Skewed state? Spending on health & old age due to rise to 43%, education down to 13%. RF 2 update following #AS2015 pic.twitter.com/Xrnz8vp02I

— Resolution Foundation (@resfoundation) November 24, 2015

Where are British taxes spent?

26 Nov 2015 1 Comment

in budget deficits, defence economics, economics of education, fiscal policy, health economics, labour supply Tags: ageing society, British economy, British politics, demographic crisis

The dangerous left-wing bias of economists strikes again

21 Sep 2015 2 Comments

in applied price theory, budget deficits, business cycles, economics of regulation, history of economic thought, occupational choice, politics - USA

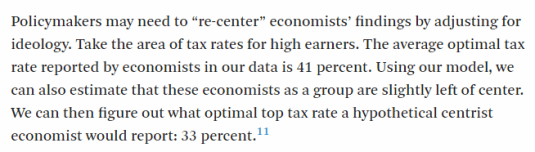

The left-wing bias of economists must be taken into account in public policy-making. Any suggestions to regulate the economy, spend our way out of a recession, increase the top tax rate and so on must be discounted for that well-known but little publicised political bias.

Source: Economists Aren’t As Nonpartisan As We Think | FiveThirtyEight

As is not well-known enough, Cardiff and Klein (2005) used voter registration data to rank disciplines at Californian Ivy League universities by Democrat to Republican ratios. Economics is the most conservative social science, with a Democrat to Republican ratio of a mere 2.8 to 1. This can be contrasted with sociology (44 to 1), political science (6.5 to 1) and anthropology (10.5 to 1). 40% of Americans are Democrats, 32% are independents with the balance Republicans.

Zubin Jelveh, Bruce Kogut, and Suresh Naidu confirmed that bias: that the typical economist is a moderate Democrat. They found a 60–40 liberal conservative bias

Jelveh, Kogut, and Naidu also reminded, as many have before them that economics is the most politically diverse of academic professions. Sociology is a notorious left-wing echo chamber as an example. Their most likely view of Jeremy Corbyn is he is a bit of a Tory. Oddly enough, sociologists are the first to point the finger at economists for political bias.

Jelveh, Kogut, and Naidu correlated political donations of more than $200 in the Federal Elections Commission database with the language used in 18,000 journal articles back to the 1970s.

More interestingly, they correlated political bias with the estimates of quantitative effects such as the top tax rate and its impact on labour supply and investment:

We found a (significant) correlation when we compared the ideologies of authors with the numerical results in their papers. That means that a left-leaning economist is more likely to report numerical results aligned with liberal ideology (and the same is true for right-leaning economists and conservative ideology)… liberals think the fiscal multiplier is high, meaning the government can improve economic growth by increasing spending, while conservatives believe the multiplier is close to zero or negative.

They are not suggesting a rigging of the results. Economists tend to sort into the fields that suit their ideologies:

It’s more likely that these correlations are driven by research areas and the methodologies employed by economists of differing political stripe. Economics involves both methodological and normative judgments, and it is difficult to imagine that any social science could completely erase correlations between these two… macroeconomists and financial economists are more right-leaning on average while labour economists tend to be left-leaning. Economists at business schools, no matter their specialty, lean conservative. Apparently, there is “political sorting” in the academic labour market.

Before you start writing out the indictment that economic policy and the global financial crisis is the product of a vast left-wing conspiracy within the economics profession you should remember the wise words of George Stigler.

Stigler argued that ideas about economic reform needed to wait for a market. He contended that economists exert a minor and scarcely detectable independent influence on the societies in which they live. As is well known, Stigler in the 1970s toasted Milton Friedman at a dinner in his honour by saying:

Milton, if you hadn’t been born, it wouldn’t have made any difference.

Stigler said that if Richard Cobden had spoken only Yiddish, and with a stammer, and Robert Peel had been a narrow, stupid man, England would have still have repealed the Corn Laws in the 1840s. England would still have moved towards free trade in grain as its agricultural classes declined and its manufacturing and commercial classes grew in the 1840s onwards because of the industrial revolution.

As Stigler noted, when their day comes, economists seem to be the leaders of public opinion. But when the views of economists are not so congenial to the current requirements of special interest groups, these economists are left to be the writers of letters to the editor in provincial newspapers. These days, they would run an angry blog.

Did Obama’s fiscal stimulus work?

30 Aug 2015 Leave a comment

in budget deficits, business cycles, fiscal policy, great recession, macroeconomics, politics - USA Tags: fiscal stimulus, obama

The ups and downs of the Greek economy

25 Aug 2015 1 Comment

in budget deficits, business cycles, currency unions, economic history, Euro crisis, fiscal policy, macroeconomics, Public Choice, rentseeking Tags: Eurosclerosis, Greece, sovereign debt crisis, sovereign defaults

@ObsoleteDogma @rodrikdani http://t.co/xKx43wjWHy—

David Andolfatto (@dandolfa) June 30, 2015

Explanation of the Greece Bailout in 90 Seconds

13 Aug 2015 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, fiscal policy, international economic law, international economics, International law, macroeconomics Tags: credible commitments, Eurosclerosis, game theory, Greece, sovereign bailouts, sovereign defaults

This time it is different: unemployment incidence by duration, USA, 1968 – 2014

08 Aug 2015 1 Comment

in budget deficits, great recession, job search and matching, labour economics, labour supply, macroeconomics, politics - USA, unemployment, welfare reform Tags: natural unemployment rate, taxation and labour supply, unemployment duration, unemployment insurance, unemployment rates, welfare state

The Great Recession was the first recession in the USA in a good 40 to 50 years where the composition of employment changed by much. Even the big recession at the beginning of the 1980s did not do much to the composition of unemployment by duration in the USA.

Source: OECD StatExtract.

Those unemployed for more than a year moved from barely double digits even in a bad recession prior to 2008 to coming on one-third of all unemployed. Likewise, those unemployed for less than a month halved from 40% to 20%. Something changed in the US labour market with the Great Recession and the long extensions of unemployment insurance from 26 weeks to 52 weeks and then 99 weeks.

More evidence of Ricardian equivalence and consumer foresight

05 Aug 2015 Leave a comment

in budget deficits, fiscal policy, public economics Tags: Ricardian equivalence

Did fiscal austerity in 2010 have credible academic support?

05 Aug 2015 1 Comment

![]()

#Greece austerity gauge. Greek government spending has fallen 20% since 2008. In UK and Italy it's up. #GreekCrisis http://t.co/WMQBxxVFqq—

RBS Economics (@RBS_Economics) July 07, 2015

One measure of the scale of austerity in Greece…and other advanced economies. http://t.co/PxCLagdd3L—

RBS Economics (@RBS_Economics) July 06, 2015

The employment level in #Greece is back to where it was in 1985. It's the equivalent of the UK losing 6 million jobs. http://t.co/AAWHMEFwfK—

RBS Economics (@RBS_Economics) July 06, 2015

Did the GFC catch modern macroeconomists by surprise?

03 Aug 2015 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, great recession, history of economic thought, law and economics, macroeconomics, monetary economics Tags: bank panics, bank runs, banking crises, currency crises, Thomas Sargent

@sjwrenlewis The stimulus package ignored what we have learned in the last 60 years of macroeconomic research

02 Aug 2015 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great recession, history of economic thought, macroeconomics, monetarism, monetary economics Tags: Brad Delong, fiscal multiplier, fiscal stimulus, Larry Summers, New Keynesian macroeconomics, Thomas Sargent

Is the socialist solution to the Greek economic crisis working?

25 Jul 2015 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, fiscal policy, global financial crisis (GFC), international economics, law and economics, macroeconomics, monetary economics, property rights Tags: capital controls, capital flight, Greece, labour exodus, sovereign defaults

For down and out Greeks, the U.K. is the promised land with jobs aplenty bloom.bg/1Lwcc55 http://t.co/XHHXxdTUiN—

Bloomberg Business (@business) July 24, 2015

A lot of countries borrowed a lot of money recently

18 Jul 2015 Leave a comment

in budget deficits, fiscal policy, global financial crisis (GFC), great recession, macroeconomics Tags: Greece, Italy, Japan, sovereign debt, sovereign default, Spain

Greece is unlikely to be the last sovereign debt restructuring of this cycle wsj.com/articles/greec… via @greg_ip http://t.co/YnvOuDurDL—

Nick Timiraos (@NickTimiraos) July 16, 2015

Maggie Thatcher on the Greek crisis

17 Jul 2015 Leave a comment

in applied welfare economics, budget deficits, comparative institutional analysis, constitutional political economy, currency unions, economic growth, economic history, economics of regulation, Euro crisis, fiscal policy, income redistribution, macroeconomics, Marxist economics, Public Choice, rentseeking Tags: Greece, growth of government, Margaret Thatcher, size of government

Why Greece joined the Euro

06 Jul 2015 Leave a comment

in applied price theory, applied welfare economics, budget deficits, business cycles, comparative institutional analysis, constitutional political economy, currency unions, economic growth, economic history, Euro crisis, fiscal policy, fisheries economics, global financial crisis (GFC), international economics, macroeconomics, Public Choice, rentseeking Tags: Euro sclerosis, Greece, insurance attacks, sovereign defaults, speculative attacks

The roots of Greece’s crisis are simple. Before Greece joined the Eurozone, investors treated it as a middle-income country with poor governance — which is to say, a credit risk.

After Greece joined the Eurozone, investors thought that Greece was no longer a credit risk — they figured, if push came to shove, other Eurozone members like Germany would bail Greece out. They were wrong.

Michael Dooley put forward a theory of speculative attacks on currencies as insurance attacks on currencies for emerging markets after the East Asian financial crisis:

First generation models of speculative attacks show that apparently random speculative attacks on policy regimes can be fully consistent with rational and well-informed speculative behaviour.

Unfortunately, models driven by a conflict between exchange rate policy and other macroeconomic objectives do not seem consistent with important empirical regularities surrounding recent crises in emerging markets. This has generated considerable interest in models that associate crises with self-fulfilling shifts in private expectations.

In this paper we develop a first generation model based on an alternative policy conflict. Credit constrained governments accumulate reserve assets in order to self-insure against shocks to national consumption. Governments also insure poorly regulated domestic financial markets.

Given this policy regime, a variety of internal and external shocks generate capital inflows to emerging markets followed by successful and anticipated speculative attacks.

We argue that a common external shock generated capital inflows to emerging markets in Asia and Latin America after 1989. Country specific factors determined the timing of speculative attacks. Lending policies of industrial country governments and international organizations account for contagion, that is, a bunching of attacks over time.

His model was not within the context of a currency union but his basic theory is correct.

There are speculative attacks on a currency or a bank run after foreign markets revises their estimates of the available central bank reserves and international lines of credit to bail out the banking systems and/or foreign debt.

Michael Dooley was dealing with the emerging economies of Southeast Asia and their official lines of credit that insure their foreign exchange liabilities and domestic banking system. Greece is about lines of credit for similar purposes to other European union member states.

via 12 charts and maps that explain the Greek crisis – Vox and The Most Important Graphs of 2011 – The Atlantic.

The reason why New Zealand should rule out helping Greece!

06 Jul 2015 Leave a comment

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), macroeconomics Tags: bank runs, banking panics, Eurosclerosis, Germany, Greece, sovereign defaults

Greece is a tiny part of the European economies so it doesn’t matter that much to the rest of the European Union what happens to Greece. The only people will notice the sovereign default of Greece once the breathless journalism has died down are Greeks themselves as they rebuild their banking and monetary system against a background of a government run by coffee shop Marxists.

Recent Comments