec 2014 1 Comment

in economic growth, Edward Prescott, Euro crisis, great depression, job search and matching, labour economics, macroeconomics, Robert E. Lucas, unemployment Tags: Eurosclerosis, great depression, voluntary unemployment

Most Keynesian economists are convinced that something exists called involuntary unemployment and people can be unemployed through no fault of their own. They will accept the going wage but no employer is willing to offer it to them.

Lucas and Rapping’s (1969) paper, “Real Wages, Employment, and Inflation” provides the micro-foundations for an analysis of the labour suppl. They felt the need to reconcile the existence of unemployment with market clearing and referred to recent work of Armen Alchian (1969) on search explanations of unemployment.

Lucas and Rapping viewed unemployment as voluntary, including the mass unemployment during the great depression (Lucas and Rapping 1969: 748).

Lucas and-Rapping viewed current labour demand as a negative function of the current real wage. Current labour supply was a positive function of the real wage and the expected real interest rate, but a negative function of the expected future wage.

Under their framework, if workers expect higher real wages in the future or a lower real interest rate, current labour supply would be depressed, employment would fall, unemployment rise, and real wages increase.

Lucas and Rapping depicted labour suppliers as rational optimisers who engaged in inter-temporal substitution: working more when current wages were high relative to expected wages. The prevailing Keynesian approach assumed labour supply was passive, and movements in the demand for labour determined changes in employment.

Lucas and Rapping offered an unemployment equation relating the unemployment rate to actual versus anticipated nominal wages, and actual versus anticipated price levels. Unemployment could be the product of expectational errors about wages.

Lucas and Rapping’s model was poor at explaining unemployment after 1933 in terms of job search and expectational errors.

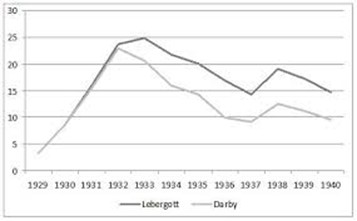

The graph below shows two different series for unemployment in the 1930s in the USA: the official BLS level by Lebergott; and a data series constructed famously by Darby. Darby includes workers in the emergency government labour force as employed – the most important being the Civil Works Administration (CWA) and the Works Progress Administration (WPA).

Once these workfare programs are accounted for, the level of U.S. unemployment fell from 22.9% in 1932 to 9.1% in 1937, a reduction of 13.8%. For 1934-1941, the corrected unemployment levels are reduced by two to three-and-a half million people and the unemployment rates by 4 to 7 percentage points after 1933.

Not surprisingly, Darby titled his 1976 Journal of Political Economy article Three-and-a-Half Million U.S. Employees Have Been Mislaid: Or, an Explanation of Unemployment, 1934-1941.

The corrected data by Darby shows stronger movement toward the natural unemployment rate after 1933. Darby concluded that his corrected date are suggests that the unemployment rate was well explained by a job search model such as that by Lucas and Rapping together with the wage fixing under the New Deal that kept real wages up and unemployment high.

Both the Keynesian approach to unemployment and the job search approach to unemployment view workers in emergency government work programs as employed and not as unemployed.

In the late 1970s, Modigliani dismissed the new classical explanation of the U.S. great depression in which the 1930s unemployment was mass voluntary unemployment as follows:

Sargent (1976) has attempted to remedy this fatal flaw by hypothesizing that the persistent and large fluctuations in unemployment reflect merely corresponding swings in the natural rate itself.

In other words, what happened to the U.S. in the 1930’s was a severe attack of contagious laziness!

I can only say that, despite Sargent’s ingenuity, neither I nor, I expect most others at least of the nonMonetarist persuasion,. are quite ready yet. to turn over the field of economic fluctuations to the social psychologist!

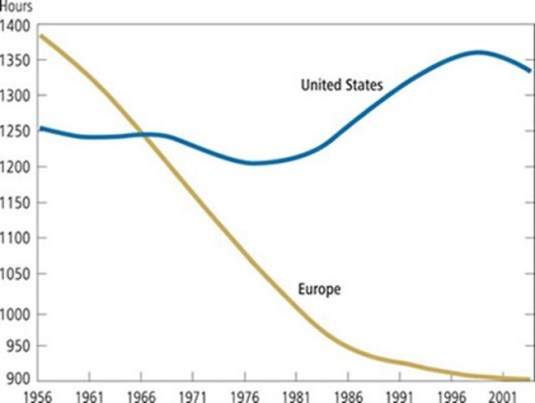

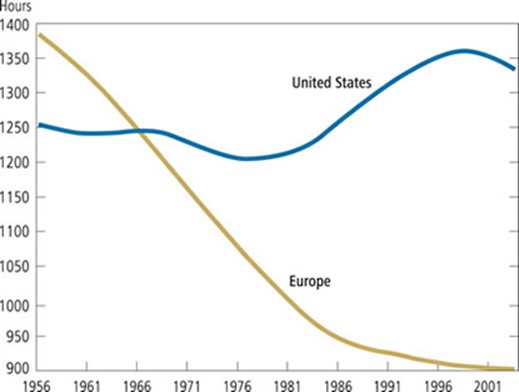

As Prescott has pointed out, the USA in the Great Depression and France since the 1970s both had 30% drops in hours worked per adult. That is why Prescott refers to France’s economy as depressed. The reason for the depressed state of the French (and German) economies is taxes, according to Prescott:

Virtually all of the large differences between U.S. labour supply and those of Germany and France are due to differences in tax systems.

Europeans face higher tax rates than Americans, and European tax rates have risen significantly over the past several decades.

In the 1960s, the number of hours worked was about the same. Since then, the number of hours has stayed level in the United States, while it has declined substantially in Europe. Countries with high tax rates devote less time to market work, but more time to home activities, such as cooking and cleaning. The European services sector is much smaller than in the USA.

Time use studies find that lower hours of market work in Europe is entirely offset by higher hours of home production, implying that Europeans do not enjoy more leisure than Americans despite the widespread impression that they do.

Richard Rogerson, 2007 in “Taxation and market work: is Scandinavia an outlier?” found that how the government spends tax revenues when assessing the effects of tax rates on aggregate hours of market work:

Examining how tax revenue is spent is central to understanding labour supply effects:

Others such as Blanchard attribute the much lower labour force participation in the EU since the 1970s to their greater preference for leisure in Europe. An increased preference for leisure is another name for voluntary unemployment.

The lower labour force participation in higher unemployment in Europe is voluntary because of the higher demand for leisure among Europeans. According to Blanchard:

The main difference [between the continents] is that Europe has used some of the increase in productivity to increase leisure rather than income, while the U.S. has done the opposite.

An unusual left-right unity ticket emerged to explain the great depression in the 1930s and the depressed EU economies from the 1970s: the great vacation theory.

10 Dec 2014 2 Comments

in economic growth, economics, economics of education, human capital, labour supply, occupational choice, politics - Australia, politics - New Zealand, politics - USA, poverty and inequality Tags: financing constraint on education, inequality and economic growth, poverty and inequality, student loans, taxation and the labour supply, top 1%

Figure 1: Estimated consequences of changes in inequality (1985 – 2005) on subsequent cumulative growth (1990-2010)

Drawing on harmonised data covering the OECD countries over the past 30 years, the econometric analysis suggests that income inequality has a negative and statistically significant impact on subsequent growth.

In particular, what matters most is the gap between low income households and the rest of the population.

In contrast, no evidence is found that those with high incomes pulling away from the rest of the population harms growth.

The paper also evaluates the “human capital accumulation theory” finding evidence for human capital as a channel through which inequality may affect growth.

Analysis based on micro data from the Adult Skills Survey (PIAAC) shows that increased income disparities depress skills development among individuals with poorer parental education background, both in terms of the quantity of education attained (e.g. years of schooling), and in terms of its quality (i.e. skill proficiency).

Educational outcomes of individuals from richer backgrounds, however, are not affected by inequality.

via Trends in Income Inequality and its Impact on Economic Growth – Papers – OECD iLibrary.

The OECD analysis published overnight in Paris suggest that the increase in equality in New Zealand the late 1980s is still scarring economic growth today by about 15 percentage points in lost cumulative economic growth.

The analysis of the OECD published overnight depends crucially upon how greater inequality reduces the ability of the lower income families to invest in human capital:

The evidence strongly suggests that high inequality hinders the ability of individuals from low economic background to invest in their human capital, both in terms of the level of education but even more importantly in terms of the quality of education.

The OECD theory of inequality and lower growth is there is a financing constraint because of inequality that reduces economic growth because of less human capital accumulation by lower income families.

This is interesting because in 2002, with Pedro Carneiro, James Heckman showed that lack of credit is not a major constraint on the ability of young Americans to attend college. They found that credit constraints prevent, at most, 4% of the U.S. population from attending. Credit constraints is weakening as a rationale for a lack of an accumulation of human capital, and can be easily solved.

The OECD is putting a lot of their growth inequality nexus eggs in one basket. That student loans and other government interventions are not closing credit constraints on financing higher education.

To add to that basket , they are placing a lot of weight in human capital as a driver of growth, and in New Zealand’s case, of technology absorption, which is a main foundation of economic growth in New Zealand. The evidence that human capital is a key contributor to higher economic growth is weakening ruck rather than strengthening.

The trend rate of productivity growth did not accelerate over the 20th century despite a massive rise in investments in human capital and R&D because of the rising cost of discovering and adapting new technological knowledge. The number of both R&D workers and highly educated workers increased many-fold over the 20th century in New Zealand and other OECD member countries including the global industrial leaders such as the USA, Japan and major EU member states.

Higher education has been free for the low income families for several generations. Student loans are readily available. It is hard to believe that such a readily solvable problem is a major source of inequality and lower growth.

Cross-country differences in total factor productivity are due to differences in the technologies that are actually used by a country and the degree in the efficiency with which these technologies are used. Differences in total factor productivity, rather than differences in the amount of human capital or physical capital per worker explain the majority of cross-country differences in per capita real incomes (Lucas 1990; Caselli 2005; Prescott 1998; Hall and Jones 1999; Jones and Romer 2010).

Differences in the skills of the individual worker or in the total stock of human capital of all workers in a country cannot explain cross national differences in value added per worker at the industry level.

The USA, Japan, France, the UK and Germany all have relatively well-educated, experienced and tested labour forces. For example, the 1993 McKinsey’s study inquired into the education and skills levels of Japanese and German steel workers. Comparably skilled German steel workers were half as productive as their Japanese counterparts (Prescott and Parente 2000, 2005).

As for the source of the growing income inequality, there is a long literature dating back 25-years arguing that skill-biased technological change is increasing the returns to investing in education

Important is the OECD conclusion that inequality in terms of the rich getting richer does not harm growth. To make sure I have not misquoted them , I quote once again from their abstract, where the OECD summarises its own findings:

Drawing on harmonised data covering the OECD countries over the past 30 years, the econometric analysis suggests that income inequality has a negative and statistically significant impact on subsequent growth.

In particular, what matters most is the gap between low income households and the rest of the population.

In contrast, no evidence is found that those with high incomes pulling away from the rest of the population harms growth.

That conclusion of the OECD almost saves me from having to go on about how inequality has not increased in New Zealand for the last 20 years, see figure 2, and that the top 1% have not increased their share of income in recent decades – see figure 3. The fact that the rich can get richer without harming the poor is an important conclusion that will surely not be reported by the media.

Figure 2: Gini coefficient New Zealand 1980-2015

Figure 3: Top 1% income shares, USA, New Zealand and Australia, 1970-2012

Another inconvenience for the OECD is the last major increase in Gini coefficient in New Zealand was followed by a 15 year economic firm – see figures 2 and 4.

Figure 4: Real GDP per New Zealander and Australian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1956-2013

The NZ top 1% share has been steady at 8-9% since the mid-1990s see figure 4; the top 1%’s share rose strongly in the USA in recent decades, from 13% in the mid-1980s to 19% in 2012.

The Occupy crowd blame everything from the global financial crisis to a bad environment on growing inequality and the growing riches of living top 1%. Such an argument has no foundation in fact in New Zealand. The last major increase in Inequality was a long time ago in New Zealand.

The OECD is also rather casual about how policies to redistribute wealth and increasing incomes. While Western Europe is diverse, as a group, the higher taxes in the European Union reduced incentives to work. Employment as a percentage of the population has been consistently lower in Western Europe than in the USA since the 1950s, with an average employment rate gap of 10 percentage points over 1980-2007.

Large increases in taxes on income from labour since the 1970s, enhanced incentives for retire early, and the interaction of generous employment insurance with the larger skill losses among workers displaced by the greater economic turbulence since 1980 all acted to reduce both real GDP and hours worked per week per working age person by up to a third in Western Europe as compared to the USA since the 1970s (Prescott 2004, 2007; Rogerson 2006, 2008; Ohanian et al. 2008; Ljungqvist and Sargent 1998, 2007, 2008). For example, Ohanian, Rao and Rogerson 2008 in “Work and taxes: allocation of time in OECD countries” found that:

Europeans pay more taxes, work fewer hours per year, have longer vacations, retire sooner, and invest less in human capital in an era in which trends in technology have significantly increased the demand for skilled workers, more innovation, more intense competition and greater entrepreneurial alertness. In The Impact of Labor Taxes on Labor Supply: An International Perspective (AEI Press, 2010) Rogerson finds that:

• a 10 percentage point increase in the tax rate on labour leads to a 10 to 15 per cent decrease in hours of work.

• Even a 5 per cent decrease in hours worked would mean a decline in labour output equating to a serious recession.

• While recessions are temporary, permanent changes in government spending patterns have long-lasting repercussions.

• Although government spending provides citizens with important benefits, such benefits must be weighed against the disincentive effects of increased labour taxes.

• Policymakers who fail to account for the decrease in labour output risk expanding government programs beyond their optimal scale.

Robert Lucas estimated in 1990 that eliminating all taxes on income from capital would increase the U.S. capital stock by about 35% and consumption by 7%.

Hans Fehr, Sabine Jokisch, Ashwin Kambhampati, and Laurence J. Kotlikoff (2014) found that eliminating the corporate income tax completely would raise the U.S. capital stock (machines and buildings) by 23%, output by 8% and the real wages of unskilled and skilled workers each by 12%.

In summary, this one paper by the OECD, which is a working paper makes profound conclusions about taxation and economic growth that contradict a large literature based on the lack of statistical significance of coefficients in the OECD’s regressions.

More fundamentally, linking lower economic growth to inequality through credit constraints on the human capital accumulation of the lower middle class is a weak reed to hang its argument. Human capital is not a good explanation of variations in growth across time or between countries.

What happened to income inequality in New Zealand in the late 1980s is not a credible explanation for lower growth 30 years later. Lower economic growth because of greater inequality is certainly an easy problem to solve if all that is required is more action on the financing constraint on human capital accumulation.

08 Dec 2014 Leave a comment

in applied welfare economics, economic growth, economic history, entrepreneurship Tags: 10-90 lag, international technology diffusion, technology diffusion, technology usage lags

Deigo Comin has been doing excellent work documenting both the length of 10-90 technology lags even for major technologies we now take for granted, and the contribution of these technology usage lags to international differences in living standards and post-war growth rates.

The East Asian Tigers all coincided with a catch-up in the range of technologies used with respect to industrialized countries. These development miracles all involved a substantial reduction of their technology adoption lags relative to (other) OECD countries

15 to 30 years is a common technology usage lag even within the United States for the 10-90 technology lag. The 10-90 lag is how long it takes between when 10% of industry is using a technology, and 90% of an industry is using that technology.

Entrepreneurship, Business Incubation, Business Models & Strategy Blog

There is a plenty of research carried out about how important early adoption of technology is. I’ve recently skimmed a couple of researches on this topic. In my opinion there are two authors that made a better job than others. Their names are Diego Comin and Bart Hobijn.

They performed a cross-country analysis called Cross-country Historical Adoption of Technology (CHAT). This research dataset covers the diffusion of 104 technologies in 161 countries during the last 200 years. The data is available for download.

I just want to share with you the results of their report which could help better understand what’s happening in today’s world of innovations and entrepreneurship and what expect from future.

Finding # 1. “On average, countries adopted a new technology 45 years after its invention.”

Finding # 2. “Variation in adoption rates is larger than you might expect and accounts for 25% of differences…

View original post 95 more words

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Economics, public policy, monetary policy, financial regulation, with a New Zealand perspective

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Restraining Government in America and Around the World

Recent Comments