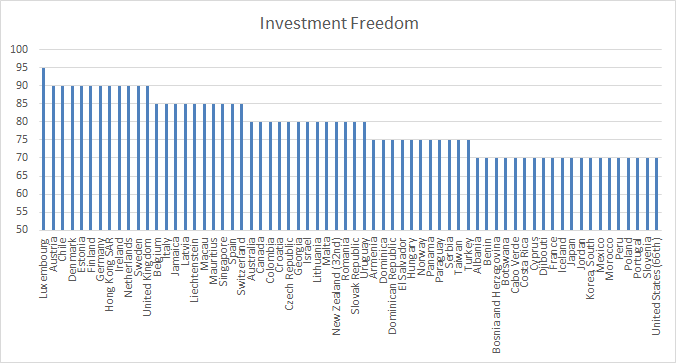

Source: 2015 Index of Economic Freedom

According to the Index of Economic Freedom 2015, in New Zealand

Foreign investment is welcomed, but the government may screen some large investments.

There was a major review of New Zealand foreign investment regulations about 10 years ago. The purpose of that review commissioned by the Labour government’s Minister of Finance, Dr Michael Cullen, was to deregulate the regulation of foreign investment in New Zealand.

At the time,under the Overseas Investment Act, the Minister of Finance could refuse permission to any investment. Australia’s current overseas investment regulations are the same. The federal treasurer may reject foreign investment proposals on the basis of an open-ended definition of national interest.

The last time that foreign investors had been refused permission to invest in New Zealand was in the early 1980s under then National Party Government Prime Minister Robert Muldoon. In a fit of pique, he refused permission to an Australian investor.

The revised foreign investment regulations limits the ability of government to reject foreign investors to narrow criteria such as the acquisition of sensitive land and large New Zealand companies. As part of this theme that foreign acquisitions of land was the main policy concern regarding foreign investment, the administration of the foreign investment regulations was moved out of a Overseas Investment Commission housed at the Reserve Bank of New Zealand to the very low key Land Information Office:

The Overseas Investment Office (OIO) assesses applications from overseas investors seeking to invest in sensitive New Zealand assets – being ‘sensitive’ land, high value businesses (worth more than $100 million) and fishing quota.

Naturally, subsequent to this genuine attempt by the Labour government of 10 years ago to deregulate foreign investment regulation, a number of investments have been refused since then often on the pretext that some part of the investment acquired sensitive coastal land door or rural land. The criteria for regulating foreign investment is as follows:

As regards the criteria relating to the relevant “overseas person”, the OIO needs to be satisfied that:

- the “overseas person” has demonstrated financial commitment to the investment; and

- the “overseas person” or (if that person is not an individual) the individuals with ownership and control of the overseas person (such as the shareholders and directors of the overseas purchaser):

- have the business experience and acumen relevant to that investment;

- are of good character; and

- are not prohibited from entering New Zealand by reason of sections 15 or 16 of the Immigration Act 2009 (e.g. persons who have been imprisoned for certain periods of time).

As regards the criteria relating to the particular investment, the OIO needs to be satisfied that the overseas investment will, or is likely to, benefit New Zealand (or any part of it or group of New Zealanders). When considering this, the OIO has a range of factors that it must consider (including, for example, whether the investment will create new job opportunities, introduce new technology or business skills, advance a significant Government policy or strategy, or bring other consequential benefits to New Zealand).

The New Zealand Initiative recently reviewed this criteria for regulating overseas investment into New Zealand and found that:

the report finds that the criteria for approval do not test the economic benefit to New Zealanders, where sensitive land is sold to an overseas person not intending to live in New Zealand indefinitely.

Indeed, the criteria are unambiguously hostile, even excluding the gain to a New Zealand vendor. This opens the way for the imposition of approval conditions that could impose net costs on New Zealanders given the regime’s potentially adverse effects on land values

The regulation of foreign investment in other countries is much more specific about what it is trying to achieve,as New Zealand Initiative also noted in its recent review:

New Zealand’s comprehensive screening regime accounts for our poor international ranking in the OECD’s FDI Regulatory Restrictiveness Index.

Most other countries focus their regimes more narrowly on national security considerations, often relating to particularly sensitive industries or sectors.

The main reason the public supports foreign investment regulation is because the public doesn’t like foreigners, and politicians pander to that xenophobia. If foreign investment is reduced, more of total investment spending has to be funded from domestic saving.

Access to foreign savings – trade in savings – allows investment to be made sooner, consumption to be smoothed over hiatuses such as recessions, and consumption to be bought forward in the light of better times such higher output and higher future incomes as because of foreign investment.The

The large national gains from foreign capital inflows is not part of that debate. A recent review of the gains from foreign capital inflows to New Zealanders found access to foreign saving led to national income per head, net of the servicing cost of foreign capital:

- average income gains of $2,600 per worker arising on a cumulative basis from capital inflow over the period 1996 – 2006; and

- growth in the value of New Zealand’s assets has greatly exceeded the rise in external liabilities to the extent that national wealth per head has risen by $14,000 in 2007 prices between 1996 and 2006.

You can’t let facts bugger a good story.

The foreign investment is in response to the high returns in the local market and the inflow of foreign capital will continue until local rates of return match those in other countries. Equalisation of risk-adjusted rate of returns is central to the operation of capital markets.

Stopping this process of equalisation of returns on capital through regulation only benefits the capitalists inside the country because the curbing of foreign investment stops rates of return falling to those overseas. Foreign investment regulation reduces the wages of New Zealand workers because they have less capital and fewer modern technologies to work with.

Fortunately, local capitalists can work in league with economic populists on the left and the right and the anti-foreign bias of the voting public to make it more difficult for foreign investors to come to New Zealand and drive down the profits of New Zealand capitalists. Who gains from that? As Paul Krugman said:

The conflict among nations that so many policy intellectuals imagine prevails is an illusion; but it is an illusion that can destroy the reality of mutual gains from trade.

Recent Comments