Anyone who had a good idea about what the the New Zealand dollar should be would be trading on their own account. These super-rich would not be wasting their time giving advice to others. Their time would be too handsomely rewarded for such meagre returns as pontificating to others as to what they should do with their portfolios.

https://twitter.com/JimRose69872629/status/626597273007296514

One of my delights as a bureaucrat was at a meeting between the Reserve Bank of New Zealand and the International Monetary Fund some 15 years or so ago

The Fund asked whether Bank whether it thought the exchange rate was too high, and what their exchange-rate modelling say about this?

- The reply of the Deputy Governor of the Reserve Bank of New Zealand was we don’t have exchange rate model because we don’t think there are any good. Gone are those days.

- The International Monetary Fund team was quite flabbergasted by this response.

At one stage the Fund team tried to draw me into the conversation about the level of New Zealand dollar because I was there representing the New Zealand Treasury. I was only attended as an observer, so naturally my response to their questions was to waffle incoherently. I could have been blunter and simply said the Reserve Bank of New Zealand spoke for New Zealand in this matter, but that would have been impolite.

I’ve been continuing to reflect on Graeme Wheeler’s repeated observation that New Zealand’s exchange rate “needs” to come down. I’m still not entirely sure what he means. The exchange rate is an asset price and presumably should reflect all expected future relevant information, not just spot information about current dairy prices. And the market has no particular reason to focus on stabilising the net international investment position at around current levels. Indeed, although it is a convenient reference point, neither does the Reserve Bank.

“Need” or not, I’d have thought it was likely that the exchange rate would fall further.

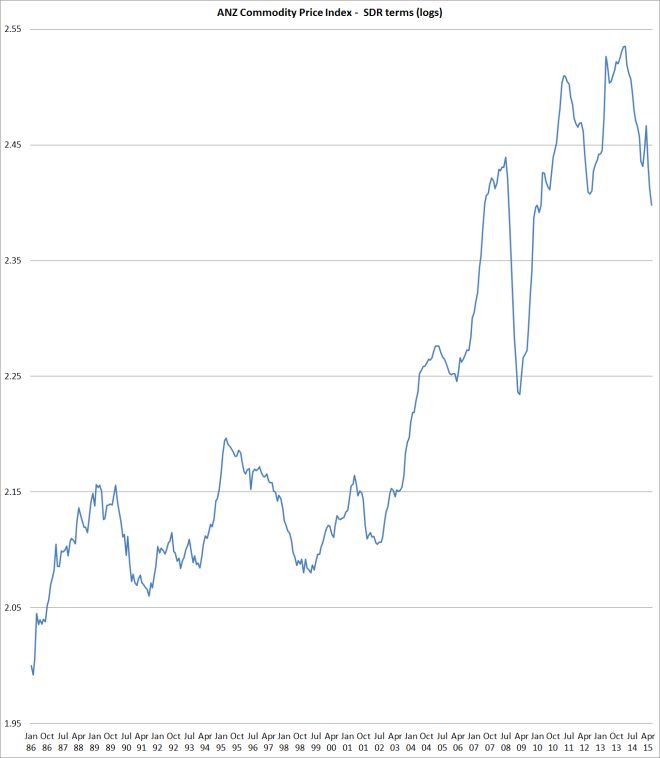

The ANZ Commodity Price Index, which lags behind (for example) falling GDT and futures dairy prices, has already had one of the larger falls in the history of the series.

Meanwhile, the fall in the exchange rate, while material, remains pretty small by the standards of past New Zealand adjustments…

View original post 165 more words

Recent Comments