Global and Korean economic forecasts by Edward Prescott

17 Jul 2019 Leave a comment

in budget deficits, business cycles, development economics, economic growth, Edward Prescott, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, growth miracles, macroeconomics, monetary economics Tags: real business cycles

FGV/EPGE – 3rd Conference Business Cycles – Edward C. Prescott 2/15

14 Jul 2019 Leave a comment

in budget deficits, business cycles, economic growth, economic history, Edward Prescott, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, monetary economics Tags: real business cycles

Nobel Symposium Harald Uhlig Modern DSGE models: Theory and evidence

17 Aug 2018 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, great recession, macroeconomics, monetary economics Tags: real business cycles

Nobel Symposium Ellen Mcgrattan Modern DSGE models: Theory and evidence

16 Aug 2018 Leave a comment

in business cycles, economic growth, global financial crisis (GFC), great recession, macroeconomics Tags: real business cycles

Ellen McGrattan, Intangible Capital and Measured Productivity

14 Aug 2018 Leave a comment

in business cycles, global financial crisis (GFC), great recession, macroeconomics, monetary economics Tags: real business cycles

Randall Wright on the mundaneness of real business cycle theory revolution

26 Jul 2018 Leave a comment

in business cycles, economic growth, macroeconomics Tags: real business cycles

Business Cycles – Edward C. Prescott

25 Mar 2017 Leave a comment

in business cycles, development economics, economic growth, economic history, financial economics, fiscal policy, macroeconomics Tags: Edward Prescott, real business cycles

Sectoral shifts in labour demand and the business cycle

01 Mar 2017 Leave a comment

in business cycles, labour economics, macroeconomics Tags: real business cycles, sectoral shifts

Random sector-specific technology shocks

New technologies unfold daily, and consumer tastes change with rising incomes and the arrival of new products. Jobs will open in the expanding industries and disappear in the shrinking sectors. This chapter is about how these sectoral reallocations of labour can cause a recession or prolong existing recessions.

A quarter or more of unemployment rate fluctuations over the business cycle could be due to variations in the rate that labour demand shifts across sectors. These sectoral reallocations in labour demand do not arise from mismatches between entrepreneurial forecasts and actual consumer demand. The higher unemployment rate is not due to a bunching of technological upgrades in a recession. The above average number of sectoral shifts in labour demand is an independent cause of a temporarily higher natural rate of unemployment.

To a significant extent, observed fluctuations in the unemployment rate can be fluctuations in the natural rate of unemployment rather than deviations from that natural rate due, for example, to aggregate demand shocks. There will always be some unemployment. There will be new labour force entrants looking for jobs and workers who are between jobs.

The natural rate of unemployment is a long-run level of unemployment that cannot be altered by monetary policy. The natural rate of unemployment depends on the flexibility of wage contracts and labour market institutions, variations in labour demand and supply in individual markets, demographic change, the mobility of workers, unemployment benefits, the cost of gathering information about vacancies and available labour, labour market regulation and random variations in the rate of reallocation of jobs across industries and regions as technology advances and consumer tastes change.

Sectoral shifts and delayed recoveries in employment

Some years can see relatively uniform growth in labour demand across sectors. Other times can see more dramatic sectoral shifts in labour demand arise out of technological progress and changes in consumer demand.

Instead of significant but steady amounts of unemployment because of labour reallocations across sectors, these job reallocations can vary significantly from one year to the next. The natural rate of unemployment can be higher in these intervals because more job seekers are undertaking the more time-consuming process of searching for jobs in new industries and/or occupations, are relocating or are undertaking retraining.

Sectoral shifts in labour demand has a randomness about them because the size, pace and diffusion of technological advances across firms and industries is uneven (Andolfatto and MacDonald 1998, 2004). The implications of technological progress for jobs has a further randomness because new technologies can displace existing jobs and create new jobs or renovate and update current equipment and employee skills (Mortensen and Pissarides 1998).

As a new technology diffuses, productivity will grow faster in the sectors that are adopting the new technology. During this implementation phase, which is slow, costly and may require considerable learning, there will be reorganisations to capitalise on the impending productivity gains.

New technologies differ in the size of the improvement over existing methods and designs and in the difficulty of adopting the new methods. There will be lower growth in years where new technologies offer comparatively minor or less broadly applicable improvements on existing methods.

Learning consumes resources, and attempts to learn a new technology through innovation or imitation diverts the resources of firms and workers away from production (Andolfatto and MacDonald 1998, 2004). This unevenness in the pace and sectoral diffusion of technological progress will introduce unevenness in the rate of labour reallocation across sectors.

With both growing and shrinking sectors, employment may stagnate or fall for a time because the unemployed are searching for new jobs in different industries and perhaps in new occupations or are retraining. A revival in growth in output and productivity in conjunction with initially poor employment growth is possible and has the attributes of a delayed recovery in employment (Andolfatto and MacDonald 2004). Cross-sector job searches and the redirection of careers is a longer process than job search in the same industries and occupations. Job migration is more time consuming than the more traditional process of layoffs and rehiring by the same employer or in the same industry and occupation.

Labour reallocation and mismatch unemployment

During periods of more intensive or above-average sectoral reallocation of labour demand, a mismatch can arise between the skills and experience of the workers who have exited the shrinking sectors and the immediate requirements of the expanding sectors. More workers than average can be moving into new sectors. Some of these job seekers may not be immediately viable candidates for the available jobs and may exert little downward pressure on wages.

There can be mismatch unemployment because the skills and locations of job seekers can be poorly matched with the locations of vacancies. Some local labour markets will have more workers than jobs. Others will have shortages. Job finding can depend on the rate at which the unemployed can retrain or move to locations with unfilled jobs, the rate at which jobs open in different locations and the rate at which workers vacate jobs in places with ready replacements (Shimer 2007).

A New Zealand candidate for frequent sectoral shifts in labour demand is terms of trade shocks. Grimes (2006) found that half the variance in GDP growth rate over a 45-year period is explained by the level and volatility of the terms of trade. He found that the terms of trade have been high and remarkably stable since the early 1990s, and since the early 1990s, New Zealand has also experienced an unusually long period with high GDP growth and low GDP volatility.

Responding to aggregate versus sectoral shocks

Recessions mix cyclical and structural changes in labour demand. The aggregate demand and sectoral shift explanations have different implications for the role of monetary and fiscal policy in moderating cyclical unemployment fluctuations.

Cyclical unemployment is a reversible response to lulls in aggregate demand. At the start of a recession, there is a general decline in demand, with few industries creating jobs to replace those that are lost. As a recession ends, the unemployed are recalled by old employers or find new jobs in those industries as demand renews. Monetary and fiscal policy can aim to smooth these temporary job losses.

Job losses from structural changes in employment and technology are permanent. The sectoral location of jobs has changed. Workers must switch to new industries, sectors and locations or learn new skills. A role for public policy is to facilitate this process of reallocation to new jobs and retraining.

Much of the higher unemployment during the 1970s stagflation could have been due to a burst in sectoral shifts in labour demand. The 1973 and 1979 oil price shocks are common examples of real shocks that required lasting changes in the sectoral distribution of consumer demand, production and employment. The more energy-intensive industries had to adapt to the suddenly much higher oil prices.

Adding to this 1970s global restructuring in labour demand was the widespread introduction and adaptation of computer technologies. Bessen (2003) and Samaniego (2006) link the 1970s productivity slowdown to the widespread adoption of information technology.

Major economy-wide reorganisations were required because of the incompatibility of substantial accumulations of plant level expertise with many existing technologies with the incoming technologies. A major new technology can initially reduce measured productivity because of plant-level learning costs, the obsolescence of old technologies and skills, the time and resources diverted to develop and introduce the many complimentary innovations that implement a major new technology and the reallocation of labour to new industries.

These technological upheavals of a grand scale can cause a temporary spike in the natural rate of unemployment. Bessen (2003) estimated that, from 1974 to 1983, annual technology adoption costs spiked from 3% to 7% of output, explaining most of the 1970s productivity slowdown. It was decades later before the initially contractionary effects of major new technologies were well understood.

Summary

There is no reason to believe that the distribution of employment across sectors and industries will change at an even pace through time. If there are an above average number of sectoral shifts in labour demand, such as in the 1970s, there can be a significant increase in the natural unemployment rate while workers find new jobs, retrain and relocate. An above average number of sectoral shifts in labour demand during the current recession could delay the recovery. These sectoral shifts are difficult to forecast.

Marginal tax rate of average earners in USA, UK, Australia and New Zealand since 2000

21 Aug 2015 Leave a comment

in applied price theory, business cycles, economic growth, economic history, labour economics, labour supply, macroeconomics, politics - Australia, politics - New Zealand, politics - USA, public economics Tags: Australia, British economy, productivity shocks, real business cycles, taxation and labour supply

Interesting to notice that in New Zealand and the USA after these increases in marginal tax rates on single taxpayers, their economies slowed down. What appears to have happened is a number of people reached the next income tax marginal tax rate threshold.

Source: OECD StatExtract.

Marginal tax rates of New Zealand average households since 2000

19 Aug 2015 Leave a comment

in economic growth, fiscal policy, labour economics, labour supply, macroeconomics, politics - Australia, politics - New Zealand Tags: Australia, lost decades, marriage and divorce, productivity shocks, real business cycles, taxation and labour supply

In 2000 in New Zealand, the marginal tax rates of single earners, married couples and dual income couples were 21%.

Sources: OECD StatExtract.and OECD Taxing Wages.

Net personal marginal income tax rates increased:

- to 51% for one earner couples with two children in 2001 and stayed up above 50% until 2014; and

- to 33% for single earners with no children in 2004 because income growth pushed them into the next tax rate bracket which then dropped down to 30% in 2011.

Sources: OECD StatExtract.and OECD Taxing Wages.

Net personal marginal income tax rates increased:

- to 33% in 2004 for two earner couples with the second earner earning 33% of average earnings and then increased to 53% in 2006 and stayed high thereafter;

- to 33% in 2004 for a two earner couple with the second earner earning 67% of average earnings and then increased further to 53% in 2006 and stayed high until 2014 when their marginal income tax rate dropped to 30%; and

Sources: OECD StatExtract.and OECD Taxing Wages.

These large increases in marginal tax rates on single earners and families coincided with a slowing of the economy in about 2005. The economy started to pick up again when there were tax cuts introduced by the incoming National Party Government. Is that more than a coincidence?

Sources: Computed from OECD StatExtract and The Conference Board. 2015. The Conference Board Total Economy Database™, May 2015, http://www.conference-board.org/data/economydatabase/.

A flat line in the above figure is growth at the trend growth rate of 1.9% of the USA in the 20th century. A rising line is above trend growth for that year while a falling lined is below trend rate in GDP per working age person.

In the lost decades of New Zealand growth between 1974 In 1992, New Zealand lost 34% against trend growth which was never recovered. There was about 13 years of sustained growth at about the trend rate or slightly above that between 1992 and 2005. The entire income gap between Australia and New Zealand open up during these lost decades of growth between 1974 and 1992.

Sources: Computed from OECD StatExtract and The Conference Board. 2015. The Conference Board Total Economy Database™, May 2015, http://www.conference-board.org/data/economydatabase/.

Australia grew pretty much in its trend rate of growth since the 1950s. The so-called resources boom is not visible such as showing up as above trend rate growth.

Recurrent business cycles without shocks – the role of lumpy investments

11 Aug 2015 Leave a comment

in business cycles, economic growth, Edward Prescott, entrepreneurship, financial economics, fiscal policy, industrial organisation, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Edward Prescott, mega sports events, mega-projects, Mexico, Norway, prosperity and depression, R&D, real business cycles, Richard Rogerson, Robert Barro, technology diffusion lags

Think it is time for a re-post of @LHSummers' brilliant, brilliant paper on RBC from 1986. minneapolisfed.org/research/qr/qr… http://t.co/S7tGIjEebI—

Simon H (@simonhinrichsen) August 10, 2015

The brilliant monetary economist Scott Freeman was one of the 1st to show the existence of real business cycles without the need of shocks to drive the ups and downs of the economy. He did this when taking time off from showing that much of the apparent correlation between the nominal and the real side of the economy is due to the endogenous response of money created by banks to fluctuations in real activity.

In 1999, Scott Freeman co-wrote Endogenous Cycles and Growth with Indivisible Technological Developments. The paper was about large, discrete technological improvements that required the accumulation of research or infrastructural investment over time before any benefits for realised in terms of increased output. With these lead-times for research or infrastructure investments, growth paths display cyclical patterns even in the absence of any shocks.

This lumpiness over time implied that a costly process such as research or construction must be completed on a large scale before the greatest part of a project’s benefits in output can be realized as Freeman and co. argue:

There are numerous examples of big research or infrastructural projects that are characterized by huge investments and relatively long development periods, where most of the benefits occur only after the project is complete.

Freeman and his co-authors gave as examples space research and satellite programs and major medical research. These are examples of prolonged and costly R & D whose benefits come primarily at the conclusion of the project.

Lags in the development of a new drug between the commencement of the R&D project and any revenues received is routinely now more than a decade. The Human Genome Project seems to be going on without end with few initial benefits.

Infrastructural examples given by Freeman and his co-authors included the installation of telephone, the internet, transportation shipping canals, interregional highways, railroads, mass transit or electricity transmission projects. All of these projects with long lead times, once completed that may increase the productivity of many economic sectors in addition to increasing output in the area concerned. In many cases there are no benefits whatsoever of the project and to after it is completed many years in the future. Oil pipelines can take up to a decade to build.

The 1973 oil price crisis launched a research and development program into alternative sources of energy and alternative sources of oil and gas supply that has lasted to this day.

Classic further examples of long lead times are mega sports events such as the World Cup and Olympic Games. Years of planning, development and construction for any benefits or revenues are obtained.

What is important in terms of the random shocks that drive the business cycle as championed by Ed Prescott is there are a range of sectors within the economy where there are long lead times before the investment leads to any outputs. Not surprisingly the first article in the real business cycle literature included in its title “time to build“.

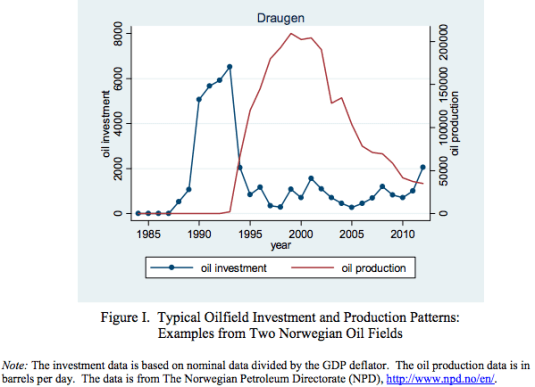

Rabah Arezki, Valerie Ramey, and Liugang Sheng in “News Shocks in Open Economies: Evidence from Giant Oil Discoveries” explore a related theme of real business cycles without shocks. In particular, they investigate news of productivity enhancements. They look at what happens to economies that discover oil. An oil discovery is a well identified “news shock.”

An oil discovery is well publicised and creates an incentive to invest in oil drilling. More importantly, there is news of greater income in the future but no change in current labour productivity or technological opportunities.

Rabah,Valerie, and Liugang found that after big oil discoveries, during the period of investment, the newly rich oil country borrows from abroad to build oil wells, oil pipelines and associated port infrastructure, obviously, but also borrows to finance higher consumption now. Consumption goes up and stays up in permanent income hypothesis fashion.

Interestingly, employment declines because of the wealth effect from the future income but there is no higher productivity of labour to encourage more work today. Investment rises soon after the news of the oil discovery arrives, while GDP does not increase for 5 years or more.

This is consistent with experience in the oil-rich Arab countries where there was increased consumption of leisure in anticipation of high future income is based on oil.

The same happened in Norway where massive investment was funded by foreign borrowing that led to annual current account deficits of up to 15% of GDP. Domestic savings fell away because Norwegians anticipated higher future incomes and started spending some of it now as predicted by the permanent income hypothesis. Norway now has a huge sovereign wealth fund able to fund a large part of its demographic burden from an ageing society.

After Mexico’s discovery of oil in the early 1970s, investment was high in oil and related industries. Consumption—by households and government—rose because of the increase in prospective real income. Since real GDP was not yet high, Mexico borrowed to pay for both the oil investment and the higher current consumption. Mexico’s foreign debt increased from $3.5 billion or 9% of GDP in 1971 to $61 billion or 26% of GDP in 1981. This boom in consumption and investment occurred without any productivity shock. All that was required was the ability to borrow.

Once the oil comes on line, the economy concern exports oil and pays back debt. This is when GDP including oil production finally rises a good five years and often more after the oil discovery. Consumption continues for its previous high rates while investment falls as the oil wells and pipelines have been built.

As with Scott Freeman, the long lead times not only can lead to large swings in investment, lumpy investments can also lead to increases in consumption, savings and employment without any productivity shocks.

Keynesian macroeconomics postulated that the economy slips into recessions for all sorts of reasons such as shifts and turns in the animal spirits and a loss of consumer confidence leading to a fall in autonomous investment and autonomous consumption. A collapse in autonomous investment and autonomous consumption is the Keynesian explanation for the great depression.

Both Keynesian macroeconomics and real business cycle theories at least at the outset couldn’t explain why there were recessions. Both attributed to them to causes they were yet to explain.

Keynesian macroeconomics could not explain what drove the waves of optimism and pessimism that either sharply increased or reduced investment. At bottom, Keynesian macroeconomics makes an unjustified assumption that technological progress unfolds at a relatively smooth rate and it attributes volatility in the economy to fluctuations in investment unrelated to trends in productivity.

The key inside of Keynesian macroeconomics was that inflation and unemployment were inversely correlated, so as one went up, the other went down as Milton Friedman explains.

Marvellously simple. A key that apparently unlocks the mystery of long-continued unemployment: inadequate autonomous spending or too low a propensity to consume. Increase either, or both, being careful simply not to go too far, and full employment could be attained.

What a wonderful prescription: for consumers, spend more out of your income, and your income will rise; for governments, spend more, and aggregate income will rise by a multiple of your additional spending; tax less, and consumers will spend more with the same result.

Though Keynes himself, and even more, his disciples, produced much more sophisticated and subtle versions of the theory, this simple version contains the essence of its great appeal to non-economists and especially governments.

A well-functioning economy should have no business cycles – no bouts of high inflation or persistent unemployment as Richard Rogerson explained:

So if there are cycles, that’s an indication of a malfunctioning economy. That idea permeated thinking for many years and was deeply ingrained. In effect, if an economy is in recession, someone should fix it.

The Keynesians only retreated as their empirical predictions were thoroughly discredited in the 1970s stagflation. Ad hoc auxiliary hypotheses were included about the supply-side in the Keynesian paradigm to prop up the old-time religion, not find new paths as Robert Barro put it:

At least Prescott and other real business cycle theorists accepted that they must eventually unpack productivity drops and name causes that can be explored further to be found persuasive or perhaps wanting. They argued that periods of temporarily low output growth need not be market failures, but could follow from temporarily slow improvements in production technologies.

As research progressed, real business cycles were viewed as recurrent fluctuations in an economy’s incomes, products, and factor inputs—especially labour—due to changes in technology, tax rates and government spending, tastes, government regulation, terms of trade, and energy prices.

Scott Freeman took this research further. He, his colleagues and his progeny showed that real business cycles can occur without any productivity rises and falls whatsoever. All that was needed was the ability to borrow and invest across time to finance lumpy investments. These lumpy investments can be anything from oil wells, dams to new drugs, anywhere involving time to build and capital accumulation:

HT: The Grumpy Economist: Arezki, Ramey, and Sheng on news shocks.

Growth accounting for the USA in the 1930s

05 Jun 2015 Leave a comment

in business cycles, economic growth, economic history, great depression, macroeconomics Tags: great depression, growth accounting, real business cycles

Notice how productivity recovers but hours worked per working age adults does not.

via The Current Financial Crisis in Spain: What Should We Learn from the ….

The impact of drought on the 1998 mild New Zealand recession

31 Mar 2015 Leave a comment

in business cycles, economic growth, macroeconomics, politics - New Zealand Tags: 1998 recession, drought, real business cycles

Reserve Bank of New Zealand has these conclusions about the contribution of drought to the business cycle in the late 1990s in New Zealand and in particular the mild 1998 recession:

a back-of-the-envelope estimate of the impact of the drought-induced fall in supply would suggest a contribution from the agricultural sector to production GDP for the March quarter of 1998 of around -0.4 percentage points out of the total 1 per cent fall in production GDP. In the June quarter of 1998, the contribution from these sectors was close to zero.

Figure 27:

In 1998, agricultural and hunting industry contributed per cent of real GDP. . That included the production of livestock, wool, dairy, horticulture, and crops, as well as the provision of agricultural contracting services and hunting. In the same year, the primary food manufacturing industry contributed 3 per cent of GDP. This category covers the processing of meat and dairy products for export and local markets.

Real business cycles, the declining clarity of information and learning by waiting

22 Dec 2014 Leave a comment

in business cycles, entrepreneurship, job search and matching, macroeconomics Tags: real business cycles

Willems and van Wijnbergen (2013) identified reduced clarity in information about business cycle fluctuations as a factor that is the lengthening the lag in the response of employment to output changes in recent US recessions.

Willems and van Wijnbergen (2013) – ungated – found that the trough in employment in the 1991 and 2001 recessions was much later than the troughs for earlier US recessions.

- There was a stronger immediate reduction in employment in pre-1990 US recessions and a faster recovery, so the 1991 and 2001 recessions were initially job-preserving – the rate at which workers were laid off was less than in prior recessions.

- Employment in the 1991 and 2001 recessions continued to fall for another year after the trough in output.

- The job-preserving recessions in 1991 and 2001 were then followed by this delayed recovery in employment growth.

- There is a lengthening labour adjustment lag that slows the loss of jobs at the start of recessions and delays the renewal of recruitment at the end of recessions.

Willems and van Wijnbergen (2013) attributed this combination of job-preserving recessions and delayed employment recoveries in 1991 and 2001 to the interaction of rising labour adjustment costs and a reduction in the clarity of entrepreneurial information about the business cycle.

The rising labour adjustment costs arose from the capital losses to employers of laying off employees who are increasingly rich in firm-specific human capital. The risks of laying off and investing precipitously have increased in recent decades because output growth subsequent to the great moderation in real output growth volatility is less predictable.

The US economy experienced a 50% reduction in volatility for many leading macroeconomic variables as well as low inflation since the early to mid-1980s. Similar declines in the real volatility and inflation rates occurred at about the same time in other industrial countries.

Prior to the mid-1980s, US real output growth was more variable, but this variation was more predictable. Frequent recessions were soon followed by recoveries. Since the early to mid-1980s in the US, major variations in real GDP growth have come increasingly as genuine surprises – 1983–2007 was one long boom punctuated by two mild recessions in 1991 and 2001.

The delay in the official dating of the peaks and troughs in business cycles in the US has increased from an average of 7½ months before 1990 to about 15 months in the post-1990 period (Willems and van Wijnbergen 2013).

With recessions more of a surprise – and the scope and depth of the panic of 2008 is an example of such a surprise in New Zealand and abroad – the value of waiting for better market information has increased.

Less certain information makes it more profitable than before for entrepreneurs to invest in waiting before laying off increasingly human capital-rich employees, making new investments and undertaking fresh recruitment. The impact of the business cycle on employment will be more muted.

Modern recessions can be initially job-preserving – layoffs are postponed for longer because the rising cost of laying off experienced labour is higher and because of the increased value of waiting to see. Recoveries in employment can be more sluggish as investors wait to be sure about the latest trends. These employers can use the employees they hoarded in larger numbers in the downswing to fill orders in the early days of the upswing in business:

We have presented evidence that the lag with which labour input reacts to structural economic shocks went up in the 1980s, thereby bringing jobless recoveries and recessions that were relatively job preserving to the US economy.

Using a real option model, this lagged response is shown to be optimal in a setting where labour input is costly to adjust and where employers are uncertain about the persistence of shocks that drive the business cycle

The role of news in real business cycles

18 Dec 2014 Leave a comment

in business cycles, economic growth, entrepreneurship, job search and matching, macroeconomics Tags: real business cycles

Revisions in investor beliefs about productivity prospects can partly account for business expansions and contractions. If favourable news about future technological opportunities can seed a boom today in consumption and investment before the actual technological improvement arrives and is realised, news that future productivity growth may not be as good as was previously expected can induce a recession without any actual change in productivity ever occurring.

Investors build in anticipation, starting new projects and recruiting more staff. Their forecasts can turn out to be too optimistic. When entrepreneurial expectations of future productivity are revised, investment demand can fall because of an excess in capital accumulation – recent investments were made under more optimistic beliefs about productivity (Beaudry and Portier 2004).

Investment demand must be muted for a time until the excess capital accumulation is brought into use, refitted or scraped. There also will be layoffs and a lull in recruitment. Job search strategies must also change as job seekers redirect their careers in light of the news about their revised prospects in different firms, industries and competing occupations.

The optimism and pessimism of investors are rational profit-seeking responses to new entrepreneurial knowledge. Profit expectations reflect consumer preferences, resource constraints and technological factors as they exist and are forecast to change and actual and forecasted opportunities and constraints in the investment sector. Entrepreneurs are dynamic risk takers who profit from anticipating shifts in consumer demand, input costs and technology.

Recessions and booms can arise due to the challenges facing entrepreneurs in forecasting the uncertain and ever-changing future demand for new capital that is implied by their forecasts of consumer demand and technological opportunities as Beaudry and Portier (2004) explain:

The view that recession and booms may arise as the result of investment swings generated by agents’ difficulties to properly forecast the economy’s need in terms of capital has a long tradition in economics.

For example, this difficulty was seen by Pigou as being an inherent feature of any economy with technological progress.

As emphasized in Pigou (1926), when agents are optimistic about the future and decide to build up capital in expectation of future demand then, in the case where their expectations are not met, there will be a period of retrenched investment which is likely to cause a recession.

Revisions in entrepreneurial beliefs and investment plans can be required when new information is uncovered (Beaudry and Portier 2004; Sill 2009). There can be lulls in investment demand following these revisions to entrepreneurial forecasts leading to recessions. As Pigou noted in 1927:

The varying expectations of business men … constitute the immediate cause and direct causes or antecedents of industrial fluctuations

Recent Comments