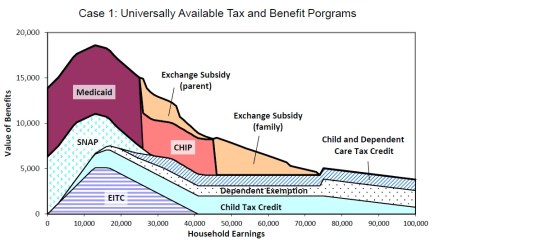

One in five Americans on Medicaid; this image does not include those on Medicare –those over 65 who get their healthcare paid by the government.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

08 Dec 2014 Leave a comment

in fiscal policy, income redistribution, labour economics, labour supply, politics - USA, public economics, welfare reform Tags: effective marginal tax rates, Obama care, poverty traps, welfare reform

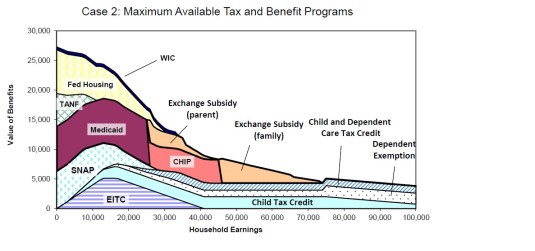

One in five Americans on Medicaid; this image does not include those on Medicare –those over 65 who get their healthcare paid by the government.

06 Dec 2014 Leave a comment

in business cycles, fiscal policy, global financial crisis (GFC), great recession, macroeconomics, monetary economics, politics - USA Tags: Macroeconomics

18 Nov 2014 Leave a comment

in applied welfare economics, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics Tags: Edward Prescott, real business cycle theory

The extension of recursive methods to dynamic equilibrium modelling spawned a revolution in aggregate economics.

This revolution has resulted in aggregate economics becoming, like physics, a hard science and not exercises in storytelling.

Operations research played a major role in the development of practical methods to model dynamic aggregate economic phenomena and to predict the consequences of policy regimes.

Subsequently recursive methods were used to develop a quantitative theory of aggregate fluctuations and other aggregate phenomena.

07 Nov 2014 Leave a comment

in applied price theory, fiscal policy, politics - New Zealand Tags: Marginal tax rates, public economics, public finance

Note: Average marginal tax rate calculations exclude the impact of ACC levies, the Benefit system and the Family Tax Credit (FTC) system which, at various times since the 1970s, involved lump sum transfers to lower income families with children that were withdrawn at higher income levels at rates of up to 30c/$, thereby adding to effective MTRs.

Comment: The average marginal tax rate has been pretty stable in New Zealand since about 1990 excepting for a drop in the late 1990s and then an increase in 1999.

via http://www.treasury.govt.nz/publications/research-policy/wp/2012/12-04

31 Oct 2014 3 Comments

in budget deficits, business cycles, comparative institutional analysis, economics of religion, fiscal policy, global financial crisis (GFC), great recession, macroeconomics

31 Oct 2014 Leave a comment

in economic growth, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, macroeconomics Tags: Eurosclerosis, GFC, Great Geviation, great recession

Figure 1: Actual and potential GDP in the US

Sources: Congressional Budget Office, Bureau of Economic Analysis

Figure 2: Actual and potential GDP in the Eurozone

Sources: IMF World Economic Outlook Databases, Bloomberg

HT: Larry Summers

31 Oct 2014 5 Comments

in fiscal policy, global financial crisis (GFC), macroeconomics, monetary economics Tags: GFC, Ireland

I am planning to blog on why the Irish economic crisis of recent years was caused exclusively by government, and in particular, government responses that made an ordinary recession into a depression

Roger Kerr, New Zealand Business Roundtable Executive Director

This is a graph courtesy of the Institute of Public Affairs in Melbourne, an impressive Australian thinktank.

It comes from the Irish government’s own 140 page ‘National Recovery Plan‘ published last week.

It is amazing reading.

Naysayers try to tell you that the Celtic Tiger was a myth and that free-market policies brought the Irish economy down.

The truth is exactly the opposite. Liberalisation caused the Irish economy to surge until a return to big government crushed it. Membership of the eurozone, poor banking regulation and the government guarantee of…

View original post 34 more words

19 Oct 2014 Leave a comment

in business cycles, fiscal policy, global financial crisis (GFC), macroeconomics, Public Choice Tags: GFC, Ireland

Dot point 4 is the key. The bank guarantee caused the depression.

Roger Kerr, New Zealand Business Roundtable Executive Director

Philip Lane is Professor of International Macroeconomics at Trinity College Dublin. He is also a managing editor of the journal Economic Policy, the founder of The Irish Economy blog, and a research fellow of the Centre for Economic Policy Research. His research interests include financial globalisation, the macroeconomics of exchange rates and capital flows, macroeconomic policy design, European Monetary Union, and the Irish economy.

Last week he visited New Zealand as a guest of the Treasury, the Reserve Bank, and Victoria University. During his visit he presented this guest lecture on the troubled Irish economy, drawing on his recent report to the Irish Parliament’s finance committee on ‘Macroeconomic Policy and Effective Fiscal and Economic Governance’.

Some highlights from his talk (also reported here by Brian Fallow in the New Zealand Herald) were:

View original post 216 more words

19 Oct 2014 Leave a comment

09 Oct 2014 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, great recession, macroeconomics, monetary economics Tags: crowding out, Earl A. Thomson, fiscal policy, great depression, great recession, permanent income hypothesis, Ricardian equivalence

27 Sep 2014 Leave a comment

HT: Robert P. Murphy

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments