Crony capitalism flashback – who voted against the TARP in 2008?

20 Jun 2014 Leave a comment

in financial economics, global financial crisis (GFC), great recession, macroeconomics, rentseeking Tags: crony capitalism, TARP

The US House of Representatives initially voted down the TARP in a grand coalition of right-wing republicans and left-wing democrats, voting 205–228. The right-wing republicans opposed the bailout because capitalism is a profit AND loss system. Democrats voted 140–95 in favour of the Bill while Republicans voted 133–65 against it.

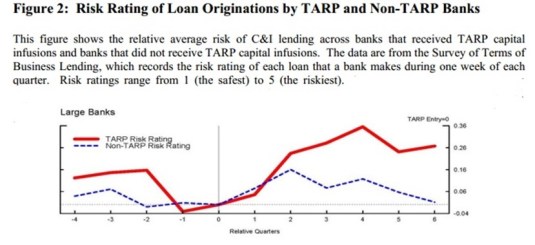

The chart above shows that the degree of risk in commercial loans made by TARP recipients appears to have increased. This is no surprise. In the 1960s, Sam Peltzman published a paper in in the 1960s showing that when deposit insurance was introduced in the USA in the 1930s, the banks halve their capital ratios. They did not need to have as much capital as before to back their lending. The chart below shows that the TARP really didn’t do much for economic policy uncertainty.

In an open letter sent to Congress, over 100 university economists described three fatal pitfalls in the TARP:

1) Its fairness. The plan is a subsidy to investors at taxpayers’ expense. Investors who took risks to earn profits must also bear the losses. The government can ensure a well-functioning financial industry without bailing out particular investors and institutions whose choices proved unwise.

2) Its ambiguity. Neither the mission of the new agency nor its oversight is clear. If taxpayers are to buy illiquid and opaque assets from troubled sellers, the terms, timing and methods of such purchases must be crystal clear ahead of time and carefully monitored afterwards.

3) Its long-term effects. If the plan is enacted, its effects will be with us for a generation. For all their recent troubles, America’s dynamic and innovative private capital markets have brought the nation unparalleled prosperity. Fundamentally weakening those markets in order to calm short-run disruptions is will short-sighted.

A recent IMF study of 42 systemic banking crises showed that in 32 cases, there was government financial intervention.

Of these 32 cases where the government recapitalised the banking system, only seven included a programme of purchase of bad assets/loans (like the one proposed by the US Treasury). These countries were Mexico, Japan, Bolivia, Czech Republic, Jamaica, Malaysia, and Paraguay.

The Government purchase of bad assets was the exception rather than the rule in banking crises and rightly so. The TARP mostly benefited bank shareholders. A case of privatising the gains and socialising the losses from banking was passed on the votes of Congressional Democrats.

To avert a financial panic, central banks should lend early and freely to solvent banks against good collateral but at penal rates

19 Jun 2014 Leave a comment

in financial economics, global financial crisis (GFC), great recession, macroeconomics, monetary economics, Thomas M. Humphrey Tags: lender of last resort, Thomas Humphrey, Walter Bagehot

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose. The amount of bad business in commercial countries is an infinitesimally small fraction of the whole business…

The great majority, the majority to be protected, are the ‘sound’ people, the people who have good security to offer. If it is known that the Bank of England is freely advancing on what in ordinary times is reckoned a good security—on what is then commonly pledged and easily convertible—the alarm of the solvent merchants and bankers will be stayed. But if securities, really good and usually convertible, are refused by the Bank, the alarm will not abate, the other loans made will fail in obtaining their end, and the panic will become worse and worse.

Walter Bagehot Lombard Street: A Description of the Money Market (1873).

The classical theory of the lender of last resort stressed

(1) protecting the aggregate money stock, not individual institutions,

(2) letting insolvent institutions fail,

(3) accommodating sound but temporarily illiquid institutions only,

(4) charging penalty rates,

(5) requiring good collateral, and

(6) preannouncing these conditions in advance of crises so as to remove uncertainty.

Did anyone follow these rules in the global financial crisis? The Fed violated the classical model in at least seven ways:

- Emphasis on Credit (Loans) as Opposed to Money

- Taking Junk Collateral

- Charging Subsidy Rates

- Rescuing Insolvent Firms Too Big and Interconnected to Fail

- Extension of Loan Repayment Deadlines

- No Pre-announced Commitment

- No Clear Exit Strategy

…{the Fed’s} policies are hardly benign, and that extension of central bank assistance to insolvent too-big-to-fail firms at below-market rates on junk-bond collateral may, besides the uncertainty, inefficiency, and moral hazard it generates, bring losses to the Fed and the taxpayer, all without compensating benefits. Worse still, it is a probable prelude to a severe inflation and to future crises dwarfing the current one.

2014 Homer Jones Memorial Lecture – Robert E. Lucas Jr.

18 Jun 2014 Leave a comment

The first part of his lecture discusses how the Fed can influence inflation and financial stability.

Central banks can control inflation. Can central banks maintain economic stability’s financial stability? This is still an open question as to whether central banks can do that. The quantity theory of money makes certain sharp predictions about monetary neutrality which are well borne out by the cross country evidence.

In the second part of this lecture, Lucas discusses how central banks around the world have used inflation targeting to keep inflation under control.

What is the Fed to do with the stable relationship between money and prices? Inflation targeting is superior to a fixed growth monetary supply growth rule. This always pushes policy in the direction of the inflation rate you want. Central banks around the world have succeeded in keeping inflation low by explicitly or implicitly targeting the inflation rate.

In the last part of his lecture, Lucas discusses financial crises. he agrees with Gary Gordon’s analysis that 2008 financial crisis was a run on Repo. A run on liquid assets accepted as money because they can be so quickly changed into money. The effective money supply shrank drastically when there was a run on these liquid assets.

Lucas favoured the Diamond and Dybvig of bank runs as panics. The logic of that model applies to the Repo markets now was well as to the banking system. How to extend Glass–Steagall Act type regulation of bank portfolios to the Repo market is a question for future research.

Inflation targeting is working well but the lender of last resort function is yet to be fully understood.

Note: The Diamond-Dybvig view is that bank runs are inherent to the liquidity transformation carried out by banks. A bank transforms illiquid assets into liquid liabilities, subject to withdrawal.

Because of this maturity mismatch, if depositors suspect that others will run on the bank, it is optimal for each depositor to run to the bank to withdraw his or her deposit before the assets are exhausted. The bank run is not driven by some decline in the fundamentals of the bank. Depositors are spooked for some reason, panic, and attempt to withdraw their funds before others get in first. In this case, the provision of deposit insurance and lender of last resort facilities reassures depositors and stems the bank run

In the Kareken and Wallace model of bank runs, deposit insurance is problematic because of the incentives it gives to deposit taking institutions that are insured to take much greater risks. When there is deposit insurance, depositors don’t care about the greater risk in the portfolios of their banks. The greater risk taking leads to higher returns at no extra cost because if these risky investments do fail, the deposit insurance covers their losses

It is therefore necessary to regulate the portfolio of insured banks to ensure that they do not do this. That is the great dilemma for banking regulation because quasi-banks and other liquidity transformation intermediaries such as a Repo market spring up just outside the regulatory net.

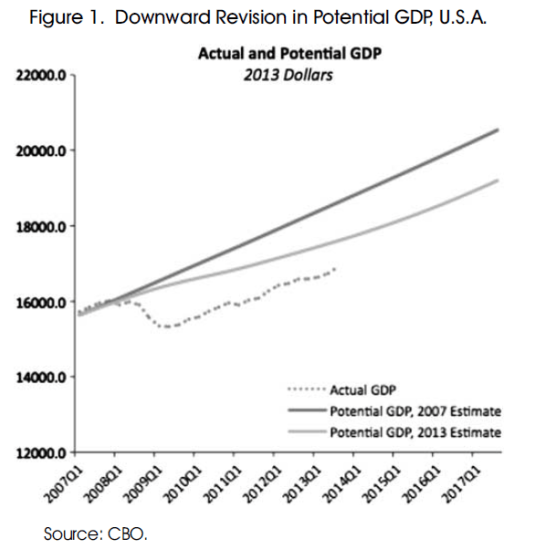

The U.S. Economic Growth Gap Revisited

18 Jun 2014 Leave a comment

in economic growth, great recession, macroeconomics Tags: The Great Recession

Robert Lucas has asked:

Is it possible that by imitating European policies on labor markets, welfare, and taxes that the U.S. has chosen a new, lower GDP trend?

If so, it may be that the weak recovery we have had so far is all the recovery we will get.

The U.S. and Euro-zone non-recoveries

15 Jun 2014 Leave a comment

in Euro crisis, great recession, macroeconomics Tags: great recession, the great deviation

Employment losses after financial crises

11 Jun 2014 Leave a comment

in Euro crisis, global financial crisis (GFC), great recession, macroeconomics Tags: financial crise will s, The shape of recovery

The Obama recovery

08 Jun 2014 1 Comment

in great recession, macroeconomics Tags: recoveries from recessions, The Great Recession

The deviation from trend is widening.

HT: John Lott

Edward C Prescott – Restoring U.S. Prosperity – Brazil, 10 May 2014

27 May 2014 Leave a comment

in Edward Prescott, great recession, macroeconomics Tags: Edward Prescott, great recession

A Great Recession or a permanent move to a lower U.S. growth path?

16 May 2014 Leave a comment

in economic growth, great recession Tags: Obamanomics, trend growth rate of the USA

Philadelphia Fed President Charles Plosser made this nice graph on official views of potential GDP and trends in actual GDP.

The path to higher U.S. prosperity

12 May 2014 Leave a comment

in applied welfare economics, economic growth, Edward Prescott, great recession, labour economics, macroeconomics Tags: capital taxation, Edward Prescott, retirement savings, tax reform

Suppose the USA:

- Had mandatory savings for retirement

- Eliminated capital income taxes

- Broadened tax base and lowered the marginal tax rate

- Phased in reforms so all birth-year cohorts are made better off

- Left welfare programs and local public good shares the same

- Savings not part of taxable income, saving withdrawals part of taxable income – with these changes U.S. income tax would be a consumption tax

US Detrended GDP per Capita

Source: Edward Prescott and Ellen McGrattan 2013.

A Great Recession or dropping to a lower long-term growth path

03 May 2014 Leave a comment

in great recession, macroeconomics Tags: Edward Prescott, great recession, Robert Lucas

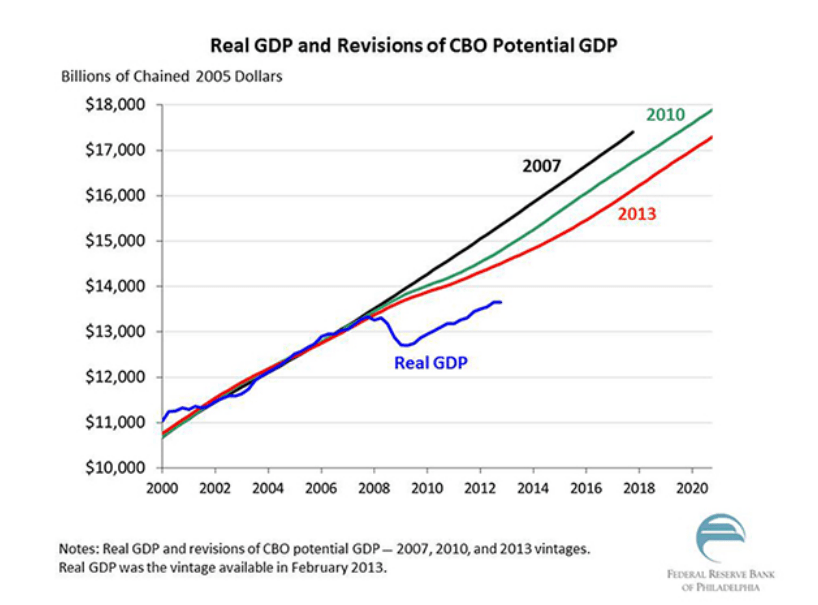

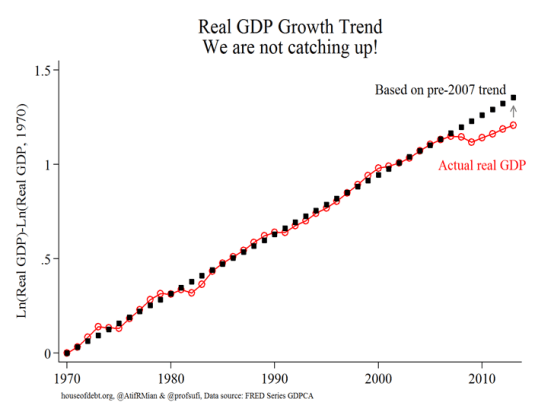

Ed Prescott and Robert Lucas are several of many who use variations of the chart below to show that the USA has moved to a lower long-term growth path.

Source: House of Debt

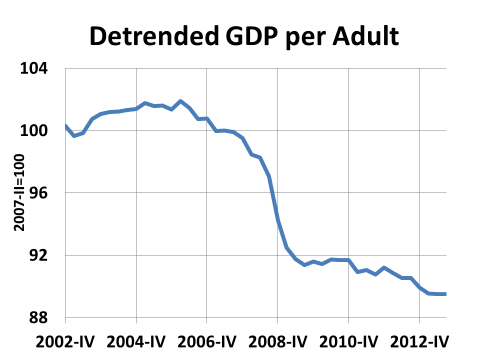

The chart below for output per working age American (ages 15 to 64) is just as depressing.

Source: Edward Prescott

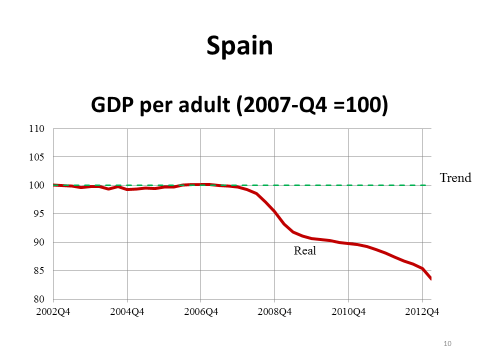

At least Spain with its 25% unemployment rate is doing a little worse.

Source: Edward Prescott

Recent Comments