Our monthly update on the question: should I stay in school? blogs.wsj.com/economics/2015… http://t.co/IaVxoAJmqe—

Josh Zumbrun (@JoshZumbrun) April 03, 2015

College graduates don’t really notice recessions

02 May 2015 Leave a comment

in business cycles, economics of education, great recession, human capital, labour economics, macroeconomics, occupational choice, politics - USA, unemployment Tags: College premium, education premium, labour demographics

On the New Deal and the rule of law

01 May 2015 Leave a comment

in economic history, macroeconomics, monetary economics, politics - USA Tags: gold standard, New Deal, regime uncertainty, rule of law

Recoveries from recessions across the G-7

28 Apr 2015 Leave a comment

in business cycles, economic growth, Euro crisis, global financial crisis (GFC), great recession, macroeconomics, politics - USA Tags: British economy, Canada, Eurosclerosis, France, Germany, Italy, Japan, recoveries from recessions

UK recovery: stronger than Italy, weaker than US & Canada. http://t.co/C0TEsbzMm3—

Jonathan Portes (@jdportes) April 28, 2015

The impact of the top tax rate in the depth and severity of the great depression

24 Apr 2015 Leave a comment

in business cycles, fiscal policy, great depression, macroeconomics, politics - New Zealand, politics - USA, public economics Tags: capital taxation, New Zealand, taxation and the labour supply, top tax rate

Source: Ellen McGrattan.

There were large differences in increases in the 1930s in the top marginal income tax rate between Sweden, the UK, France with Australia and New Zealand and between the USA and Canada and the rest as McGrattan explains:

These data show that there is a strong negative correlation, roughly −94%, between the change in the top income tax rates and the deviation in per capita real GDP relative to trend in 1933.

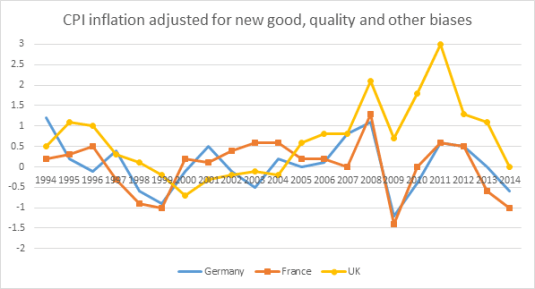

British, German and French inflation rates adjusted for 1.5% new goods and quality bias, 1994-2014

24 Apr 2015 Leave a comment

in economic history, inflation targeting, macroeconomics, monetary economics

There has been close to zero inflation in France and Germany for almost 20 years now. The UK had mild deflation between 1998 and 2005, followed by a spike in inflation.

Source: OECD StatExtract.

Note that the 1.5% bias adjustment includes other known biases in the CPI in addition to new goods and quality variation.

The role of new taxes in the Great Recession

24 Apr 2015 Leave a comment

in economic growth, fiscal policy, great recession, labour economics, labour supply, macroeconomics, politics - USA Tags: great recession, obama, Obamacare, taxation and entrepreneurship, taxation and investment, taxation and labour supply

.

Australian and New Zealand inflation rates adjusted for new goods and quality bias of 1.5%

23 Apr 2015 Leave a comment

in inflation targeting, macroeconomics, politics - Australia, politics - New Zealand Tags: Australia, CPI bias, inflation, New Zealand

In praise of measurement error: good thing no one noticed the severe deflation in Australia and in New Zealand in the late 1990s for otherwise the do-gooders might have felt the need to do something about it. Good thing no one is panicking over the recent mild deflation in New Zealand as well.

Source: OECD StatExtract

The looming fiscal crisis in the USA

22 Apr 2015 Leave a comment

in fiscal policy, global financial crisis (GFC), great recession, macroeconomics, politics - USA Tags: ageing society

US, UK and Japanese inflation adjusted for new good and quality bias, 1994-2014

22 Apr 2015 Leave a comment

in econometerics, inflation targeting, macroeconomics, politics - USA Tags: CPI bias

All agree that the consumer price index (CPI) is biased and overstates inflation. In 1996, economists hired by the Senate Finance Committee estimated that the U.S. CPI overstates annual inflation by 1.1% (Boskin et al. 1996). That estimated CPI bias has not gotten smaller with time. It is now up to 1.5%, even 2%.

The main biases in the consumer price index everywhere come from how to handle changes in the quality of goods and services and how to deal with completely new goods and services.

I thought I might see what happened if I took account of this one and a half percentage point annual bias because of new goods, quality variation and other known biases in the CPI estimates for the USA, UK and Japan in the relevant OECD StatExtract database for annual CPI inflation.

Source: OECD StatExtract.

Taking into account new good and quality bias, Japan is been in serious deflation for quite some time now – at least 20 years. Japanese inflation went positive in the last year or two because I believe they increased their consumption tax.

The USA has a low inflation for about 20 years. The UK had no inflation for about seven years from 1997 then it started to rise again until 2012.

People get hot and bothered with deflation. Breathless journalism aside, fears of inflation are just a legacy of the great depression in the 1930s.

The only depression where deflation was accompanied by mass unemployment was the Great Depression. Mild deflation with good growth is a common phenomenon as Atkinson and Kehoe found:

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates. Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

The social cost of high company tax rates is just too high

22 Apr 2015 Leave a comment

in economic growth, fiscal policy, human capital, income redistribution, labour economics, macroeconomics, Public Choice Tags: company tax rate, entrepreneurial alertness, tax reform

The rest of Europe can’t expect Germany to keep bailing them out

22 Apr 2015 Leave a comment

in Euro crisis, macroeconomics, population economics Tags: ageing society, European Union, Eurosclerosis, France, Germany, labour demographics

BofA-ML: Working age population projections, a serious problem for Germany http://t.co/eStgQePoVP—

Fabrizio Goria (@FGoria) March 30, 2015

Has New Zealand been in deflation since 2012?

21 Apr 2015 Leave a comment

in global financial crisis (GFC), great depression, inflation targeting, macroeconomics, monetary economics Tags: CPI bias, deflation, inflation, monetary policy

All agree that the consumer price index (CPI) is biased and overstates inflation. In 1996, economists hired by the Senate Finance Committee estimated that the U.S. CPI overstates annual inflation by 1.1% (Boskin et al. 1996). That estimated CPI bias has not gotten smaller with time. It is now up to 1.5%, even 2%.

One of the rationales for the inflation target of the Reserve Bank of New Zealand of 0-2% was the 2% was to account for the consumer price index was biased upwards. Targeting 0% would lead to mild deflation when inflation was properly measured.

The main biases in the consumer price index everywhere come from how to handle changes in the quality of goods and services and how to deal with completely new goods and services.

I thought I might see what happened if I took this one and a half percentage point annual bias in the CPI estimated for the USA and adjusted the New Zealand CPI inflation rates available at the Reserve Bank of New Zealand’s website over the last 20 years or so with this number.

If these consumer price index bias adjustments are correct, and they are roughly correct, inflation came to a dead stop in New Zealand after the global financial crisis in 2008, spiked again, and then moved into deflation in 2012. If anything, there’s been a mixture of price stability and the deflation since 2012.

People get quite hot and bothered with deflation. The New Zealand economy has been in a deflationary phase since the beginning of 2012 but it is recently grown so quickly that it is referred to in the media as the rock-star economy.

Breathless journalism aside , fears of inflation are just a legacy of the great depression in the 1930s. The only depression where deflation was accompanied by mass unemployment was the Great Depression. Mild deflation with good growth is a common phenomena as Atkinson and Kehoe found:

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates.

Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

Levels of output are nowhere near returning to pre-crisis trends

21 Apr 2015 Leave a comment

in business cycles, economic growth, Euro crisis, global financial crisis (GFC), great recession, macroeconomics Tags: Eurosclerosis

The role of unions in prolonging the Great Depression

20 Apr 2015 1 Comment

in business cycles, fiscal policy, great depression, labour economics, labour supply, macroeconomics, politics - USA, unemployment, unions Tags: capital taxation, FDR, Herbert Hoover, Leftover Left, Leo Ohanian, New Deal, union power, union wage premium, unionisation

Our friends on the left at the Economic Policy Institute were good enough to remind us of the link between rapid unionisation of the US labour market in the early and mid-1930s and the petering out of the recovery from the great depression. That recession within a depression is the Roosevelt recession.

New blog on Mind The Gap: on labour #unions and income #inequality

oxfamblogs.org/mindthegap/201… http://t.co/FyrOboCaRk—

Ricardo FuentesNieva (@rivefuentes) April 17, 2015

Harold Cole and Lee Ohanian analysed in depth this double-dip depression in the USA in a paper in the Journal of Political Economy titled “New Deal Policies and the Persistence of the Great Depression: A General Equilibrium Analysis” about 10 years ago:

The recovery from the Great Depression was weak… Real gross domestic product per adult, which was 39 percent below trend at the trough of the Depression in 1933, remained 27 percent below trend in 1939. Similarly, private hours worked were 27 percent below trend in 1933 and remained 21 percent below trend in 1939.

The weak recovery is puzzling because the large negative shocks that some economists believe caused the 1929–33 downturn—including monetary shocks, productivity shocks, and banking shocks—become positive after 1933. These positive shocks should have fostered a rapid recovery, with output and employment returning to trend by the late 1930s.

The focus of the paper by Cole and Ohanian in explaining the weak recovery – the double-dip depression in the 1930s – are the New Deal cartelisation policies designed to limit competition and increase labour bargaining power through extensive unionisation of workforce.

The recovery from the depths of the Great Depression was weak but real wages in several sectors rose significantly above trend despite mass unemployment.

The view that limiting competition in product markets and the labour market was essential for economic prosperity was influential in the 1920s and 1930s. Both FDR and Hoover believed high wages were the key to prosperity.

FDR’s recipe for economic recovery from the great depression when he came to office in 1933 was raising prices and wages and the promotion of unions:

Union membership rose from about 13 percent of employment in 1935 to about 29 percent of employment in 1939, and strike activity doubled from 14 million strike days in 1936 to about 28 million in 1937.

The result of this suppression of market competition and the encouragement of unions was real wages increase despite the weak recovery:

The coincidence of high wages, low consumption, and low hours worked indicates that some factor prevented labour market clearing during the New Deal.

The combination of government interference with competition and strong unions stifled the recovery from the great depression rather than speed it up as was the plan of FDR:

New Deal labour and industrial policies did not lift the economy out of the Depression as President Roosevelt had hoped.

Instead, the joint policies of increasing labour’s bargaining power and linking collusion with paying high wages prevented a normal recovery by creating rents and an inefficient insider-outsider friction that raised wages significantly and restricted employment.

Not only did the adoption of these industrial and trade policies coincide with the persistence of depression through the late 1930s, but the subsequent abandonment of these policies coincided with the strong economic recovery of the 1940s.

U.S. unemployment fell from 22.9% in 1932 to 9.1% in 1937, a reduction of 13.8%, but was back up to 13% by 1938. The Social Security payroll tax debuted in 1937 on top of tax increases in the Revenue Act of 1935. In 1937, the economy fell into recession again. Cooley and Ohanian argue that:

The economy did not tank in 1937 because government spending declined. Increases in tax rates, particularly capital income tax rates, and the expansion of unions, were most likely responsible.

The Great Depression in the USA was unique in the fact that it was so long and the recovery, so weak:

Total hours worked per adult in 1939 remained about 21% below their 1929 level, compared to a decline of 27% in 1933… Per capita consumption did not recover at all, remaining 25% below its trend level throughout the New Deal, and per-capita non-residential investment averaged about 60% below trend.

After 1933, productivity growth was rapid, the banking system was stabilized, deflation was eliminated and there was plenty of demand stimulus as the Fed more than doubled the monetary base between 1933 and 1939. As Lee Ohanian noted:

Depressions are periods of low employment and low living standards. The normal forces of supply and demand should have reduced wages, which would have lowered business costs and increased employment and output. What prevented the normal forces of supply and demand from working?

Central to the faltering of this recovery by 1937 was the regime change when the Supreme Court finally upheld revised laws promoting unionisation:

The downturn of 1937-38 was preceded by large wage hikes that pushed wages well above their NIRA levels, following the Supreme Court’s 1937 decision that upheld the constitutionality of the National Labor Relations Act. These wage hikes led to further job loss, particularly in manufacturing.

The "recession in a depression" thus was not the result of a reversal of New Deal policies, as argued by some, but rather a deepening of New Deal polices that raised wages even further above their competitive levels, and which further prevented the normal forces of supply and demand from restoring full employment.

Lee Ohanian argues that the defining characteristic of the Great Depression was this failure of real wages to fall in the face of mass unemployment:

The defining characteristic of the Great Depression is a substantial and chronic excess supply of labour, with employment well below normal, and real wages in key industrial sectors well above normal.

Policies of Hoover and of FDR of propping up wages and encouraging unions and work sharing were the most important factors in precipitating and prolonging the Great Depression. The Great Depression was the first time U.S. wages did not fall in that you were administered a period of significant deflation.

The manufacturing sector, where unions and the threat of unionisation was much stronger which was much harder hit initially than the agricultural sector both in terms of loss of jobs and wages not falling. The Great Depression did not start as an ordinary garden variety recession, as argued by Milton Friedman. It was immediately severe and sector specific with industrial production declining by about 35% between late 1929 and the end of 1930.

This decline in industrial production occurs before any banking crises. Despite this sector specific nature of the onset that Great Depression, monetary policy might have some role in explaining the start of the Great Depression but not in its prolongation:

any monetary explanation of the Depression requires a theory of very large and very protracted monetary non-neutrality. Such a theory has been elusive because the Depression is so much larger than any other downturn, and because explaining the persistence of such a large non-neutrality requires in turn a theory for why the normal economic forces that ultimately undo monetary non-neutrality were grossly absent in this episode.

Source: A different view of the Great Depression’s cause | VOX, CEPR’s Policy Portal.

50% more R&D since the 60s, but still no growth dividend?

18 Apr 2015 1 Comment

in applied price theory, economic growth, economics of education, entrepreneurship, history of economic thought, human capital, industrial organisation, macroeconomics, occupational choice, survivor principle Tags: Ben Jones, Chad Jones, creative destruction, endogenous growth theory, innovation, R&D

Spending on intellectual property products has risen in the USA from 1% in 1950 to 5% now. Public R&D spending in the USA has been pretty static for 60 years. Intellectual property products in the chart below includes traditional research and development, spending on computer software, and spending on entertainment such as movies, TV shows, books, and music. Spending on software and entertainment was only recently measured in the US national accounts. This inclusion of intangible capital investments will radically change the story of economic growth and the business cycle in the 20th century.

Source: Chad Jones (2015).

The growth rate in the USA hasn’t changed much despite this massive increase in intellectual property property product production. Is innovation getting harder? R&D is supposed to boost the growth rate, if you are to believe politicians bearing subsidies for it wherever they find it.

Source: Chad Jones (2015).

Ben Jones in The Burden of Knowledge and the Death of the Renaissance Man: Is Innovation Getting Harder? found that as knowledge accumulates as technology advances, successive generations of innovators may face an increasing educational burden. Innovators can compensate through lengthening their time in education and narrowing expertise, but these responses come at the cost of reducing individual innovative capacities. This has implications for the organization of innovative activity – a greater reliance on teamwork – and has negative implications for economic growth.

This longer period of education and initial study is not compensated by inventors innovating for longer spans of their lifestyle. This rising burden of knowledge is cutting into their best years of their lives. Jones found a broad and dramatic declines in early life-cycle productivity among great minds and ordinary inventors, and a close relationship of these trends with increased training duration.

Jones found that the age at first invention, specialisation, and teamwork increased over time in a large micro-data set of inventors. Upward trends in academic collaboration and lengthening doctorates can also be explained in his framework of innovation getting harder because of a rising burden of knowledge. Co-authorship in academic literature has increased, including physics, biology, chemistry, mathematics, psychology, and economics. This measure of teamwork has increased 17% per decade.

Using data on Nobel Prize winners, Jones found that the mean age at which the innovations are produced to win the Prize has increased by 6 years over the 20th Century.

- Before 1901, two-thirds of the Nobel laureates did their prize-winning work before the age of 40 and 20 per cent did it before age of 30.

- By 2000, however, great achievements seldom occurred before the age of 40.

It’s now taking longer for scientists to get their basic training and start their careers. There is simply more to learn because knowledge in all fields has grown by quantum leaps in the past century. Nobels are being handed out for different types of work than a century ago.

- There has been a trend away from awarding prizes for abstract, theoretical ideas.

- Now more honours are being bestowed on people who have made discoveries through painstaking lab work and experimentation – which takes a lot of time to do.

Jones’ theory provides an explanation for why productivity growth rates did not accelerate through the 20th century despite an enormous expansion in collective research effort and levels of education and many more graduates. Innovation is getting harder?

{kind=link}

Recent Comments