I learnt at the Australian Productivity Commission that the first law of public policy development is plagiarise, plagiarise, plagiarise. Why be original? Copy the successes of others, improve upon them, but do not repeat their failures, just learn from them.

I developed this policy insight from my experience at the Productivity Commission with a smart-arse Commissioner – that was the chairman’s private description of him in a conversation with me, not mine.

This Commissioner with whom I had countless arguments would respond to the many US studies I had marshalled by always asking for Australian evidence – what is the Australian evidence?

He knew that there was no Australian data or studies so he could slow the whole policy process down through this appeal to data chauvinism. The Americans are swimming in data and that is before you get to their cross-sectional data with 50 states.

Ever since then, I regarded data chauvinism – the request for Australian evidence and studies or New Zealand evidence and studies – as a stalling tactic designed either to defend the status quo.

By and large, all the local evidence shows when it augments the US studies is how a local regulation or tax screws things up further. Local evidence rarely served the interests of my opponents who were fighting against deregulation or privatisation.

It is a good public policy – you are much more likely to implement a proposal or act on a particular empirical study – if there are half a dozen to a dozen overseas studies preferably in several different countries showing much the same thing. Beware the man of one study. Milton Friedman (1957) rightly preferred to emphasize the congruence of evidence from a number of different sources and with due attention to the quality of the data:

I have preferred to place major emphasis on the consistency of results from different studies and to cover lightly a wide range of evidence rather than to examine intensively a few limited studies.

The role of empirical evidence is to resolve disagreements – to bring people closer together. One study in one country rarely does that. Many studies in many countries about the same topic of controversy is far more persuasive.

Green MP Gareth Hughes today nailed the case as to why governments should never run businesses. Too many MPs simply do not understand what dividends represent and what the profits from asset sales represent.

Data out today shows the asset sales so far have cost $1 billion. https://t.co/HeDndEjINg – double blow for Kiwis facing rising power bills

Hughes was reported today saying that taxpayers lost nearly $1 billion in dividends since the recent privatisations of power companies. He is the Green party spokesman on state owned enterprises.

Does the Green Party understand that an asset sells for a price equal to its risk-adjusted discounted net present value of the stream of dividends. When you sell a financial asset, you cash out the net present value of the stream of dividends that might have come from those assets.

The Greens, who are prissy about government transparency and dishonesty of their opponents, did not mention the $4.7 billion in revenue from the asset sale. Taxpayers now receiving more in dividends as a part owner of the privatised power companies than they did as a full owner.

Hughes had the cheek to complain about the politicisation of those privatisations such as favourable terms for small share buyers. That inability of governments to even sell an asset competently is a strong reason why governments should never run businesses in the first place.

If an asset cannot be sold in the full light of day – a major issue in an election campaign and a referendum – without the sale price that is politicised, what is the chance of good management of any state-owned enterprise when it is not the central focus of opposition scrutiny?

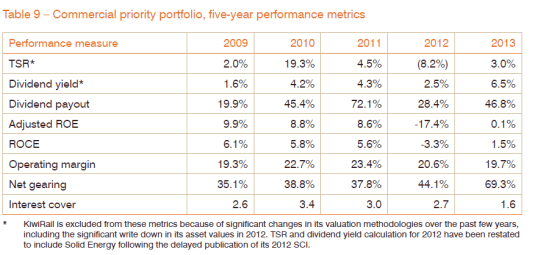

It is been many years since dividends from the state-owned enterprise portfolio has been a net positive cash flow for the taxpayer, as the chart below shows.

Source: New Zealand Treasury – data released under the Official Information Act.

KiwiRail and Solid Energy gobbled up whatever dividends came out of the power companies. Aside from power companies, state-owned enterprises not really offer much in the way of dividends to the taxpayer as the chart again shows.

In common with New Zealand, Maine found that a number could not complete work requirements because they could not get time off work from their off the books job.

Lindsay Mitchell found through Official Information Act requests that one in 10 beneficiaries are working full-time and one in 5 have no intention of looking for a job in the next year despite a requirement to actively look for work as a condition of receipt of their benefit.

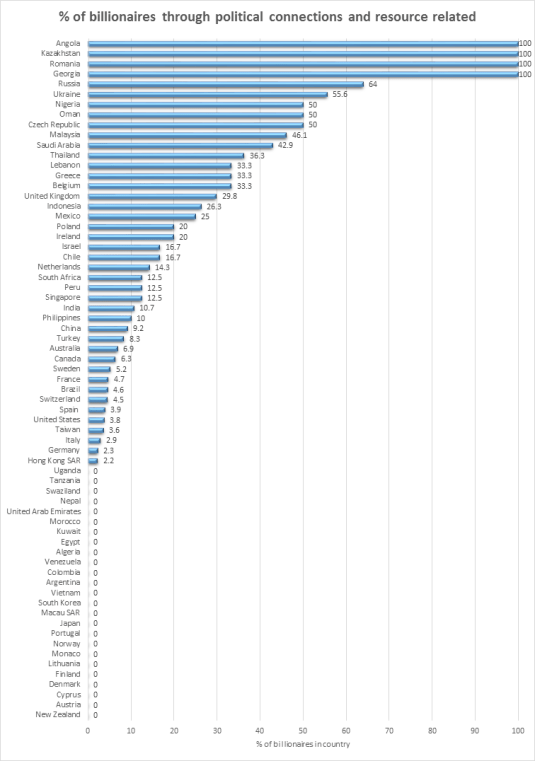

The 1826 Billionaires in the Forbes 2015 list are classified as rich through political connections if they made their money through past political positions, close relatives or friends in government, or questionable licenses, privatisations or resource extraction industries.

All privatizations were included in the politically-connected/resource-related category despite my data source acknowledging the possibility that the new owners may have transformed the company. Resource billionaires were all deemed to be lucky or cronies by my data source rather than diligent as some most certainly were. This is something of a slur by my data source given the industriousness of some resource billionaires some of whom were even geologists.

Political cronyism is a path to billionaire wealth mainly in the developing countries. Less than 10% of Chinese billionaires made their money through political connections, which is surprising.

The most mystifying bureaucratic rule I have come across is in Western Europe. A number of these countries require entrepreneurs deposit a minimum sum of money in a bank or before a notary up to a month before registration and 3 months after incorporation. If they cannot do this, they cannot start their business lawfully.

I am mystified as to what this regulation is designed to do other than make it difficult to start a new business. It is a private commercial matter as to whether trade credit is extended to new businesses. That indeed is one of the challenges facing every entrepreneur: discovering who are reliable business partners or not.

One of the functions of banks is to issue letters of credit. These vouch for the financial strength of a customer when seeking new business or export markets.

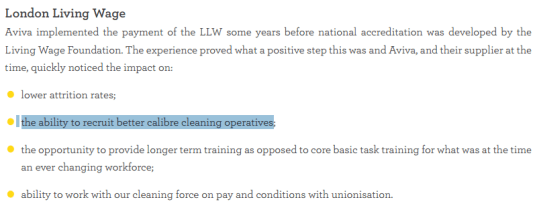

Research publicised by a Living Wage UK highlighted the Achilles heel of any living wage proposal. This Achilles heel applies to the voluntary adoption of the living wage and a living wage mandated through minimum wage laws.

The critique to follow accepts pretty much everything claimed by the living wage movement about the benefits of the living wage but simply traces out the consequence of this one promised benefit.

The living wage is substantially above the minimum wage. Offering the living wage will change the composition of the recruitment pool of low-wage employers. This is the Achilles heel of the living wage which Living Wage UK documents in its study it tweeted about and from which I have taken the above snapshot.

Jobseekers would not have considered vacancies by these employers will now apply because of the living wage increase. These better calibre applicants will win those jobs ahead of the jobseekers whose current productivity levels are less than that to justify the cost of the living wage.

Central to the living wage rhetoric is that somehow employees will be more productive because of the adoption of the living wage.

The simplest way of doing that for an employer is to hire more qualified, more productive employers are no longer a hire the type of people you currently hire. They will be unemployed or pushed into the non-living wage sector of the low-wage market.

A living wage is an exclusionary policy where ordinary workers, often with families who are not productive enough to produce $19.25 per hour living wage plus overheads will never be interviewed.

The workers with the type of skills that currently win those jobs covered by a living wage increase will not be shortlisted because the quality of the recruitment pool will increase because of the living wage.

There will be an influx of more skilled workers attracted by the higher wages for living wage jobs. They will go to the head of the queue and displaced workers who currently apply for and win these jobs before the adoption of the living wage.

Any extra labour productivity from paying a living wage increase is in doubt because low skilled service sectors are notorious for their low potential for productivity gains. They are the bread-and-butter ofBaumol’s disease.

The modern theories of the firm focus, in part or in full on reducing opportunistic behaviour, cheating and fraud in employment relationships. The cost of discovering prices and making and enforcing contracts and getting what you pay for are central to Coase’s theory of the firm put forward in 1937.

The profits of entrepreneurs for running a firm is directly linked from their successful policing of the efforts of employees and sub-contractors to ensure the team and each member perform as promised and individual rewards matched individual contributions (Alchian and Demsetz 1972; Barzel 1987). Alchian and Demsetz’s (1972) theory of the firm focused on moral hazard in team production. As they explain:

Two key demands are placed on an economic organization-metering input productivity and metering rewards.

The main rationale in personnel economics from everything ranging from employer funding of retirement pensions to the structure of promotions and executive pay including stock options is around better rewarding self-motivating employees who strive harder and reducing the costs of monitoring employee effort.

At bottom, the efficiency wage hypothesis is entrepreneurs are unaware of the higher quality and greater self-motivation of better paid recruits for vacancies but wise bureaucrats and farsighted politicians notice these gaps in the market. Bureaucrats and politicians notice these gaps in the market before those who gain from superior entrepreneur alertness to hitherto untapped opportunities for profit do so and instead leave that money on the table.

It’s kicking the living wage movement when it is down to mention that low paid workers with families will lose a considerable part of the living wage increase because of reductions in family tax credits and in-kind assistance from the government that are linked to their pay.

Their jobs are put at risk because of a large increase in the cost of employing them to their employers. Their take-home pay after taxes, family tax credits and other government assistance increases by much less. This is a pointless gamble with job security because of the much small increase in the take-home pay of many breadwinners on the living wage.

Back in the day, MFAT got around to reviewing its contributions to various UN organisations. They discovered they were contributing $250,000 to some obscure committee that was part of the UN Food and Agricultural organisation.

When this particular committee heard that their contribution was under review, they immediately dispatched 6 bureaucrats from Rome to Wellington to make their case.

These flying UN diplomats could have been so stupid as to not notice that 6 UN bureaucrats showing up out of nowhere after years of silence as soon as their budget contribution was under review might not improve what little goodwill they had left in the Wellington bureaucracy. No one could remember why we were contributing. Their willingness to spend so freely in airfares certainly did not help.

The same goes for the European Bank for Reconstruction and Development. This bank was formed shortly after the fall of the Berlin Wall. New Zealand joined for reasons now forgotten.

I happen to call upon the Australian Executive Director representing New Zealand at that Bank while passing through London representing the New Zealand Treasury. Naturally, he felt the need to call upon his New Zealand masters in Wellington shortly after. MFAT did not know what to do with them because they could not remember why New Zealand was still a member of that bank.

This London based Australian international diplomat did better than the Australian Executive Director representing New Zealand on the World Bank. He managed to visit all 12 Pacific islands but never visited New Zealand in his entire 4 years of office. This included after the establishment of the New Zealand Agency for International Development.

What more, this Australian Executive Director flew to Canberra for consultations with his Australian authorities just before Christmas every year. He felt rather put upon when his New Zealand deputy insisted that he take personal days while attending his grandson’s christening.

I visited the World Bank once or twice. It was like visiting a brothel. Absolutely everyone propositioned me from money.

The first people I spoke to try to sell New Zealand some oil debts that Mozambique are defaulted on to Angola. The last person I spoke to tried to interest New Zealand and investing in Latin American trade research.

They are all hopeless is give me directions to the Cato Institute. They seemed to know very little about American politics and Washington DC think tanks.

One of my first jobs at the New Zealand Treasury was to form a position on what the OECD Secretariat should do about its seriously underfunded pension plan. It provided for a 50% life pension after 10 years of service.

I suggested what was done with underfunded superannuation funds in Australia, which was to close them to new members.

An OECD official called upon me in Wellington at my desk a few weeks later. I do not think he made a special trip to Wellington just to put me right, but he made sure I was included on his itinerary.

What a splendid opportunity! In an Australian election year, Kevin Rudd will be back in the Australian news, frequently front page.

This re-emergence of Kevin747 will remind Australian voters of how dysfunctional he was and how dysfunctional the last Labour government was.

Most of the reporting of Kevin Rudd in the Australian media be about how that control freak and social cripple will bring his dysfunctionality to United Nations and international relations generally.

Bill Shorten must hate the idea. The last thing he wants as an unpopular opposition leader is for the last Labour Prime Minister, who he stabbed in the back as prime minister first time round, to be back in the news.

Mark Latham uses to say that the only reason Kevin Rudd was popular with the Australian people was that never met him.

Back in the day, I was having a beer in Bob Hawke’s office along with the rest of the economic division staff from his department. We were told to avoid discussing racing as Hawke would never stop talking about it.

Somehow the conversation got on to Malcolm Fraser becoming secretary general of the Commonwealth Secretariat. He had recently lost the race.

Bob Hawke told us a story about a conversation he had with Margaret Thatcher on the candidature of Malcolm Fraser.

Hawke said that Thatcher said do you really want Malcolm Fraser beating down your door every day about apartheid. She had a point.

I took that remark by Hawke to mean that Fraser had independent stature as a former prime minister. He could annoy powerful people because he had nothing to lose and everything to gain.

The Nigerian chief who got the job will be so grateful for the appointment that he would not upset his sponsors. That is why Helen Clark will not become UN Secretary General. She is overqualified.

UN Secretary General is not the best job Clark has ever had. She has independent gravitas and everything to gain and nothing to lose by being an activist secretary general.

All previous Secretary Generals were obscure foreign ministers who will be just so grateful for the big promotion. They did not have independent gravitas.

If you look at positions such as president of the European commission, managing director of the IMF or president of the World Bank and other international appointments, they do not go to statesman.

Today the Treasury advised that it no longer calculates an annual rate of return on the portfolio of state owned enterprises as a whole. It no longer publishes an annual portfolio report (APR).

Source: Treasury response to Official Information Act request by Jim Rose, 14 January 2016.

The Treasury regards the crown portfolio report which contains performance indicators on the state owned enterprises portfolio as a whole as too resource intensive.

The Treasury prefers to be more forward-looking in their reporting on a quarterly basis to the Minister of Finance. Unfortunately, the Treasury refused to my requests for access to this forward-looking reporting to the Minister of Finance on commercial-in-confidence grounds.

The forward-looking approach to state-owned enterprise performance is now only by the Treasury and the Minister of Finance. No one else has access to this financial performance information.

It is no longer possible to say using a figure calculated by the Treasury whether the portfolio of state owned enterprises as a whole are a good return to the taxpayer or not. Individual annual reports of the state owned enterprises can be reviewed but the portfolio wide rate of return is no longer available from the Treasury with the associated credibility of the same.

A common argument against state ownership is that as a whole government ownership is a bad investment. Specifically, the portfolio of state owned enterprises struggle to pay a return in excess of the long-term bond rate.

A common argument for continued state ownership is the loss of the dividends from privatisation. The vulgar argument such as by the New Zealand Labor Party and New Zealand Greens is if a state owned enterprise is privatised either partially or fully, the taxpayers no longer receive dividends. The fact that the sale price reflects the present value of future dividends is simply ignored.

Governments are so bad as business owners and so incapable of running a commercial process free of politics that governments cannot even sell a state-owned enterprise for a good price under the full glare of the media and public.

A reply to the loss of dividends argument is the dividends from the portfolio as a whole do not repay the government debt incurred to fund capital infusions into state-owned enterprises both when initially established and through time. In that case, it is better to leave your money in the bank than in the state of enterprise.

John Quiggin often criticises privatisation on the grounds that state owned enterprises can invest at a cheaper rate because they are financed at the long-term bond rate:

In general, even after allowing for default risk, governments can borrow more cheaply than private firms. This cost saving may or may not outweigh the operational efficiency gains usually associated with private ownership.

It is not possible to scrutinise that argument without an annual rate of return on the portfolio of state owned enterprises as a whole to see if it is true at first pass at least. As the Treasury no longer calculates a rate of return on the portfolio and taxpayers’ equity, that debate comes to something of a crashing halt in New Zealand.

If these state owned enterprises were privately owned and listed on the share market, investors would just look at trends in share prices for daily measure of expected future profitability.

The fiscal case for privatisation must be assessed on a case by case basis. It will always be true for example that if a public enterprise is operating at a loss, and can be sold off for a positive price with no strings attached, the government’s fiscal position will benefit from privatisation.

Various early ventures in public ownership, such as the state butcher shops operated in Queensland in the 1920s (apparently a response to concerns about thumbs on scales) met this criterion, and there doesn’t seem to be much interest in repeating this experiment.

In most sectors of the economy, the higher cost of equity capital is more than offset by the fact that private firms are run more efficiently, and therefore more profitably, than government enterprises.

But enterprises owned by governments are usually capital intensive and often have monopoly power that entails close external regulation, regardless of ownership. In these situations, the scope to increase profitability is limited, and the lower value of the asset to a private owner is reflected in the higher rate of return demanded by equity investors.

Quiggin is wrong about government enterprises have been a lower cost of capital because it contradicts the most fundamental principles of business finance as explained by Sinclair Davidson:

…it is clear that the Grant-Quiggin view violates the Modigliani-Miller theories of corporate finance. The cost of capital is a function of the riskiness of the investment projects and not a function of a firm’s ownership structure.

How the cash flows of a business are divided between owners and creditors does not matter unless that division changes the incentives they have to monitor the performance of the firm and keep it on its toes. Those lower down the pecking order if things go wrong such as owners have much more of an incentive to monitor the success of the business and lift its performance.

Capital structures of firms, the property rights structures of firms, matter precisely because they influence incentives of those with different claims on the cash flows of the firm.

Having to pay debt disciplines managerial slack and ensures that free-cash flows are used to repay debt (or pay dividends) rather than be invested in low quality new ventures. Having to borrow from strangers such as banks ensures regular scrutiny of the soundness and prospects of the company from a fresh set of eyes. Capital structures made up of both debt and equity keeps the firm on its toes.

Unfortunately, in New Zealand it is much more difficult to review the arguments for and against the current size and shape of the state owned enterprise portfolio as for example summarised by John Quiggin:

Technologies and social priorities change over time, with the result that activities suitable for public ownership at one time may be candidates for privatization in another. However, the reverse is equally true. Problems in financial markets or the emergence of new technologies may call for government intervention in activities previously undertaken by private enterprise.

In summary, privatization is valid and important as a policy tool for managing public sector assets effectively, but must be matched by a willingness to undertake new public investment where it is necessary.

As a policy program, the idea of large-scale privatization has had some important successes, but has reached its limits in many cases. Selling income-generating assets is rarely helpful as a way of reducing net debt. The central focus should always be on achieving the right balance between the public and private sectors.

This balancing of public and private ownership is more difficult in New Zealand because portfolio wide rates of return are unavailable unless you calculate them yourself. That must be labour-intensive given the Treasury thought it was too labour-intensive for it to do for itself.

An obvious motive to start a review the extent of state ownership is the portfolio is performing poorly. That warning sign is no longer available because the crown portfolio report is no longer published.

One way to fix an underperforming portfolio is to sell the dogs in the portfolio. One of the first ways owners notice dogs in their portfolio is the portfolio not returning as well as it used too because of the emergence of these dogs so further enquiries are made and explanations sought.

Taxpayers, ministers and parliamentarians are all busy people with little personal stake in the rate of return on the state owned enterprises portfolio.

Taxpayers, ministers and parliamentarians will all first look at the portfolio wide rate of return to see whether more detailed scrutiny of individual investments is required. That quick check against poor value for money and trouble ahead is no longer available on the state owned enterprises portfolio in New Zealand.

When I have sought the figures on the portfolio rate of return for the last two years through the Official Information Act to bring the table below up-to-date, I am told by Bill English that I can look up the annual reports of 49 state owned enterprises up for myself and do the calculation.

For that reason, the information on portfolio rates of returned for state owned enterprises, which I sought under the Official Information Act was publicly available and therefore the Treasury and the Minister of Finance both had a good reason under the legislation to turn my request down for access to that official information.

To put it mildly, the difference in credibility of a calculation of the rate of return of the portfolio of state owned enterprises made by the Treasury and by an angry blogger are beyond measure.

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

Ever since then, I regarded data chauvinism – the request for Australian evidence and studies or New Zealand evidence and studies – as a stalling tactic designed either to defend the status quo.

Ever since then, I regarded data chauvinism – the request for Australian evidence and studies or New Zealand evidence and studies – as a stalling tactic designed either to defend the status quo.

Hawke said that Thatcher said do you really want Malcolm Fraser beating down your door every day about apartheid. She had a point.

Hawke said that Thatcher said do you really want Malcolm Fraser beating down your door every day about apartheid. She had a point.

Recent Comments