Source: Edward Prescott

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

22 Feb 2015 Leave a comment

in business cycles, economic growth, economic history, macroeconomics, politics - USA Tags: Edward Prescott

Source: Edward Prescott

02 Feb 2015 Leave a comment

in business cycles, fiscal policy, inflation targeting, macroeconomics, monetary economics Tags: new classical macroeconomics, Paul Samuelson, policy credibility, rational expectations, regime uncertainty, Stephen Williamson, time inconsistency, Tom Sargent

31 Jan 2015 Leave a comment

in budget deficits, business cycles, economic growth, Euro crisis, great depression, great recession, macroeconomics, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: deflation, fiscal policy, liquidity traps, monetary policy, stabilisation policy

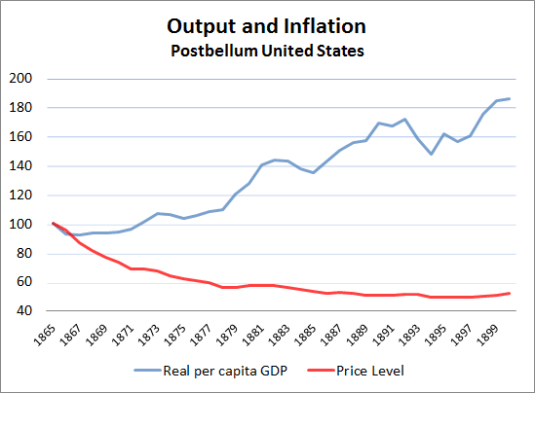

Deflation has a bad reputation. People blame deflation for causing the great depression in the 1930s. What worse reputation can you get as a self-respecting macroeconomic phenomena?

The inconvenient truth for this urban legend is empirical evidence of deflation leading to a depression is rather weak.

The most obvious is confounding evidence, is up until the great depression, deflation was commonplace. In the late 19th century, deflation coincided with strong growth, growth so strong that it was called the Industrial Revolution.

For deflation to be a depressing force, something must have happened in the lead up to the Great Depression to change the impact of deflation on economic growth.

Atkeson and Kehoe in the AER looked into the relationship between deflation and depressions and came up empty-handed.

Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

Deflation and Depression: Is There an Empirical Link?

Andrew Atkeson, and Patrick J. Kehoe, 2004.

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates. Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

View original post 1,842 more words

31 Jan 2015 8 Comments

30 Jan 2015 1 Comment

in business cycles, econometerics, economics of bureaucracy, economics of information, inflation targeting, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: lags on monetary policy, Levis Kochin, monetary policy

Monetarists blame fluctuations in inflation on excessively volatile growth in monetary aggregates. In 1982, Friedman defined monetarism in an essay on defining monetarism as follows:

Like many other monetarists, I have concluded that the most important thing is to keep monetary policy from doing harm.

We believe that a steady rate of monetary growth would promote economic stability and that a moderate rate of monetary growth would prevent inflation

The U.S. data supported this hypothesis about the volatility of monetary growth and inflationuntil 1982, but since 1983 monetary aggregates have been essentially uncorrelated with subsequent inflation in the U.S.

Levis Kochin pointed out in 1979 that a well designed monetary policy would lead to zero correlation between any measure of monetary policy and subsequent inflation. The reason for this is the correlation between any variable and a constant is zero.

If monetary growth is stable, say, a constant growth rate of 4% per year, as advocated by Milton Friedman, monetary growth will have no correlations with any variable:

Poole (1993, 1994) and Tanner (1993) also argue that one predictable consequence of optimal monetary policy is that the correlation between monetary policy instruments and policy goals will be driven to zero.

Poole further contends that it is obvious to any careful reader of Theil (1964) that optimally variable policy will give rise to a zero correlation between policy and goal variable…

In 1966 Alan Walters, a U.K. monetarist, observed:

If the [monetary] authority was perfectly successful then we should observe variations in the rate of change of the stock of money but not variations in the rate of change of income… [a]ssuming that the authority’s objective is to stabilize the growth of income.

Milton Friedman in 2003, wrote about how the Fed acquired a good thermostat:

The contrast between the periods before and after the middle of the 1980s is remarkable.

Before, it is like a chart of the temperature in a room without a thermostat in a location with very variable climate; after, it is like the temperature in the same room but with a reasonably good though not perfect thermostat, and one that is set to a gradually declining temperature.

Sometime around 1985, the Fed appears to have acquired the thermostat that it had been seeking the whole of its life…

Prior to the 1980s, the Fed got into trouble because it generated wide fluctuations in monetary growth per unit of output. Far from promoting price stability, it was itself a major source of instability as Chart 1 illustrates.

Yet since the mid ’80s, it has managed to control the money supply in such a way as to offset changes not only in output but also in velocity.

Nick Rowe explained the difficulty of causation and correlation under different policy regimes and Milton Friedman’s thermostat superbly as an econometric problem Nick Rowe:

If a house has a good thermostat, we should observe a strong negative correlation between the amount of oil burned in the furnace (M), and the outside temperature (V).

But we should observe no correlation between the amount of oil burned in the furnace (M) and the inside temperature (P). And we should observe no correlation between the outside temperature (V) and the inside temperature (P).

An econometrician, observing the data, concludes that the amount of oil burned had no effect on the inside temperature. Neither did the outside temperature. The only effect of burning oil seemed to be that it reduced the outside temperature. An increase in M will cause a decline in V, and have no effect on P.

A second econometrician, observing the same data, concludes that causality runs in the opposite direction. The only effect of an increase in outside temperature is to reduce the amount of oil burned. An increase in V will cause a decline in M, and have no effect on P.

But both agree that M and V are irrelevant for P. They switch off the furnace, and stop wasting their money on oil.

Subsequent work of Levis Kochin showed that if the effects of fluctuations in monetary aggregates were not precisely known then the optimal policy would produce negative correlations between monetary aggregates and inflation:

The negative correlation results from coefficient uncertainty because the less certain we are about the size of a multiplier, the more cautious we should be in the application of the associated policy instrument.

Therefore, although optimal policy leads to lack of correlation between the goal and control variables if the coefficient is known, it will lead to a negative relationship if there is coefficient uncertainty. The higher the uncertainty, the more cautious will be the optimal policy response. Also, if the control variable can’t be controlled perfectly then the correlation between the goal and the control variable becomes positive i.e., the control errors are random…

Uncertainty about the impact of a policy will stay the hand of any bureaucrat , much less a central banker, as Kochin and his co-author explain:

Uncertainty should lead to less policy action by the policymakers. The less policymakers are informed about the relevant parameters, the less activist the policy should be. With poor information about the effects of policy, very active policy runs a higher danger of introducing unnecessary fluctuations in the economy.

26 Jan 2015 Leave a comment

in business cycles, economics of information, history of economic thought, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Franco Modigliani, Keynes in macroeconomics, monetary policy, stabilisation policy, The fatal conceit, The pretence to knowledge

26 Jan 2015 Leave a comment

in business cycles, economic growth, great recession, macroeconomics, politics - USA Tags: great recession, Jagadeesh Gokhale, prosperity and depression

24 Jan 2015 Leave a comment

in applied welfare economics, business cycles, comparative institutional analysis, development economics, economic growth, global financial crisis (GFC), great recession, growth disasters, growth miracles, inflation targeting, macroeconomics, monetarism, Robert E. Lucas Tags: Robert E. Lucas

24 Jan 2015 Leave a comment

in business cycles, fiscal policy, great depression, great recession, history of economic thought, macroeconomics, monetary economics, Robert E. Lucas Tags: Paul Samuelson, prosperity and depression, The fatal conceit, The pretence to knowledge

20 Jan 2015 Leave a comment

in business cycles, Euro crisis, global financial crisis (GFC), great recession, labour economics, macroeconomics, unemployment Tags: Euroland

via Economic Rebounds in U.S. and Euro Zone: Deceivingly Similar, Strikingly Different – Dallas Fed.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Economics, public policy, monetary policy, financial regulation, with a New Zealand perspective

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Restraining Government in America and Around the World

Recent Comments