Helpful distinctions for family thinking: structure, stability & strength (&.. how related) @inclusionist @mboteach http://t.co/zMi92WYUhi—

Richard V. Reeves (@RichardvReeves) January 13, 2015

The three S’s in family policy

18 May 2015 Leave a comment

in economics of education, gender, human capital, labour economics, labour supply, occupational choice, poverty and inequality, welfare reform Tags: child poverty, economics of marriage, family poverty, female labour force participation, labour force participation, male labour force participation, marriage and divorce, single parents, welfare reform

US imprisonment rates by race and education

18 May 2015 Leave a comment

in economics of crime, labour economics, law and economics, occupational choice Tags: crime and punishment, criminal deterrence, imprisonment rates

Paid sick day entitlements across the OECD membership

17 May 2015 Leave a comment

in economics of regulation, labour economics, labour supply, occupational choice Tags: employment law, employment protection laws, employment regulation

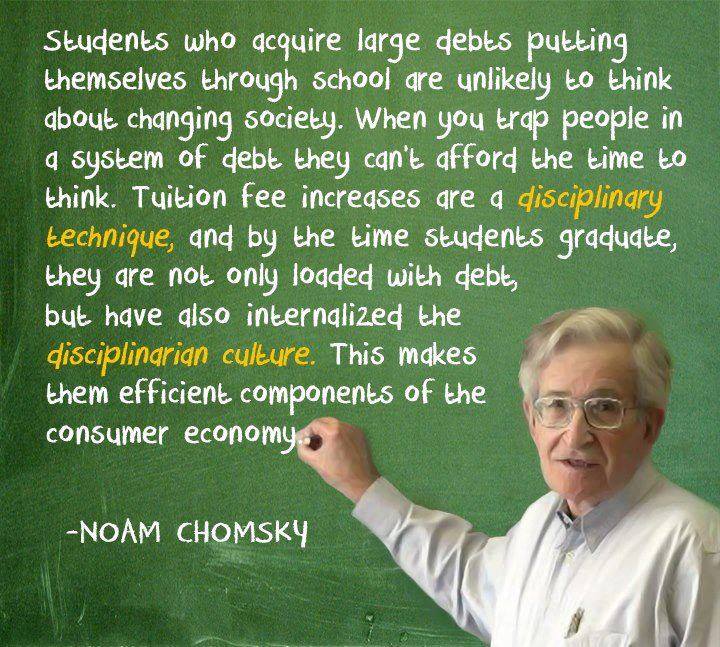

Who gains most from making higher education more accessible through loans and subsidised fees

16 May 2015 Leave a comment

in economics of education, human capital, labour economics, occupational choice, poverty and inequality Tags: free tertiary education, graduate premium, student loans

Wow. I mean, WOW. College completion figures over time by income quartile. bit.ly/16Bb1jh http://t.co/y0MVyiDCEZ—

Richard V. Reeves (@RichardvReeves) February 04, 2015

The main drivers of child poverty

15 May 2015 Leave a comment

in applied welfare economics, economics of love and marriage, gender, labour economics, labour supply, occupational choice, politics - Australia, politics - New Zealand, politics - USA, population economics, welfare reform Tags: child poverty, economics of the family, family poverty, marriage and divorce, single mothers, single parents

CHART: Black Illegitimacy Rate Went from < 20% in 1950 to 75.2% in 2010. Has Obama ever mentioned that? http://t.co/1UBUQ5aLRi—

Mark J. Perry (@Mark_J_Perry) May 12, 2015

Quotation of the Day from Charles Murray http://t.co/Y8W6xGjRPO—

Mark J. Perry (@Mark_J_Perry) May 12, 2015

The Rise and Rise of the Super Working Rich

15 May 2015 1 Comment

in economic history, entrepreneurship, financial economics, human capital, industrial organisation, labour economics, occupational choice, property rights, survivor principle, theory of the firm Tags: entrepreneurial alertness, Eugene Fama, Leftover Left, separation of ownership and control, super-rich, superstar wages, superstars, top 1%, Twitter left, working rich

The rise of the rentiers is nothing new. What is new is the degree of financial globalization and liberalization that has supercharged the fortunes of the super-wealthy even beyond robber baron levels. But it’s no mystery how to reverse this. It’s a matter of setting better rules for markets and taxing earners at the top a bit more.

In the course of a deranged rant against the entrepreneurs in society, the Atlantic collected an excellent set of information suggesting that the working rich have replaced rentiers as the super-rich. Rentiers are the idle rich. A rentier is a person or entity receiving income derived from patents, copyrights, interest, etc.

In The Evolution of Top Incomes: A Historical and International Perspective (NBER Working Paper No. 11955), Thomas Piketty and Emmanuel Saez concluded that:

While top income shares have remained fairly stable in Continental European countries or Japan over the past three decades, they have increased enormously in the United States and other English speaking countries.

This rise in top income shares is not due to the revival of top capital incomes, but rather to the very large increases in top wages (especially top executive compensation). As a consequence, top executives (the “working rich”) have replaced top capital owners at the top of the income hierarchy over the course of the twentieth century…

The Twitter Left claim that the surge in top compensation in the United States is attributable to an increased ability of top executives to set their own pay and to extract rents at the expense of shareholders. Obviously, from the chart below the pay the top 0.1% goes up and down with the share market. Top wages do not seem to have any independent power to dupe shareholders into overpaying them in bad times.

Xavier Gabaix and Augustin Landier found back in 2008 that what a major company’s CEO earns is directly proportional to the size of the firm that they are responsible for running. Executive compensation closely track the evolution of average firm value. During 2007 – 2009, firm value decreased by 17%, and CEO pay by 28%. During 2009-2011, firm value increased by 19% and CEO pay by 22%.

Xavier Gabaix and Augustin Landier also found that compensation for executives has risen with the market capitalization. From 1980 to 2003, the average value of the top 500 companies rose by a factor of six. Two commonly used indexes of chief executive compensation show close to a proportional six-fold matching increase.

Better executive decisions create more economic value. If the number of big companies is greater than the number of good chief executives, competitive bidding will push up executive pay to reflect the value of the talent that is available.

What happens to share prices when there is a surprise CEO resignation? Up or down? Apple went up and down in billions on news of Steve Jobs’ health.

When Hewlett Packard’s CEO Mark Hurd resigned unexpectedly, the value of HP stock dropped by about $10 billion! This makes his $30 million in annual compensation a bargain for shareholders. The fall in share price represents the difference between what the market expected from Hurd as Hewlett Packard’s CEO and what the market expects from his successor. Was Hurd under-paid?

There is an easy way to test for whether top executives cheat public shareholders. Compare the pay of large private companies, and public companies with a large or a few share holders, with public companies with diffuse share holdings. Private equity typically also pay its top executives very well, even though the capacity to dupe public shareholders are not a factor.

The burst of takeovers and leverage buyouts in the 1980s were very much driven by opportunities to profit from reducing corporate slack and downsizing flabby corporate headquarters of large publicly listed companies.

The response of the Left over Left of the day was support regulation to stop these mergers and takeovers rather than applauding them as giving lazy capitalists their comeuppance. This regulation undermined the market the corporate control rather than strengthened it as Michael Jensen explains:

This political activity is another example of special interests using the democratic political system to change the rules of the game to benefit themselves at the expense of society as a whole.

In this case, the special interests are top-level corporate managers and other groups who stand to lose from competition in the market for corporate control. The result will be a significant weakening of the corporation as an organizational form and a reduction in efficiency.

Central to the hypothesis of the Twitter Left of CEOs overpaying themselves is there is free cash within the business they pocket in pay rises, fringe benefits and lavished corporate headquarters rather than pay out in dividends or invest in profitable investments.

The interests and incentives of managers and shareholders frequently conflict over the optimal size of the firm and the payment of free cash to shareholders. What to pay the top executives is a minor manifestation of this common entrepreneurial difference of opinion the future of the business.

These conflicts in entrepreneurial judgements are severe in firms with large free cash flows–more cash than profitable investment opportunities. Jensen defines free cash flow as follows:

Free cash flow is cash flow in excess of that required to fund all of a firm’s projects that have positive net present values when discounted at the relevant cost of capital. Such free cash flow must be paid out to shareholders if the firm is to be efficient and to maximize value for shareholders.

Payment of cash to shareholders reduces the resources under managers’ control, thereby reducing managers’ power and potentially subjecting them to the monitoring by the capital markets that occurs when a firm must obtain new capital. Financing projects internally avoids this monitoring and the possibility that funds will be unavailable or available only at high explicit prices.

Michael Jensen developed a theory of mergers and takeovers based on free cash flows that explains:

- the benefits of debt in reducing agency costs of free cash flows,

- how debt can substitute for dividends,

- why diversification programs are more likely to generate losses than takeovers or expansion in the same line of business or liquidation-motivated takeovers,

- why bidders and some targets tend to perform abnormally well prior to takeover.

Michael Jensen noted that free cash flows allowed firms’ managers to finance projects earning low returns which, therefore, might not be funded by the equity or bond markets. Examining the US oil industry, which had earned substantial free cash flows in the 1970s and the early 1980s, he wrote that:

[the] 1984 cash flows of the ten largest oil companies were $48.5 billion, 28 percent of the total cash flows of the top 200 firms in Dun’s Business Month survey.

Consistent with the agency costs of free cash flow, management did not pay out the excess resources to shareholders. Instead, the industry continued to spend heavily on [exploration and development] activity even though average returns were below the cost of capital.

Jensen also noted a negative correlation between exploration announcements and the market valuation of these firms—the opposite effect to research announcements in other industries. Not surprisingly, after a successful corporate takeover, there is major changes to realise the untapped benefits they saw in the company that the incumbent management were not seizing capturing:

Corporate control transactions and the restructurings that often accompany them can be wrenching events in the lives of those linked to the involved organizations: the managers, employees, suppliers, customers and residents of surrounding communities.

Restructurings usually involve major organizational change (such as shifts in corporate strategy) to meet new competition or market conditions, increased use of debt, and a flurry of recontracting with managers, employees, suppliers and customers.

All modern theories of the focus in part or in full on reducing opportunistic behaviour, cheating and fraud in employment and commercial relationships. The market the corporate control, and mergers and takeovers realise large benefits from displacing underperforming manager teams. Premiums in hostile takeover offers historically exceed 30 percent on average. Acquiring-firm shareholders on average earn about 4 percent in hostile takeovers and roughly zero in mergers.

In terms of corporate control, Eugene Fama divides firms into two types: the managerial firm, and the entrepreneurial firm.

The entrepreneurial firms are owned and managed by the same people (Fama and Jensen 1983b). Mediocre personnel policies and sub-standard staff retention practices within entrepreneurial firms are disciplined by these errors in judgement by owner-managers feeding straight back into the returns on the capital that these owner-managers themselves invested. Owner-managers can learn quickly and can act faster in response the discovery of errors in judgement. The drawback of entrepreneurial firms is not every investor wants to be hands-on even if they had the skills and nor do they want to risk being undiversified.

The owners of a managerial firm advance, withdraw, and redeploy capital, carry the residual investment risks of ownership and have the ultimate decision making rights over the fate of the firm (Klein 1999; Foss and Lien 2010; Fama 1980; Fama and Jensen 1983a, 1983b; Jensen and Meckling 1976).

Owners of a managerial firm, by definition, will delegate control to expert managerial employees appointed by boards of directors elected by the shareholders (Fama and Jensen 1983a, 1983b). The owners of a managerial firm will incur costs in observing with considerable imprecision the actual efforts, due diligence, true motives and entrepreneurial shrewdness of the managers and directors they hired (Jensen and Meckling 1976; Fama and Jensen 1983b).

Owners need to uncover whether a substandard performance is due to mismanagement, high costs, paying the employees too much or paying too little, excessive staff turnover, inferior products, or random factors beyond the control of their managers (Jensen and Meckling 1976; Fama and Jensen 1983b, 1985).

Many of the shareholders in managerial firms have too small a stake to gain from monitoring managerial effort, employee performance, capital budgets, the control of costs and the stinginess or generosity of wage and employment policies (Manne 1965; Fama 1980; Fama and Jensen 1983a, 1983b; Williamson 1985; Jensen and Meckling 1976). This lack of interest by small and diversified investors does not undo the status of the firm as a competitive investment nor introduce slack in the monitoring of payments to top executives.

Large firms are run by managers hired by diversified owners because this outcome is the most profitable form of organisation to raise capital and then find the managerial talent to put this pool of capital to its most profitable uses (Fama and Jensen 1983a, 1983b, 1985; Demsetz and Lehn 1985; Alchian and Woodward 1987, 1988).

More active investors will hesitate to invest in large managerial firms whose governance structures tolerate excessive corporate waste and do not address managerial slack and and overpaid executives. Financial entrepreneurs will win risk-free profits from being alert and being first to buy or sell shares in the better or worse governed firms that come to their notice.

The risks to dividends and capital because of manifestations of corporate waste, reduced employee effort, and managerial slack and aggrandisement in large managerial firms are risks that are well known to investors (Jensen and Meckling 1976; Fama and Jenson 1983b). Corporate waste and managerial slack also increase the chances of a decline in sales and even business failure because of product market competition (Fama 1980; Fama and Jensen 1983b).

Investors will expect an offsetting risk premium before they buy shares in more ill-governed managerial firms. This is because without this top-up on dividends, they can invest in plenty of other options that foretell a higher risk-adjusted rate of return. The discovery of monitoring or incentive systems that induce managers to act in the best interest of shareholders are entrepreneurial opportunities for pure profit (Fama and Jensen 1983b, 1985; Alchian and Woodward 1987, 1988; Demsetz 1983, 1986; Demsetz and Lehn 1985; Demsetz and Villalonga 2001).

Investors will not entrust their funds to who are virtual strangers unless they expect to profit from a specialisation and a division of labour between asset management and managerial talent and in capital supply and residual risk bearing (Fama 1980; Fama and Jensen 1983a, 1983b; Demsetz and Lehn 1985). There are other investment formats that offer more predictable, more certain rate of returns.

Competition from other firms will force the evolution of devices within the firms that survive for the efficient monitoring the performance of the entire team of employees and of individual members of those teams as well as managers (Fama 1980, Fama and Jensen 1983a, 1983b; Demsetz and Lehn 1985). These management controls must proxy as cost-effectively as they can having an owner-manager on the spot to balance the risks and rewards of innovating.

The reward for forming a well-disciplined managerial firm despite the drawbacks of diffuse ownership is the ability to raise large amounts in equity capital from investors seeking diversification and limited liability (Demsetz 1967; Jensen and Meckling 1976; Fama 1980; Fama and Jensen 1983b; Demsetz and Lehn 1985). Portfolio investors may know little about each other and only so much about the firm because diversification and limited liability makes this knowledge less important (Demsetz 1967; Jensen and Meckling 1976; Alchian and Woodward 1987, 1988).

It is unwise to suppose that portfolio investors will keep relinquishing control over part of their capital to virtual strangers who do not manage the resources entrusted to them in the best interests of the shareholders (Demsetz 1967; Williamson 1985; Fama 1980, 1983b; Alchian and Woodward 1987, 1988).

Managerial firms who are not alert enough to develop cost effective solutions to incentive conflicts and misalignments will not grow to displace rival forms of corporate organisation and methods of raising equity capital and loans, allocating legal liability, diversifying risk, organising production, replacing less able management teams, and monitoring and rewarding employees (Fama and Jensen 1983a, 1983b; Fama 1980; Alchian 1950).

Entrepreneurs will win profits from creating corporate governance structures that can credibly assure current and future investors that their interests are protected and their shares are likely to prosper (Fama 1980; Fama and Jensen 1983a, 1983b, 1985; Demsetz 1986; Demsetz and Lehn 1985). Corporate governance is the set of control devices that are developed in response to conflicts of interest in a firm (Fama and Jensen 1983b).

At bottom, the private sector is highly successful designing forms of organisation that allow large sums of money, billions of dollars to be raised in the capital market and entrusted to management teams.

via The Rise and Rise of the Super-Rich – The Atlantic and How the Richest 400 People in America Got So Rich – The Atlantic.

Unskilled but Unaware of It

14 May 2015 Leave a comment

in economics of education, human capital, labour economics, labour supply, occupational choice Tags: cognitive psychology, Dunning-Kruger effect, economics of personality traits, educational psychology

The grammar test is the easiest explanation of the Dunning-Kruger effect. The only way to know you have bad grammar is to have good ground but as you don’t have good grammar you think you have good grammar because you don’t know you have bad grammar because you have no way of self-assessing your bad grammar because you don’t have good grammar.

Why is the gender gap so large and the glass ceiling so thick in Sweden?

14 May 2015 1 Comment

in discrimination, economics of love and marriage, gender, human capital, labour economics, occupational choice, politics - USA Tags: asymmetric marriage premium, do gooders, economics of families, gender wage gap, maternity leave, Sweden, The fatal conceit, unintended consequences

The gender wage gap is no better than the OECD average, despite generous maternity and paternity leave. What gives?

America: one day a year celebrating mothers, fathers.

Sweden: 480 days paid leave per child. vox.com/2014/5/12/5708… http://t.co/weFDrTj7Jb—

Ezra Klein (@ezraklein) May 11, 2015

Source: Closing the gender gap: Act now – http://dx.doi.org/10.1787/9789264179370-en

How big is the wage gap in your country? bit.ly/18o8icV #IWD2015 http://t.co/XTdntCRfDQ—

(@OECD) March 08, 2015

One important question is whether government policies are effective in reducing the gap. One such policy is family leave legislation designed to subsidize parents to stay home with new-born or newly adopted children.

One of the RLE articles shows that for high earners in Sweden there is a large difference between the wages earned by men and women (the so-called “glass ceiling”), which is present even before the first child is born. It increases after having children, even more so if parental leave taking is spread out.

These findings suggest that the availability of very long parental leave in Sweden may be responsible for the glass ceiling because of lower levels of human capital investment among women and employers’ responses by placing relatively few women in fast-track career positions. Thus, while this policy makes holding a job easier and more family-friendly, it may not be as effective as some might think in eradicating the gender gap.

via New volume on gender convergence in the labour market | IZA Newsroom.

Child poverty and single parenthood

13 May 2015 Leave a comment

in economics of love and marriage, gender, labour economics, labour supply, occupational choice, poverty and inequality, welfare reform Tags: child poverty, economics of marriage, family poverty, marriage and divorce, single mothers, single parents, welfare reform

Over half of all births to young adults in the U.S. now occur outside of marriage. bit.ly/1qONO10 http://t.co/KXl4sFd122—

Isabel Sawhill (@isawhill) September 17, 2014

Despite forgoing #marriage, young Americans are not forgoing parenthood. bit.ly/1sMG2bJ http://t.co/1aSELaJlfg—

Isabel Sawhill (@isawhill) October 31, 2014

Despite forgoing #marriage, young Americans are not forgoing #parenthood. bit.ly/1xLa1AJ http://t.co/fetnPAiCPG—

Isabel Sawhill (@isawhill) October 13, 2014

Almost 60% of births to women with only a high school degree occur out of wedlock. bit.ly/1sMG2bJ http://t.co/zomTFjZwA2—

Isabel Sawhill (@isawhill) October 14, 2014

Creative destruction in occupations

12 May 2015 Leave a comment

in labour economics, labour supply, occupational choice, personnel economics Tags: creative destruction, innovation, skill biased technological change

"The Changing Nature of Middle-Class Jobs" – via @nytimes nyti.ms/17Jzp1N http://t.co/2vRL6idiXt—

PewResearch FactTank (@FactTank) February 22, 2015

The primary school teachers union has done very well in New Zealand in recent times

12 May 2015 Leave a comment

in economics of bureaucracy, economics of education, labour economics, labour supply, occupational choice, Public Choice, rentseeking, unions Tags: public sector wage premium, union power, union wage premium

The average CEO in America earns about as much as the average dentist

12 May 2015 Leave a comment

in human capital, labour economics, labour supply, occupational choice, politics - USA, poverty and inequality Tags: CEO pay, top 1%

Women and Social Mobility – Key Facts

11 May 2015 Leave a comment

in discrimination, gender, labour economics, labour supply, occupational choice, politics - USA, population economics Tags: gender wage gap

How are today's baby boomer women faring compared to their #mothers? Check out these 6 facts: brook.gs/1J2Hq1l http://t.co/DMZG536cE3—

Brookings (@BrookingsInst) May 11, 2015

1. Today’s working women (henceforth described as “daughters”) have higher wages than their mothers – but do not have higher wages than their fathers. Men have higher wages than both their fathers and their mothers.

2. The poorest women are doing best. 80% of daughters raised in the bottom quintile have higher wages than their fathers did. (h/t Scott Winship)

3. “Men’s wages remain more important to increasing couples’ family income,” despite “women’s significant generational gains” …

4. Women who grew up in households where their mother did not work actually have the highest family incomes today—but not because they themselves earn more. Daughters’ individual incomes do not vary significantly by mother’s work status, but family income does—suggesting that daughters whose mothers didn’t work have higher earning husbands. (Catherine Rampell discovered this by asking Pew to split out their analyses by mothers’ labor choices.) Perhaps those raised in more traditional settings are more likely to replicate a traditional division of labor?

via via Women and Social Mobility: Six Key Facts | Brookings Institution.

Another gender gap that dare not mention its name

11 May 2015 Leave a comment

in discrimination, economics of education, gender, human capital, labour economics, occupational choice Tags: educational attainment, gender wage gap, reversing gender gap

Prediction: No commencement speaker will mention the huge ‘degree gap’ favoring women. ow.ly/MCiAm http://t.co/kzzNagctAk—

(@AEI) May 06, 2015

Recent Comments