Celebrating humanity's flourishing through the spread of capitalism and the rule of law

09 Oct 2014 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, great recession, macroeconomics, monetary economics Tags: crowding out, Earl A. Thomson, fiscal policy, great depression, great recession, permanent income hypothesis, Ricardian equivalence

03 Sep 2014 Leave a comment

in Austrian economics, business cycles, F.A. Hayek, fiscal policy, great depression, macroeconomics Tags: FA Hayek, General Theory, Keynes

02 Sep 2014 1 Comment

in Austrian economics, business cycles, economic growth, inflation targeting, monetarism, monetary economics, Murray Rothbard Tags: Austrian school of economics, business cycle, fractional reserve banking, hyperinflation, inflation, monetary business cycle, monetary cranks, quantity theory of money

I lost a good 15 minutes of my life that I will not get back on my deathbed listening to some monetary cranks at a Meet the Candidates forum last night for the New Zealand general election.

Monetary cranks advocate boundless inflation and credit expansion as the patent medicine for all our economic ills:

those who have Found the Light about Money take up their pens and write, with a conviction, a persistence and a devotion otherwise only found among the disciples of a new religion.

It is easy to scoff at these productions: it is not so easy always to see exactly where they go wrong. It is natural that practical bankers, vaguely conscious that the projects of monetary cranks are dangerous to society, should cling in self-defence to the solid rock, or what they believe to be so, of tradition and accepted practice. But it is not open to the detached student of economics to take refuge from dangerous innovation in blind conservatism.

D.H. Robertson (1928)

Listening to these monetary cranks in the audience last night rates with the worst movies I have ever ever seen for time I want back my deathbed. I think the worst movie I have ever seen was Absolute Beginners starring David Bowie. After that it, might be Last Tango in Paris.

These particular monetary cranks with their obsessions about factional reserve banking are from the social credit party in New Zealand. They are followers of Major C.H. Douglas, whom Keynes referred to as a:

private, perhaps, but not a major in the brave army of heretics

Social credit and other monetary cranks believe that all the world’s problems will be sold if the reserve bank prints money and they seem to think that was really easy because there is a fractional reserve banking system.

No one in the room who knew better wanted to lose more time that they wanted back on their deathbed explaining why printing money doesn’t make you richer. The “money is wealth” error is the defining affliction of the monetary crank.

The good economist will know that money creation is no short-cut to wealth. Only the production of valued goods and services in a market which reflects the consumer’s willingness to pay can relieve poverty and promote prosperity. A people are prosperous to the extent they possess goods and services, not money. All the money in the world—paper or metallic—will still leave one starving if goods and services are not available.

Obviously, none of them were persuaded by the quantity theory of money: if you increase the supply of money without a matching increase in the rate of real growth in the production of goods and services, you’ll have more money chasing the same amount of goods so prices will go up. It’s called inflation. Printing money creates inflation.

There is a school of thought in economic school, the Austrian school of economics, does get excited about fractional reserve banking. The reason it does is to explain how fractional reserve banking creates inflation and promotes the business cycle.

A cycle of booms and busts is not looked upon as a good thing by the Austrian school of economics.

The Austrian school wants to get rid of fractional reserve banking as a way of reducing inflation and reducing the possibility of a loose monetary policy causing booms and busts in the economy.

These monetary cranks from social credit party honestly believed that printing more money will make you wealthier. Thankfully no one asked them to explain their position.

A few supporters of the monetary cranks in the audience asked other members of their views on the ideas of these monetary cranks. Sensibly, they all gave short answers that did not provoke them further and waste more of their precious life listening to them talk nonsense.

If printing money was a winner, as with any populist policy that has a half a chance of working, the parties of the centre-left and centre right would be all over it like flies to s…

04 Aug 2014 Leave a comment

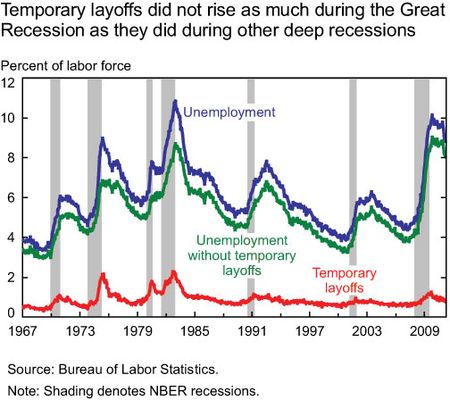

in business cycles, job search and matching, labour economics, labour supply, macroeconomics, occupational choice, unemployment Tags: recall unemployment, rest unemployment, temporary layoffs, waiting unemployment, work for the dole

Time use surveys in a range of countries show that the unemployed spend maybe a few hours per week looking for a new job. Krueger and Mueller (2008) found that:

…average search time is highest in the U.S.A., at 32.3 minutes per day, closely followed by Canada.

Europeans search much less, but there is considerable variation across countries.

In France the unemployed search around 21 minutes a day compared with 3 minutes in Finland

A small amount of job search per week is rational for many of the unemployed because a major form of job search doesn’t involve any job search any time soon. Instead, they are waiting for a call.

Also, Anglo-Saxon labour market are much more dynamic with many more vacancies opening every month as compared with the Eurosclerosis dual labour markets. In the European Union’s dual labour markets, it is not rational to search for vacancies that will never be there.

Job searches is an entrepreneurial venture that can involve a considerable amount of biding your time. Job seekers must choose between wider job search that may involve switching to a new industry or new occupation and investing in availability for suitable vacancies in their local labour markets or a recall to employment by old employers.

A spell of unemployment followed by a rehire by an old employer is known as recall unemployment or a temporary layoff.

Demand is less stable and more seasonal in industries such as construction, manufacturing and agriculture. When demand rebounds, recalling an old employee is a faster and cheaper hiring process than screening unfamiliar applicants of uncertain quality and training recruits.

Recall is not certain. Temporary layoffs will forecast their chances of recall and review these forecasts as they discover more about the length of drop in local labour demand and the general state of the rest of the labour market. the majority of unemployed who regard themselves as temporary layoffs are indeed recalled to their old job by their old employer after most downturns.

Better prospects of recall by old employers will reduce the intensity of job searches of temporary layoffs and increase their asking wages for other jobs. Workers with considerable industry and firm-specific human capital are likely to risk waiting longer for recall. Workers will search more intensively for other jobs as their forecasts of their chances of recall to old jobs become less encouraging.

There are more temporary layoffs in milder recessions because the lull in demand is expected to be short and there are fewer business closures. The higher levels of recall unemployment will reduce downward pressure on asking wages and slow the filling of vacancies because many well qualified job applicants are waiting for recall to their old jobs rather than applying more widely for new jobs.

Dixon and Crichton (2006) found that 58% of New Zealand benefit-to-work transitions involved starting with a new employer, 30% continued with an employer for whom they worked part-time in the benefit spell and 12% returned to an employer they had worked for in the past 2 years. The prospect of a recall by an old employer has been important for unemployed workers in countries such as the US, Canada, Demark, Sweden, Austria and Norway.

In the context of work-for-the-dole schemes and activation programmes that involve intensive monitoring of job search by the unemployed on unemployment benefits, requiring workers who are temporarily laid off to search for jobs is in many ways counter-productive.

Developing a screening mechanism to find these temporary layoffs and distinguishing them from permanent layoffs would be quite challenging. Countries which have unemployment insurance premiums spend a lot of try trying to adjust those premiums for temporary layoffs. This is so employers and employees do not take advantage of unemployment insurance to have a week or two off work in slack periods at the expense of the unemployment insurance system and top up their wages in the interim.

A cousin of recall unemployment is rest unemployment or waiting unemployment – job seekers who are waiting for conditions in a depressed sector to improve (Hamilton 1988; Alvarez and Shimer 2008).

Some job seekers may wait for local labour market conditions to improve, rather than search for jobs in other industries and new occupations. A job seeker’s old industry may offer better wage and job finding prospects than other industries If the newly unemployed worker waits a while.

Rest unemployment or waiting unemployment strives to salvage as much of the occupation and industry-specific human capital of the newly unemployed worker as possible.

A significant share of job seekers have been found to be waiting for local labour market conditions to improve rather than searching further afield in different industries or new occupations (Alvarez and Shimer 2008).

Again, rest unemployment or waiting unemployment is a type of job search that cannot be well handled by work-for-the-dole schemes and intensive monitoring of the job search of unemployed workers.

03 Aug 2014 6 Comments

in business cycles, job search and matching, labour economics, labour supply, macroeconomics, welfare reform Tags: Active labour market programs, Jeff Borland, mandatory work requirements, search and matching, welfare reform, work for the dole

Jeff Borland is a critic of work for the dole. He points out that they do not improve the job finding rates of participants and in fact reduce the amount of job search because work for the Dole participants are busy undertaking work for the dole requirements:

The main reason is that participation in the program diverts participants from job seeking activity towards Work for the Dole activity. Research on similar programs internationally has come up with comparable findings.

This made me wonder. If unemployment is caused by deficient aggregate demand, and otherwise is involuntary, how can work for the dole increase unemployment or reduce the rate at which people exit unemployment?

‘Involuntary’ unemployment occurs when all those willing and able to work at the given real wage but no job is available, i.e. the economy is below full employment. A worker is ‘involuntary’ unemployment if he or she would accept a job at the given real wage. Keynesians believe money wages are slow to adjust (e.g. due to money illusion, fixed contracts or because employers and employees want long run money wage stability), and so the real wage may no adjust to clear the labour market: there can be ‘involuntary’ unemployment.

Under the deficient aggregate demand theory of unemployment, people have no control over why they are unemployed – that’s why their unemployment is involuntary.

Sticky wages are no less sticky when work for the dole is introduced and people search more intensively for jobs. Deficient demand unemployment is no less deficient when there is an increase in job search intensity.

Work for the dole must be carefully defined, of course, to differentiate it from the failed active labour market programs of the past that attempted to improve the employability of the unemployed. By work for the dole, I simply mean mandatory work requirements simply make it more of an ordeal to be on unemployment and thereby encourage people to find a job.

Mandatory work requirements simply tax leisure. By taxing leisure, mandatory work requirements change the work leisure trade-off between unemployment and seeking a job with greater zeal and a lower asking wage more attractive option. More applicants asking for lower wages will mean employers can fill jobs faster and at lower wages, which means our create more jobs in the first place.

The probability of finding a job for an unemployed worker depends on how hard this individual searches and how many jobs are available: Chance of Finding Job = Search Effort x Job Availability

Both the search effort of the unemployed and job creation decisions by employers are potentially affected by unemployment benefit generosity and mandatory work for welfare benefits requirements.

Modern theory of the labour market, based on Mortensen and Pissarides provides that more generous unemployment benefits put upward pressure on wages the unemployed seek. If wages go up, holding worker productivity constant, the amount left to cover the cost of job creation by firms declines, leading to a decline in job creation.

Everything else equal under the labour macroeconomics workhorse search and matching model of the labour market, reducing the rewards of being unemployed exerts downward pressure on the equilibrium wage. This fall in asking wages increases the profits employers receive from filled jobs, leading to more vacancy creation. More vacancies imply a higher finding rate for workers, which leads to less unemployment. The vacancy creation decision is based on comparing the cost of creating a job to the profits the firm expects to obtain from hiring the worker.

When unemployment benefits are less generous or more onerous work requirements are attached, some of the unemployed will become less choosey about the jobs they seek in the wages they will accept. a number of people at the margin between working or not. An example is commuting distance to jobs. A number of people turn down a job because is just that little too far to commute. A small change in the cost of accepting that job would have resulted in them moving from being unemployed to fully employed.

Unemployment is easy to explain in modern labour macroeconomics: it takes time for a job seeker to find a suitable job with a firm that wishes to hire him or her; it takes time for a firm to fill a vacancy. Search is required on both sides of the labour market – there are always would-be workers searching for jobs, and firms searching for workers to fill vacancies.

In a recession, a large number of jobs are destroyed at the same time. It takes time for these unemployed workers to be reallocated new jobs. It takes time for firms to find where it is profitable to create new jobs and find workers suitable to fill these new jobs.

Recessions are reorganisations. Unemployed workers look for jobs, and firms open vacancies to maximize their profits. Matching unemployed workers with new firms firms is a time-consuming and costly process.

02 Aug 2014 Leave a comment

in business cycles, macroeconomics Tags: Fonterra, real business cycle theory

One contaminated pipe at a milk processing factory of New Zealand’s largest company, Fonterra, New Zealand’s largest company (7% of GDP) and largest exporter caused such a loss of brand-name value of the company that the New Zealand Treasury revised down its GDP forecasts for the year.

It is a little bit scary to wonder what kind of nation we live in when a single, small, dirty pipe threatens to bring the nation to its knees. That indeed was the fear when, over the weekend, Fonterra announced the contamination of a small amount of whey powder from a Waikato processing plant – Bank of New Zealand

This growth forecast revision after the milk contamination scandal, but turn out to be false reading, is a good example of how the random fortunes of individual large companies can have economy-wide implications and can even lead to recessions.

Source: (Gabaix 2011).

There is growing evidence that idiosyncratic shocks to the fortunes of the 100 largest firms arising from changes in demand and cost conditions in their local and export markets combine to contribute about one-third of up-swings and downswings in U.S. output and employment (Gabaix 2011).

In an economy dominated by a few large firms, idiosyncratic shocks to large firms do not cancel out. The ups and downs in the individual fortunes of very large firms combine with firm-to-firm linkages to travel far beyond the firm and sector of origin (Gabaix 2011). These effects are likely to be stronger outside of the USA because it has a more diversified economy than most countries (Gabaix 2011).

Di Giovanni and Levchenko (2010) found that having fewer and less diversified firms and exports dominated by large firms helps to explain why small, more open economies such as New Zealand are more volatile. Fonterra accounts for 7 per cent of GDP and 20 per cent of overall exports. Drought is important to the New Zealand business cycle and agricultural exports (Buckle, Kim, Kirkham, McLellan and Sharma 2007).

As another example of the importance of a few large firms, Samsung and Hyundai account for 35 per cent of Korean exports and 22 per cent of Korean GDP.It would not be a good idea for the chief executives of those two Korean businesses to travel in the same car and have an accident.

Finland was monikered the one-firm economy because Nokia was responsible for 1/5th of Finnish economic growth, exports and company tax revenues for two decades. Nokia shares initially fell by 90 per cent in 2007 when Apple leap-frogged it with an iPhone that resembled a PC. The loss of one product development race imperilled the foundation of one-fifth of Finnish economic growth.

The literature on the contribution of large firms to business cycle volatility is a good examples of how the real business cycle theory is alive and well and is a progressive research programme.

28 Jul 2014 Leave a comment

in business cycles, macroeconomics, Milton Friedman, monetarism Tags: boom and bust, Milton Friedman, plucking model, recoveries from recessions

Milton Friedman (1993) proposed a model of the depth of recessions and steepness of recoveries built on two empirical regularities:

The strength of a recovery should be positively correlated with depth of the recession but there should be no correlation between expansions and recessions (Friedman 1993; Alchian 1969).

The figure below illustrates Friedman’s model, which likens the time path of output to a string on the underside of an upward sloping board that is plucked downward at random intervals to various extents into busts that are followed by booms.

Source: Garrison (1996).

The upward sloping board plotted as a thick line in the figure represents a ceiling on feasible output and employment in a given year that is set by resource and technology availabilities. The upward slope of this board accounts for trend real GDP growth over time due to technological progress and other factors.

The business cycle starts with a bust caused by an adverse policy or other shock and is then followed by a boom as the market self-adjusts and the policy errors are reversed. Without the initial adverse policy or other shock, there would neither be a bust nor a boom.

The correlation between busts and booms arises from the monetary contraction that caused the bust eventually inducing an offsetting correction in monetary policy.

The monetary contraction that pushed or plucked output below the upward sloping ceiling is later followed by a monetary expansion that offset the earlier contraction. With the amplitude of monetary expansions correlated to offset the prior contractions, GDP growth will have similar plucks or falls and rebounds to the upward sloping output ceiling because of the link albeit with a lag between monetary growth and output fluctuations. The increases and decreases in monetary growth are independent policy choices with unique causes.

The associated upward and downward movements in GDP growth are not correlated with each other but should be correlated with the prior fluctuations in monetary growth. There would not be a bust and later boom if there is no monetary contraction to start the cycle. This is why Friedman (1993) proposed that the depths of busts are unrelated to the duration and strength of prior economic booms.

25 Jul 2014 Leave a comment

in business cycles, inflation targeting, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: leads and lags on monetary policy, Milton Friedman, monetary policy

Many Keynesians, Friedman notes, advocate “leaning against the wind.” By this they mean, in some sense, that the monetary (and fiscal) authorities should try to balance out the private sector’s excesses rather than passively hope that it adjusts on its own.

There are large uncertainties about the size and timing of responses to changes in monetary policy. There is a close and regular relationship between the quantity of money and nominal income and prices over the years. However, the same relation is much looser from month to month, quarter to quarter and even year to year.

Monetary policy changes take time to affect the economy and this time delay is itself highly variable. The lags on monetary policy are three in all:

The lag between recognition and the taking of action (the legislation lag)

the lag between action and its effects (the implementation lag)

These delays mean that is it difficult to ascertain whether the effects of monetary policy changes in the recent past have finished taking effect. Secondly, it is difficult to ascertain when proposed changes in monetary policy will take effect. Thirdly, feedbacks must be assessed. The magnitude of the monetary adjustment necessary to deal with the problem at hand is thus never obvious. It is common for a central bank to act incrementally. The central bank makes small adjustments to monetary conditions over time as more information is available on the state of the economy and forecasts are updated.

The existence of lags may mean that by the time policy has its full effect, the problem with which it was meant to deal may have disappeared.

Milton Friedman (1959) tested the Fed’s success at leaning “against the wind” by checking whether the rate of money growth has truly been lower during expansions and higher during contractions. He admits that this method of grading he Fed’s performance is open to criticism, but he decided to go ahead and see what turns up. Friedman found that Fed has – for the periods surveyed – been unsuccessful.

By this criterion, for eight peacetime reference cycles from March 1919 to April 1958. Actual policy was in the ‘right’ direction in 155 months, in the ‘wrong’ direction in 226 months; so actual policy was ‘better’ than the [constant 4% rate of money growth] rule in 41% of the months.

Nor is the objection that the inter-war period biased his study is good since Friedman found that:

For the period after World War II alone, the results were only slightly more favourable to actual policy according to this criterion: policy was in the ‘right’ direction in 71 months, in the ‘wrong’ direct in 79 months, so actual policy was better than the rule in 47% of the months.

One of the best ways to parry a metaphor is with another metaphor. Keynesians have a host of metaphors in their rhetorical arsenal; one frequently voiced is that a wise government should “lean against the wind” when choosing policy. Friedman counters:

We seldom know which way the economic wind is blowing until several months after the event, yet to be effective, we need to know which way the wind is going to be blowing when the measures we take now will be effective, itself a variable date that may be a half year or a year or two from now. Leaning today against next year’s wind is hardly an easy task in the present state of meteorology.

Friedman’s remarks, as even his strong critics admit, are mighty and strike at the heart of any activist stabilisation policy. By meeting Keynesians on their own theoretical turf and scrutinising their practice, Friedman manages to produce objections that both Keynesians and non-Keynesians must take seriously. A key part of any response to Friedman rests on the ability of forecasters to do their jobs with tolerable accuracy.

Keynesian policies do not necessarily follow even if the Keynesian theory of the business cycle were conclusively proved. It must also be demonstrated that the government has the ability and willingness of the government to act as the theory prescribes. Friedman’s critique does not depend on the quantity theory of money.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Economics, public policy, monetary policy, financial regulation, with a New Zealand perspective

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Restraining Government in America and Around the World

Recent Comments