Celebrating humanity's flourishing through the spread of capitalism and the rule of law

06 Feb 2015 Leave a comment

in applied welfare economics, economic growth, health economics, technological progress Tags: The Great Enrichment, The Great Escape, The Great Fact

05 Feb 2015 Leave a comment

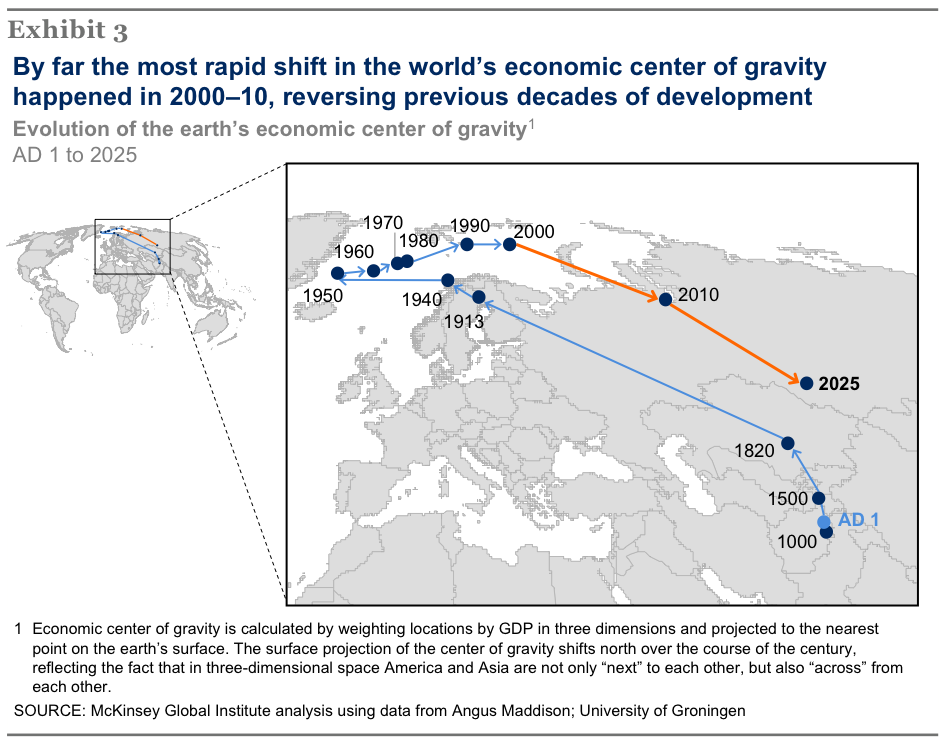

in economic growth, economic history, politics - New Zealand Tags: geography, global economic hubs

HT: https://twitter.com/tutor2u_econ/status/552013472247341056?s=09

31 Jan 2015 Leave a comment

in budget deficits, business cycles, economic growth, Euro crisis, great depression, great recession, macroeconomics, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: deflation, fiscal policy, liquidity traps, monetary policy, stabilisation policy

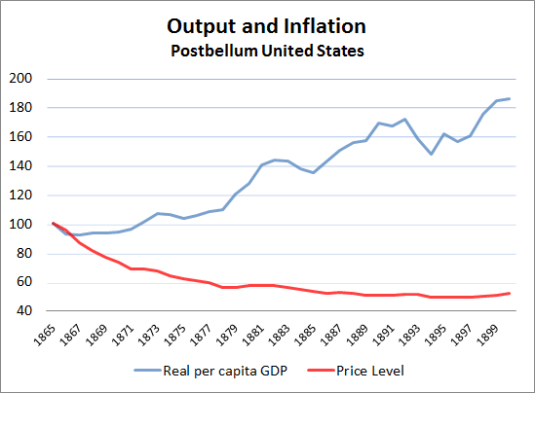

Deflation has a bad reputation. People blame deflation for causing the great depression in the 1930s. What worse reputation can you get as a self-respecting macroeconomic phenomena?

The inconvenient truth for this urban legend is empirical evidence of deflation leading to a depression is rather weak.

The most obvious is confounding evidence, is up until the great depression, deflation was commonplace. In the late 19th century, deflation coincided with strong growth, growth so strong that it was called the Industrial Revolution.

For deflation to be a depressing force, something must have happened in the lead up to the Great Depression to change the impact of deflation on economic growth.

Atkeson and Kehoe in the AER looked into the relationship between deflation and depressions and came up empty-handed.

Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

Deflation and Depression: Is There an Empirical Link?

Andrew Atkeson, and Patrick J. Kehoe, 2004.

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates. Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

View original post 1,842 more words

28 Jan 2015 Leave a comment

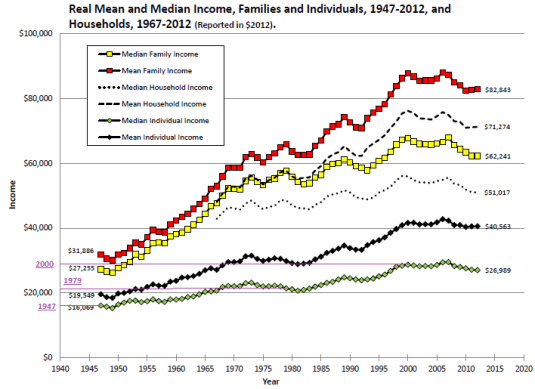

in applied welfare economics, economic growth, income redistribution, politics - USA, poverty and inequality Tags: middle class stagnation

27 Jan 2015 Leave a comment

in budget deficits, currency unions, development economics, economic growth, economic history, Euro crisis, fiscal policy, global financial crisis (GFC), growth disasters, law and economics, macroeconomics, poverty and inequality Tags: currency unions, Euroland, Greece, optimal currency area, sovereign default

26 Jan 2015 Leave a comment

in business cycles, economic growth, great recession, macroeconomics, politics - USA Tags: great recession, Jagadeesh Gokhale, prosperity and depression

26 Jan 2015 Leave a comment

24 Jan 2015 Leave a comment

in applied welfare economics, business cycles, comparative institutional analysis, development economics, economic growth, global financial crisis (GFC), great recession, growth disasters, growth miracles, inflation targeting, macroeconomics, monetarism, Robert E. Lucas Tags: Robert E. Lucas

24 Jan 2015 Leave a comment

22 Jan 2015 Leave a comment

in economic growth, macroeconomics Tags: Edmund Phelps, Golden rule of savings, intergenerational equity, John Rawls, just savings

Why is the Left so keen to tax the rich of today, which reduces investment, but through this concerns about sustainable development, not tax the rich of the next generation by leaving them a smaller capital stock?

Rawls proposes a principle of just savings. Rawls suggests that each generation puts itself in the place of the next, and asks what it could reasonably expect to receive.

Currently living people have a justice-based reason to save for future people only if such saving is necessary for allowing future people to reach the sufficientarian threshold as specified. This is known as the accumulation stage.

Once just institutions are securely established — this is known as the steady-state stage — justice does not require people to save for future people. Rawls also holds that, in that second stage, people ought to leave their descendants at least the equivalent of what they received from the previous generation.

Edmund Phelps developed a Golden Rule in the 1960s that suggests that it is possible to save and invest too much. Phelps also generated the result that the savings rate can be too high:

The basic significance of the golden rule is as a warning against national policies of over-saving or counterproductive austerity.

20 Jan 2015 Leave a comment

in applied price theory, applied welfare economics, economic growth, economic history, income redistribution, macroeconomics, Public Choice, public economics, rentseeking Tags: Leftover Left, Thomas Piketty

17 Jan 2015 Leave a comment

in economic growth, Gary Becker, human capital, job search and matching, labour economics, occupational choice Tags: human capital externalities

While there is a vast literature documenting the large private returns from education and on-the-job human capital (Card 1999; Rubenstein and Weiss 2007; Almeida and Carneiro 2008), evidence of human capital spillovers is limited. Many studies find little evidence of spillovers from education (Lange and Topel (2005), Ciccone and Peri (2006)). Studies even struggle to find small spillovers from another year in high school (Acemoglu and Angrist 2001). Differences in human capital also explain only a small part of cross-national differences in incomes per capita (Hsieh and Klenow 2010; Parente and Prescott 2000, 2005).

The R&D industries offer a case study of the likely size of skills spillovers from worker mobility from large firms. The mobility of technical personnel and the human capital embodied in them across R&D firms is a substantial source of knowledge transfer (Møen 2005). For there to be a spillover, the new employer must pay recruits less than the value added by the job experience and skills they bring to the fold.

A key advantage of studying the mobility of R&D workers for skills spillovers is these industries are populated with many spin-offs founded by the ex-employees of larger firms. R&D spin-offs tend to be larger on average that other new firms and initially employ more advanced, more experienced workers and more technical specialists than do other new firms (Andersson and Klepper 2013).

Capturing the value of skills spillovers from job-hopping is a major business opportunity. The efforts of entrepreneurs to create and enforce property rights over information and other resources as their value increases are central to the organisation of both markets and firms.

A litmus test for the capture of the value of skills spillover is whether wages adjust in line with evolving career opportunities. Becker (2007, p. 134) explains this process of market adaptation and entrepreneurship as follows:

Firms introducing innovations are alleged to be forced to share their knowledge with competitors through the bidding away of employees who are privy to their secrets. This may well be a common practice, but if employees benefit from access to saleable information about secrets, they would be willing to work more cheaply than otherwise.

Møen (2005), Magnani (2006) and Maliranta, Mohnen and Rouvinen (2009) found that employers capture much of the skills spillovers to others by paying R&D workers less early in their careers; later employers pay higher wages to reflect the valued added by the human capital that these R&D recruits bring.

Andersson, Freedman, Haltiwanger, Lane and Shaw (2009) found that software firms in markets with large returns from product breakthroughs pay higher starting salaries to attract star employees. Accounting and legal firms and sports teams also pay more to recruit and retain top performers (Wezel, Cattini and Pennings 2006; Campbell, Ganco, Franco and Agarwal 2012; Rosen 2001).

Employers balance skills and knowledge acquisition through recruitment with in-house development of skills and knowledge. Mason and Nohara (2010) did not find ‘any evidence’ that the external experience of scientists and engineers is any more valuable to firms than is their internal experience.

Firms will pay a wage that equalises the returns on skills acquisition through recruitment with the returns on investing in in-house training. This equalisation of the returns between internal and external sources of skills and knowledge is consistent with competition penalising firms that pay too much or too little for inputs and rewarding entrepreneurs for superior alertness to new opportunities.

The option value of founding or working for a spin-off is also captured in the wages of R&D workers (Kitch 1980; Pakes and Nitzan 1983). Central to a spin-off is carrying on with new ideas and prototypes that the leaving employees judged to be under-valued by the parent firm and they want to build on at their own entrepreneurial risk (Klepper and Sleeper 2005; Klepper 2007).

Large firms are known for incremental innovations while small firms pioneer product break-troughs whose prospects were not as well valued inside large hierarchies (Baumol 2002, 2005; Audretsch and Thurik 2003). Many R&D spin-offs continue with emerging ideas and products that their parents were in the process of abandoning (Hellmann 2007; Chatetterjee and Rossi-Hansberg 2012; Klepper and Thompson 2010). One reason is the developing idea does not fit in with the risk profile and skills of the parent so many spin-offs are friendly (Fallick, Fleischman, and Rebitzer 2006; Chen and Thompson 2011).

Founding or working for a spin-off or start-up is a real prospect. In many innovative industries, upwards of 20 percent of new entrants are intra-industry spinoffs; these firms outperform other new entrants and disproportionately populate the ranks of industry leaders (Klepper and Thompson 2010).

The evidence of large firms spawning more entrepreneurs among scientists and engineers is mixed. Large parent firm size reduces both the probability of leaving, and more so, the probability of leaving to found a spin-off (Andersson and Klepper 2013; Sørensen 2007; Sørensen and Philipps 2011). Spin-offs are less likely from large parents because more of the skills and experience accumulated within large firms is firm-specific human capital and is therefore less mobile into a spin-off.

Scientists and engineers who worked in small firms are ‘far more likely’ to found a spin-off than are their large firm counterparts, and their spin-offs are more likely to be a success (Elfenbein, Hamilton and Zenger 2010; Sørensen and Phillips 2011). Working in smaller firms allows spin-off minded employees to gain the balance and wide array of technical knowledge and management skills that are prized in entrepreneurship (Elfenbein, Hamilton and Zenger 2010; Lazear 2004, 2005).

Working in managerial hierarchies works against founding a spin-off. Tåg, Åstebro and Thompson (2013) found that conditional on size, employees in firms with more layers of management are less likely to enter entrepreneurship, self-employing or quit to go to another firm. They attributed this to the employees in firms with fewer management layers developing a broader range of skills; multiple layers of management offering more promotion opportunities; and skill mismatch is less problematic in more hierarchical firms because there are more chances to move. The higher pay and better career opportunities in larger firms reduces job quits, and with it, skills spillovers and spin-offs.

The wage adjustments for current skills and knowledge transfer opportunities to future employers, start-ups and spin-offs are large. New science graduates accept 20 per cent less in starting pay to work where they can publish more in their own names (Stern 2004).

Scientists and engineers working in R&D accept 20 per cent less pay than other scientists and engineers who work in technical and managerial occupations to secure this more interesting work (Dupuy and Smits 2010). Gibbs (2006) suggested that the U.S. Department of Defense is able to recruit and retain engineers and scientists on low pay because they offer work on some of the most advanced technical research in the world.

Employers who pay full value in wages, share options, learning and R&D opportunities in exchange for the labour and human capital of employees are not benefiting from a skills spillover.

The evidence just reviewed identifies market processes that minimise skills spillovers from large R&D firms to spin-offs. Large firms train their employees in skills that are more often firm-specific and adjust wages to account for the career opportunities that might arise from on-the-job training that is more mobile. The employees of larger firms have longer job tenures in part because their human capital is less mobile.

15 Jan 2015 Leave a comment

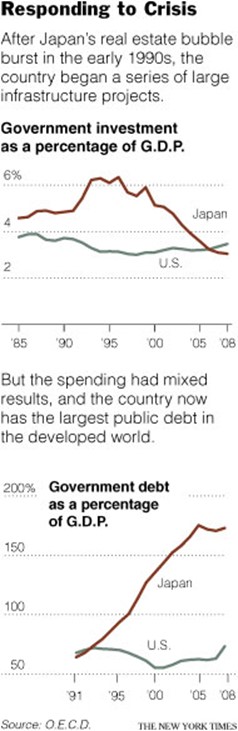

in economic growth, macroeconomics, politics - New Zealand, public economics Tags: fiscal stimulus, Japan, Lost Decade, Think Big

The low Japanese productivity growth throughout the 1990s could have been the result of subsidies to inefficient firms and declining industries both directly and through a banking system rolling over loans in arrears to insolvent firms.

This policy is known as zombie lending, and it lowered productivity because higher cost firms kept producing a greater share of Japanese output than would otherwise have been the case (Hayashi and Prescott 2003; Ahearne and Shinada 2005).

Japan’s economic policies have until recently kept insolvent banks operating, further encouraging zombie lending, which impeded the flow of capital to the more efficient firms.

The competitive process where zombies shed workers and lose market share was thwarted. The Japanese authorities subsidised insolvent banks and firms and provided credit to some firms and not to others (Prescott 2002; Hayashi and Prescott 2002; Caballero et al. 2005; Hoshi and Kashyap 2004).

The pervasiveness and long-term persistence of zombie lending as a shock to Japanese productivity growth cannot be understated. As Kashyap noted:

The government allowed even the worst banks to continue to attract financing and support their insolvent borrowers

…By keeping these unprofitable borrowers alive, banks allowed the zombies to distort competition throughout the rest of the economy.

Caballero et al. (2008) estimated that 30 per cent of all publicly traded Japanese manufacturing, construction, real estate, retail, wholesale, and service sector firms were on life support from banks in the early 2000s, and that most large Japanese banks only complied with capital standards because regulators were lax in their inspections.

The percentage of zombies hovered between 5 and 15 per cent up until 1993 and rose sharply over the mid-1990s to exceed 25 per cent for every year after 1994 (Caballero et al. 2008).

Figure 1: Prevalence of Firms Receiving Subsidized Loans in Japan

Source: Caballero et al. (2008) Zombie Lending and Depressed Restructuring in Japan. American Economic Review.

Zombie lending is a more serious problem for Japanese non-manufacturing firms than for manufacturing firms (Caballero et al. 2008). Small and medium size firms were also major beneficiaries of zombie lending.

Zombie lending also discourages new investments that increase Japanese productivity, encourages inefficient firms to avoid making the decisions necessary to raise their profitability, and impedes the solvent Japanese banks from finding good lending opportunities (Caballero et al. 2008; Sekine et al. 2003). As Kashyap noted:

Usually when an industry is hit by a bad shock, many firms exit… In Japan, firms never exited. Given that they never exited, it is not surprising that new firms weren’t created.

Under normal conditions, higher cost firms would go bankrupt and be replaced by new and better ideas and firms. Instead, firms that were more efficient than the zombie firms tended to exit industries because their demise does not require the banks to acknowledge large bad loans. This exit of the firms of intermediate efficiency rather than the exit of the least efficient firms dragged productivity down even further (Nishimura et al. 2005; Okana and Horioka 2008). New Zealand in the 1970s and in the early 1980s also had a range of policy measures that supported high-cost firms and declining industries.

When bankrupt firms can stay in business, they retain workers who otherwise would be willing to work for lower wages at a healthy firm and depress market prices for their products. Low prices and high wages reduce the profits that more productive firms can earn which discourages entry and investment.

The creation of new jobs is a measure of industry dynamism. In manufacturing, which suffered the least from the zombie problem, job creation hardly changed from the early 1990s to the late 1990s. In contrast, there was a large decline in job creation in the non-manufacturing sectors, particularly in construction (Caballero et al. 2008; Hoshi 2006; Caballero et al. 2008).

There was less restructuring of employment and market shares in favour of the more productive firms. The gap in productivity growth between the Japanese manufacturing and non-manufacturing sectors more than doubled over the 1990s (Caballero et al. 2008).

Japanese R&D spending has also slowed down significantly since the start of the 1990s (Comin forthcoming). The gap in the rate of computer adoption between Japan and USA also increased in the 1990s. The speed of diffusion of new technologies slowed to the point that South Körea has now surpassed Japan in the diffusion of computers and the Internet (Comin forthcoming).

Over the 1990s, there were ten massive fiscal packages to maintain employment and investment. Much of this additional Japanese government spending was on public works and other projects whose social payoffs have been queried by independent observers. The consumption tax was increased from 3 per cent to 5 per cent in 1997. There were two rounds of temporary tax cuts – for 2 years only.

Japan pursued economic policies in response to a recession that stifled total factor productivity by providing bad incentives to the private sector.

The unproductive firms depressed Japanese productivity because they competed for labour and capital that could have been used by the more productive firms. Zombie lending allowed many firms to stay in business long after the monetary policy changes that uncovered their unprofitable petered out. The diversion of resources to these insolvent firms prevented a productivity recovery. The lack of a productivity recovery depressed wages, incomes and consumer demand.

The zombie lending and fiscal packages compounded the 1990 monetary contraction into the highly persistent shocks that were required to be able to depress Japanese productivity growth for more than a decade.

More and more resources were tied up in high cost firms and in declining industries. This was rather than be reallocated to more productive uses by the normal market processes of relative price and wage changes, free entry and profit and loss. Kashyap argues that:

The experience in Japan definitely shows that providing subsidized credit to dying firms will be costly over time. Keeping an industry from restructuring only delays the day of reckoning and raises the cost substantially

…There are many examples besides Japan where people fail to recognize that it is dangerous to keep people attached to businesses that are fundamentally unprofitable

The massive Japanese government investments have echoes of the ‘Think Big’ energy investments in New Zealand in the late 1970s.

The productivity impact of ‘Think Big’ was suspect. In addition, state-owned enterprises offering a net return of zero to the Crown in the 1980s has Japanese parallels.

The propping up of high cost state owned and private firms in the 1970s and 1980s in New Zealand helped to depress productivity growth rates. State-owned enterprises offered a net return of about zero to the taxpayer, even as recently as last year in New Zealand.

More and more resources were tied up in New Zealand in the high cost firms and declining industries than be reallocated to more productive uses by the market processes of price and wage changes, free entry and profit and loss. The lack of productivity growth depressed wages, incomes and consumer demand in New Zealand.

The productivity based explanations for the slumps in New Zealand from 1974 to 1992 and in Japan from 1990 to 2003 have a number of common threads.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Economics, public policy, monetary policy, financial regulation, with a New Zealand perspective

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Restraining Government in America and Around the World

Recent Comments