77% more long-term unemployed people than before the crisis – We need them back in work! bit.ly/1JTTzYm #Jobs http://t.co/EFRGclFVms—

OECD Social (@OECD_Social) July 10, 2015

HT: IMF

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

13 Mar 2015 Leave a comment

in business cycles, economics of regulation, Euro crisis, job search and matching, labour economics, law and economics, macroeconomics, unemployment Tags: employment protection laws, Euroland, Eurosclerosis, labour market regulation

77% more long-term unemployed people than before the crisis – We need them back in work! bit.ly/1JTTzYm #Jobs http://t.co/EFRGclFVms—

OECD Social (@OECD_Social) July 10, 2015

HT: IMF

11 Mar 2015 Leave a comment

in business cycles, great recession, human capital, job search and matching, labour economics, labour supply, occupational choice, politics - USA, unemployment Tags: labour demographics

10 Mar 2015 Leave a comment

in applied welfare economics, economic growth, economic history, labour economics, liberalism, poverty and inequality, Rawls and Nozick Tags: class struggle, immiseration of the proletariat, Leftover Left, top 1%

How is the immiseration of the proletariat going to occur any time soon, and with it, the workers will rise up because they have nothing to lose but their chains, if the Australian top 1% doesn’t lift its game.

There is a serious lack of greed and expropriation of labour surplus by the top 1% in Australia. Their share of income has been falling for many decades and only increased in the last few years and then only slightly.

The top 1% is supposed to be grinding the working class down, and causing crisis after financial crisis but there’s hardly any of evidence of that in Australian income inequality data.

06 Mar 2015 1 Comment

in business cycles, macroeconomics Tags: conjecture and refutation, forecasting errors, Karl Popper, methodology of economics, Noah Smith, philosophy and social sciences, prophecy

Noah Smith is ranting today about how economists cannot forecast the timing of recession. He doesn’t use the most obvious argument.

That argument is if you are any good at picking the timing of the next recession, you wouldn’t go around talking and telling other people and publishing in the paper for all the world to hear.

You would keep quiet and trade in your own account, signing futures contracts and share options to take maximum advantage of seeing further than others. Show me the money, as Murray Rothbard explained:

Many studies, formal and informal, have been made of the record of forecasting by economists, and it has been consistently abysmal.

Forecasters often complain that they can do well enough as long as current trends continue; what they have difficulty in doing is catching changes in trend. But of course there is no trick in extrapolating current trends into the near future.

You don’t need sophisticated computer models for that; you can do it better and far more cheaply by using a ruler.

The real trick is precisely to forecast when and how trends will change, and forecasters have been notoriously bad at that. No economist forecast the depth of the 1981–82 depression, and none predicted the strength of the 1983 boom.

The next time you are swayed by the jargon or seeming expertise of the economic forecaster, ask yourself this question: If he can really predict the future so well, why is he wasting his time putting out newsletters or doing consulting when he himself could be making trillions of dollars in the stock and commodity markets?

Karl Popper argued that the job of the economist and other social scientists is not to be a prophet but to make conditional predictions such as if circumstances A apply, B will ensue. To do any more is to fall for the age-old allure of the prophet and his prophecies.

06 Mar 2015 Leave a comment

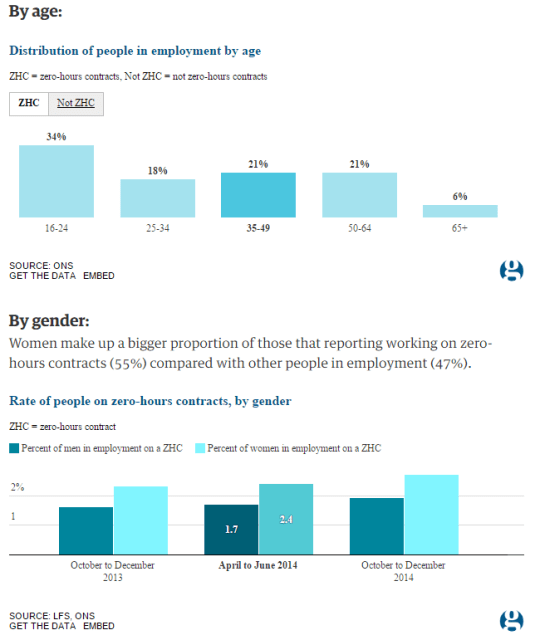

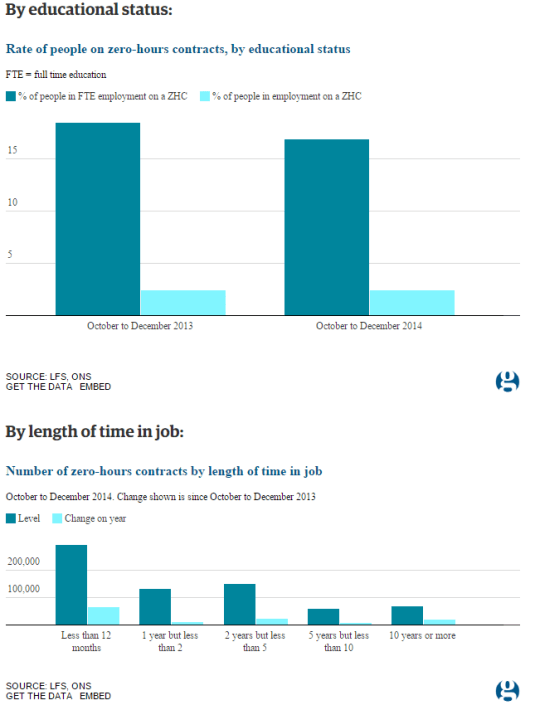

in job search and matching, labour economics, labour supply, politics - New Zealand Tags: zero hours contracts

Firstly, those on zero hours contracts are overwhelmingly younger people and more often women. Both groups value flexible working hours more than others. That’s why they make up the majority of workers on zero hours contracts.

Also not surprisingly, people on zero hours contracts also tend to be more often in full-time education. Another group that values flexibility in hours. Furthermore, many of those on zero hours contracts have only been in the current job for less than 12 months. Again, suggesting they come from groups that change jobs frequently, which means they can easily quit and find another job if they don’t like a zero-hours contract.

Via Zero-hours contracts in four charts | News | The Guardian

04 Mar 2015 7 Comments

in applied price theory, Austrian economics, entrepreneurship, F.A. Hayek, George Stigler, human capital, industrial organisation, job search and matching, labour economics, law and economics, Ludwig von Mises, politics - New Zealand, survivor principle Tags: Armen Alchian, employment law, employment protection laws, entrepreneurial alertness, France, Israel Kirzner, The fatal conceit, The pretence to knowledge

As discussed yesterday, if the Employment Court had its way, New Zealand case law under the Employment Relations Act regarding redundancies and layoffs would be as job destroying as those in France.

The Employment Court’s war against jobs goes back more than 20 years. To 1991 and G N Hale & Son Ltd v Wellington etc Caretakers etc IUW where the Court held that a redundancy to be justifiable under law it must be ‘unavoidable’, as in redundancies could only arise where the employer’s capacity for business survival was threatened.

The Court of Appeal slapped that down and affirm the right of the employer to manage his business in no uncertain terms:

…this Court must now make it clear that an employer is entitled to make his business more efficient, as for example by automation, abandonment of unprofitable activities, re-organisation or other cost-saving steps, no matter whether or not the business would otherwise go to the wall…

The personal grievance provisions … should not be treated as derogating from the rights of employers to make management decisions genuinely on such grounds. Nor could it be right for the Labour Court to substitute its own opinion as to the wisdom or the expediency of the employer’s decision.

When a dismissal is based on redundancy, it is the good faith of that basis and the fairness of the procedure followed that may fall to be examined on a complaint of unjustifiable dismissal

… the Court and the grievance committees cannot properly be concerned with an examination of the employer’s accounts except in so far as it bears on the true reason for dismissal.

The Employment Court could only inquire as to the genuineness of the employer’s decision and the procedures adopted. The Court could not substitute their views on management decisions. No second-guessing.

In Brake v Grace Team Accounting Ltd, the Employment Court found its way back into second-guessing employer’s decisions about how to manage their business. The figures used by the employer to decide that a redundancy was required were in error. The employer miscalculated.

The Employment Court had previously held in Rittson-Thomas T/A Totara Hills Farm v Hamish Davidson that the statutory test of what a fair and reasonable employer could have done in all the circumstances applies to the substantive reasoning for redundancies. Some enquiry into the employer’s substantive decision is required to establish that a hypothetical fair and reasonable employer could also make the same decision in all of the circumstances.

Subsequently in Brake v Grace Team Accounting Ltd, the Employment Court found that the actions by the employer were “not what a fair and reasonable employer would have done in all the circumstances” and “failed to discharge the burden of showing that the plaintiff’s dismissal for redundancy was justified”.

The Court found that the redundancy was “a genuine, but mistaken, dismissal”, but it still found that the dismissal was substantively unjustified. That is a major new development. Mistaken dismissals that are genuine are unlawful and grounds for compensation under the employment law.

The case was appealed where the issues were whether the correct test had been applied. The Court of Appeal, in a sad day for employers, job creation and the unemployed, found that the Employment Court was within its rights to do what it did and applied the statutory tests correctly:

GTA acted precipitously and did not exercise proper care in its evaluation of its business situation and it made its decision about Ms Brake’s redundancy on a false premise.

So it never turned its mind to what its proper business needs were but rather proceeded to evaluate its options based on incorrect information. We can see no error in the finding by the Employment Court that a fair and reasonable employer would not do this.

The test is now that fair and reasonable employers in New Zealand do not make mistakes. A much greater burden is now laid upon employers to show that not only that redundancies are justified, but they have made careful calculations and no mistakes.

No more seat of your pants entrepreneurship in New Zealand. No more entrepreneurial hunches – the essence of entrepreneurship is acting on hunches and other judgements that are incapable of being articulated to others and about which there is mighty disagreement in many cases. As Lavoie (1991) states:

…most acts of entrepreneurship are not like an isolated individual finding things on beaches; they require efforts of the creative imagination, skillful judgments of future costs and revenue possibilities, and an ability to read the significance of complex social situations.

The essence of entrepreneurship is your hunches are better than the next guy’s and you survive in competition by backing that hunch often to the consternation of the crowd. As Mises explains:

[Economics] also calls entrepreneurs those who are especially eager to profit from adjusting production to the expected changes in conditions, those who have more initiative, more venturesomeness, and a quicker eye than the crowd, the pushing and promoting pioneers of economic improvement…

The entrepreneurial idea that carries on and brings profits is precisely that idea which did not occur to the majority… The prize goes only to those dissenters who do not let themselves be misled by the errors accepted by the multitude

In many cases, those entrepreneurial hunches are sorted, sifted and selected on the basis of trial and error in the marketplace. Central to Hayek’s conception of the meaning of competition is it is a process of trial and error with many errors:

Although the result would, of course, within fairly wide margins be indeterminate, the market would still bring about a set of prices at which each commodity sold just cheap enough to outbid its potential close substitutes — and this in itself is no small thing when we consider the insurmountable difficulties of discovering even such a system of prices by any other method except that of trial and error in the market, with the individual participants gradually learning the relevant circumstances.

Remember Hayek’s conception of competition as a discovery procedure where prices and production emerge through the clash of entrepreneurial judgements and competitive rivalry:

…competition is important only because and insofar as its outcomes are unpredictable and on the whole different from those that anyone would have been able to consciously strive for; and that its salutary effects must manifest themselves by frustrating certain intentions and disappointing certain expectations

Errors are no longer permitted in the New Zealand labour market by the Employment Court. The Court has outlawed error in redundancy decisions.

This is despite the fact that the conception by Kirzner of the market process is that it is an error correction procedure without rival and a central role of entrepreneurial alertness is to correct errors in pricing and production:

It is important to notice the role played in this process of market discovery by pure entrepreneurial profit. Pure profit opportunities emerge continually as errors are made by market participants in a changing world. The inevitably fleeting character of these opportunities arises from the powerful market tendency for entrepreneurs to notice, exploit, and then eliminate these pure price differentials.

The paradox of pure profit opportunities is precisely that they are at the same time both continually emerging and yet continually disappearing. It is this incessant process of the creation and the destruction of opportunities for pure profit that makes up the discovery procedure of the market. It is this process that keeps entrepreneurs reasonably abreast of changes in consumer preferences, in available technologies, and in resource availabilities.

Rothbard made similar arguments about the centrality of discrepancies and error in entrepreneurship:

The capitalist-entrepreneur buys factors or factor services in the present; his product must be sold in the future. He is always on the alert, then, for discrepancies, for areas where he can earn more than the going rate of interest.

In Frank Knight’s conception of profit, there were temporary profits that arise from the correction of error:

In the theory of competition, all adjustments “tend” to be made correctly, through the correction of errors on the basis of experience, and pure profit accordingly tends to be temporary.

The Employment Court misunderstands the market process as a process of error correction. Those errors are identified through entrepreneurial alertness and trial and error. These errors are both of over-optimism and over-pessimism as Kirzner explains:

Errors of over-pessimism are those in which superior opportunities have been overlooked. They manifest themselves in the emergence of more than one price for a product which these resources can create. They generate pure profit opportunities which attract entrepreneurs who, by grasping them, correct these over-pessimistic errors.

The other kind of error, error due to over-optimism, has a different source and plays a different role in the entrepreneurial discovery process. Over-optimistic error occurs when a market participant expects to be able to complete a plan which cannot, in fact, be completed.

A considerable part of entrepreneurial alertness arises from the business opportunities created by sheer ignorance and pure error as Kirzner explains:

What distinguishes discovery (relevant to hitherto unknown profit opportunities) from successful search (relevant to the deliberate production of information which one knew one had lacked) is that the former (unlike the latter) involves that surprise which accompanies the realization that one had overlooked something in fact readily available. (“It was under my very nose!”)

The market process is a selection procedure where the more efficient survive for reasons that may be unknown to the entrepreneurs directly concerned as well as to observers and officious judges. Alchian pointed out the evolutionary struggle for survival in the face of market competition ensured that only the profit maximising firms survived:

The surviving firms may not know why they are successful, but they have survived and will keep surviving until overtaken by a better rival. All business needs to know is a practice is successful.

One method of organising production and supplying to the market will supplant another when it can supply at a lower price (Marshall 1920, Stigler 1958). Gary Becker (1962) argued that firms cannot survive for long in the market with inferior product and production methods regardless of what their motives are. They will not cover their costs.

The more efficient sized firms are the firm sizes that are currently expanding their market shares in the face of competition; the less efficient sized are those firms that are currently losing market share (Stigler 1958; Alchian 1950; Demsetz 1973, 1976). Business vitality and capacity for growth and innovation are only weakly related to cost conditions and often depends on many factors that are subtle and difficult to observe (Stigler 1958, 1987). The Employment Court pretends to know better than the outcome of the competitive struggle in the market for survival.

The Employment Court also believes employers have something akin to academic tenure. In 2010, the Court found that an employee’s redundancy was unjustified because the employer did not offer redeployment and there is no requirement that the right of the redeployment be written into the employment agreement (Wang v Hamilton Multicultural Services Trust). The particulars of this case were quite interesting:

In the case at hand, the Employment Court held that the employer was obliged to look for alternatives to making the employee redundant. Given that he would be able to perform the new finance manager position with some up-skilling, the employer should have offered him the position rather than simply inviting him to apply for it.

The notion that an employee through training can quickly increase their marginal productivity by 50% to fill a more senior role contradicts the modern labour economics of human capital. A 50% salary increase through a bit of training would imply extraordinary annual returns on other forms of on-the-job training and formal education as well as the training at hand in the Employment Court case.

I would very much like to be in the position where I can get a 50% salary increase after a bit of training. As I recall, I required about 5-10 years of on-the-job human capital acquisition before my starting salary as a graduate was 50% higher through promotion and transfers.

In summary, the Employment Court stands apart from the modern labour economics of human capital and job search and matching as well as the modern theory of entrepreneurial alertness, and the market as a discovery procedure and an error correction mechanism. The Employment Court has fallen for both the pretence to knowledge and the fatal conceit.

03 Mar 2015 Leave a comment

in economics of regulation, job search and matching, labour economics, law and economics, organisational economics, politics - New Zealand Tags: employment protection laws, France, The fatal conceit, vexatious litigation

If the Employment Court had its way, New Zealand case law under the Employment Relations Act regarding redundancies and layoffs would be as strict as those in France. As top employment lawyer Peter Cullen explained in the Dominion Post today:

Former Employment Court chief justice Tom Goddard said employees could not be made redundant unless the company would otherwise go to the wall.

The employer appealed.

The Court of Appeal said something quite different. Its view was that if a business could be run more efficiently without a particular position, then it was entitled to disestablish it.

The Court of Appeal made it plain that it would not critically examine the logic behind the employer disestablishing a role. If the reason behind the redundancy was genuine, that was all that really mattered. Of course a fair process and consultation ought to precede any decision, but the outcome nevertheless was that the position could go.

The Employment Court wanted the position to be the same as at that in France where layoffs are permissible only to avoid bankruptcy:

…firms still cannot lay off workers to improve competitiveness when the business is healthy; they can only make economic dismissals to preserve competitiveness when already in financial straits. In France, it ought to be legal to fix small problems before they become big.

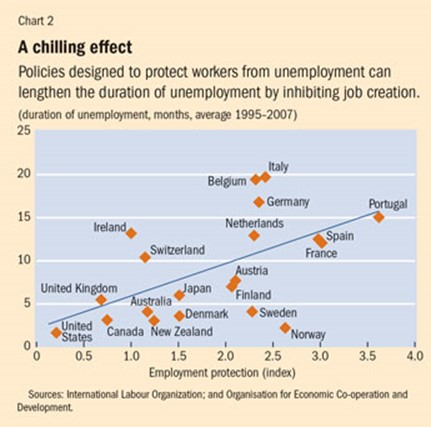

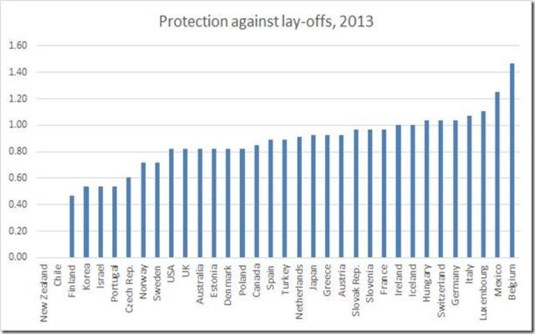

This French standard of regulation of layoffs and redundancies, if it had survived on appeal, would have come as a surprise to many, including the OECD who rates New Zealanders having no regulation of layoffs in its Index of Employment Protection.

Source: OECD employment protection index.

But you can’t keep an activist Employment Court down. It’s next tactic was salami tactics. Chipping away at the right of the employer to run its business and decide how large its labour force is. Peter Cullen again with the Employment Court pretending it can second-guess entrepreneurial judgements and arithmetic:

In the case between Grace Team Accounting and employee Judith Brake, the Employment Court found that the decision to make Brake’s position redundant was based upon mistaken arithmetic. The Court of Appeal held that Brake’s redundancy amounted to an unjustified dismissal.

Next cab off the rank was requiring employers to give preference to redundant employees pretty much no matter what. Peter Cullen again:

In the case of Neil Wang and his employer the Hamilton Multicultural Services Trust, the trust encouraged Wang to apply for another role within the organisation.

However, the Employment Court said the trust should have considered whether they should have simply offered Wang the position without having to go through an application process.

The court found that even though the other role was not the same, it required the same skills and minimal retraining and so the trust should have simply given Wang the role.

It is standard in the redundancies and restructurings I’ve been involved with for non-managerial employees to go through internal reassignment panels. Some didn’t make it and were laid off.

It’s common for the managerial vacancies to be advertised externally so that redundant managers must compete with external applicants so that the workplace can renew itself. Quite a few managers don’t make it through this process because of the external competition.

This clear preference for existing employees is a major reregulation of the labour market. Now, every redundant employee can engage in vexatious litigation and squeeze a few thousand dollars extra out of the employer by threatening to go to the Employment Court for a second opinion on the entrepreneurial judgements of the employer. To save managerial time as well is legal fees, it’s cheaper for most employers to pay the redundant employee off with a small settlement.

Anything that makes it more expensive to fire an employee makes it more expensive to hire an employee. This will reduce job creation in New Zealand now that the French standard applies:

…businesses remain obligated to assist laid-off employees in finding other jobs and in retraining them for their new positions – a distinctly French phenomenon. For businesses with more than 1,000 employees, this limbo period before dismissal can last from four to nine months.

03 Mar 2015 Leave a comment

in econometerics, economic growth, industrial organisation, politics - New Zealand Tags: capital mobility, Trans-Tasman income gap

Hall and Scobie (2005) attributed 70 percent of the labour productivity gap with Australia to New Zealand workers using less capital per worker than their Australian counterparts, rather than their using w3capital less efficiently. Figure 1 shows that the capital labour ratio is lower in New Zealand than in Australia and has been lower than Australia for several decades and is getting worse.

Figure 1: Capital intensity in New Zealand relative to Australia: 1978-2002

Source: Hall and Scobie 2005.

In 1978, New Zealand and Australian workers had about the same amount of capital per hour worked. By 2002, capital intensity in Australia was over 50 percent greater than in New Zealand. This lower rate of capital intensity is capital shallowness.

Capital should flow to countries with the highest risk adjusted rates of return. If workers in a country work with less capital than in other countries, the rate of return on providing them with more capital is higher than the global average return to capital. As Stigler (1963) said:

There is no more important proposition in economic theory than that, under competition, the rate of return on investment tends toward equality in all industries.

Entrepreneurs will seek to leave relatively unprofitable industries and enter relatively profitable industries, and with competition there will be neither public nor private barriers to these movements.

This mobility of capital is crucial to the efficiency and growth of the economy: in a world of unending change in types of products that consumers and businesses and governments desire, in methods of producing given products, and in the relative availabilities of various resources—in such a world the immobility of resources would lead to catastrophic inefficiency

Hall and Scobie (2005) acknowledged that lower capital intensities could be entirely a by-product of lower MFP. New Zealand had the third worst MFP growth performance since 1985, one quarter the OECD average (OECD 2009).

Rather than money being left on the table by persistent, known but unexploited entrepreneurial opportunities for pure profit by investing more in under-capitalised New Zealand and providing additional capital and equipment and more advanced technologies for New Zealanders to work with, investors have done the best they could the relative poor investment opportunities here.

Figure 2: Differences in capital intensity: the case of different production functions

Source: Hall and Scobie 2005.

A divergence in labour productivity levels between Australia and New Zealand emerged in the 1970s and 1980s. Kehoe and Ruhl (2003) attributed 96 percent of the fall in labour productivity in New Zealand between 1974 and 1992 to a fall in MFP. Changes in capital intensities played a minor role.

Aghion and Howitt (2007) found that three-quarters of the growth in output per worker in Australia and New Zealand between 1960 and 2000 was due to growth in MFP. New Zealand’s annual MFP growth of 0.45 percent between 1960 and 2000 was simply much lower than Australia’s 1.26 percent per year. Capital deepening was equally lower in New Zealand with 0.16 percent comparing to 0.41 percent in Australia.

Less would be invested in a country if the returns are lower because the capital is poorly employed. There might be a lack of complementary skills and education and, more often, policy distortions that lower MFP (Alfaro et al 2007; Caselli and Feyrer 2007; Lucas 1990).Investment in ICT capital is greatest in the USA because it is the global industrial leader and has very flexible markets. Investment in ICT in the EU is proportionately less because less flexible markets make ICT investments in the EU members less fruitful to investors.

To explore the relative role of lower MFP and the cost of capital in capital shallowness, Hall and Scobie (2005) used national accounts data to estimate the cost of capital and found that New Zealand faced a higher cost of capital than Australia, the USA and the OECD average since the early 1990s. Research that is more recent disputes these concerns about a higher cost of capital in New Zealand.

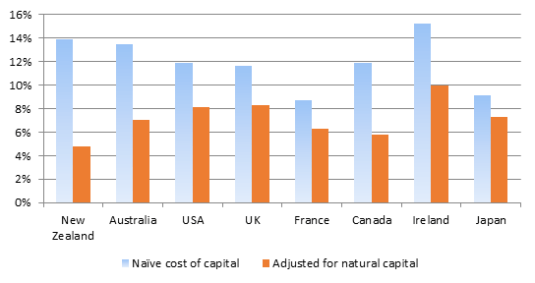

In Caselli and Feyrer’s (2007) revised cost of capital estimates, the cost of capital is significantly lower in New Zealand than in Australia and elsewhere in the OECD area such as the USA, Japan and UK – see Figure 3. Caselli and Feyrer (2007) correct for an overestimation of the cost of capital that is prevalent for countries such as New Zealand where the value of land and natural resources are high.

Figure 3: Caselli and Feyrer’s Estimates of the Cost of Capital, 1996

Source: Caselli and Feyrer (2007); Hsieh and Klenow (2011).

Notes: The measure of capital income used by Hall and Scobie (2005) to calculate the cost of capital includes payments to reproducible physical capital (equipment, machinery, ICT, buildings and other structures) as well as payments to natural capital (land and natural resources). Dividing the income that flows to all types of capital including land and natural resources by just the value of reproducible physical capital overestimates the cost of capital. Caselli and Feyrer (2007) used World Bank (2006) estimates of natural capital stocks in 1996 to estimate of income flows to reproducible physical capital. Their estimates excluded income flows to land and natural resources to estimate the cost of reproducible capital.

Caselli and Feyrer (2007) revised estimate in Figure 3 is for the cost of capital for investing in equipment, machinery, ICT, buildings and structures. When land and resources are included, shown in light blue as the naive cost of capital, the estimated cost of capital is one-half of percentage point higher in New Zealand than in Australia and two percent higher in New Zealand than the USA and UK in Figure 3. When land and natural resources are excluded, shown in red as the adjusted for natural capital estimate, the cost of capital is much lower in New Zealand than in Australia, the USA, Japan and UK – see Figure 3.

What Caselli and Feyrer (2007) show is the estimation of the cost of capital to New Zealand is fraught with statistical difficulties. A broader data set yields radically different results. That is the broader lesson.

At a minimum, safest thing to say, is there are no reliable estimates of the cost of capital in New Zealand. Depending on how you measure it, the cost of capital in New Zealand is either much higher or much lower than in the leading industrial countries such as the USA and UK. Such a broad range of estimates is no basis for public policy interventions.

When having to choose between arguing for a persistent, known but unexploited entrepreneurial opportunities for risk-free profit left on the table in New Zealand by foreign investors for decades, and measurement error in the case of one of the nastiest measurement jobs – measuring capital and natural resources – measurement error is more likely.

Capital is the most internationally mobile of factors of production. Entrepreneurs have every incentive to move it to new destinations with higher risk-adjusted rates of returns. Returns will not be exactly equal, but there will be a tendency for equalisation subject to these reservations listed by George Stigler in 1963:

The last of these reservations listed by George Stigler in 1963 about the statistical concepts used in compiling what data can be collected and the concepts relevant to the entrepreneurial decisions about the allocation of resources appear to be crucial to the debate about capital shallowness in New Zealand. They also echo Hayek’s great reservation in his 1974 lecture The Pretence to Knowledge about focusing on what can be measured rather than what is important in both economic analysis and public policy making:

We know: of course, with regard to the market and similar social structures, a great many facts which we cannot measure and on which indeed we have only some very imprecise and general information. And because the effects of these facts in any particular instance cannot be confirmed by quantitative evidence, they are simply disregarded by those sworn to admit only what they regard as scientific evidence: they thereupon happily proceed on the fiction that the factors which they can measure are the only ones that are relevant.

Hall and Scobie (2005) were careful scholars who noted that possibility that the apparent capital shallowness in New Zealand is merely the result of measurement error because of the problems of measuring land and natural. Caselli and Feyrer (2007) justify their caution and vindicated the view that the marginal product of capital is pretty much the same all round the world. As Caselli and Feyrer (2007) explain:

There is no prima facie support for the view that international credit frictions play a major role in preventing capital flows from rich to poor countries.

Lower capital ratios in these countries are instead attributable to lower endowments of complementary factors and lower efficiency, as well as to lower prices of output goods relative to capital. We also show that properly accounting for the share of income accruing to reproducible capital is critical to reach these conclusions.

There is various debates in policy circles in New Zealand about this lack of capital per worker and a higher cost of capital in New Zealand.

But that debate and any policy measures that were introduced as a result may be misplaced and all due to measurement error, or more correctly the grave difficulties of measuring both the capital stock and the cost of capital, both generally and in New Zealand course of its large bounty of natural resources. The data was always in doubt, so any policy interventions should be very cautious and incremental.

It would have been surprising to find that lower productivity in New Zealand was due to a lack of access to capital. There is growing evidence that capital intensities are not a major contributor to cross-national per capita income gaps.

There is a broad empirical consensus that capital intensity explains about 20 per cent of cross-country income differences; differences in human capital account for 10 to 30 per cent of cross-national differences with MFP accounting for the remaining 50 to 70 percent (Hsieh and Klenow 2011).

The New Zealand capital shallowness hypothesis is too marred in measurement shortcomings to rebut this broad empirical consensus about MFP differences between all other countries. For example, when reviewing the trans-Atlantic productivity and income gap, Edward Prescott said:

The capital factor is not an important factor in accounting for differences in incomes across the OECD countries… [It] contributes at most 8 percent to the differences in income between any of these countries.”

At the broader level, this blind alley about capital shallowness in New Zealand illustrates the pretence to knowledge. The politicians and bureaucrats pretended to know the cost of capital and the size of the capital stock in New Zealand and then work out what to do in response while doing more good than harm. This was despite serious reservations about the quality of data at hand.

This blind alley about the cost of capital and capital shallowness in New Zealand illustrates Josh Lerner’s point about distractions such as these and their many equivalents overseas reinforce the importance of the neglected art of setting the table– of fostering a favourable business environment. The neglected art of setting the table includes:

01 Mar 2015 Leave a comment

in applied welfare economics, economic growth, economics of regulation, monetarism, politics - Australia, politics - New Zealand, poverty and inequality Tags: economic reform, Margaret Thatcher, rent seeking, Rogernomics

There are plenty of critics of deregulation, albeit enough for them are smart enough to realise they cannot restore the lost monopolies and high marginal tax rates on the middle-class. They admit in their hearts that deregulation and other economic reforms worked as did inflation targeting.

The common force behind economic reform from 1980 onwards was the growing deadweight welfare losses of the pre-1980s status quo.The pressure for reform came from the rising burden that increases in taxes and regulation placed on economic growth as evidenced by the 1970s productivity slowdown and stagflation.

George Stigler argued that ideas about economic reform need to wait for a market. As Stigler noted, when their day comes, economists seem to be the leaders of public opinion. But when the views of economists are not so congenial to the current requirements of special interest groups, these economists are left to be the writers of letters to the editor in provincial newspapers and run angry blogs.

Post-1980 trends in taxes, spending, and regulation in New Zealand and abroad reflect demographic shifts, more efficient taxes, more efficient spending, a shift in the political influence from the taxed to the subsidised, shifts in political influence among taxed groups, and shifts in political influence among the subsidised groups (Becker and Mulligan 1998, 2003).

The common forces behind economic reform across the OECD area have subtle implications for the size of the reform dividend for New Zealand

Certainly, in New Zealand, the post-1984 economic reforms followed a good 10 years of economic stagnation and regular economic crises.

In the early 1980s, New Zealand’s economy was in trouble. The country had lost its guaranteed export market when Britain joined the European Economic Union in 1973. The oil crisis that year had also taken a toll.

The Labour Party Minister of Finance, Sir Roger Douglas, prior coming to office in 1984, wrote a book called There’s Gotta Be A Better Way.

The rising deadweight cost of taxes and regulation due to technological change, and the dissipation of wealth through rising cost structures progressively enfeebled the subsidised groups, allowing others to win the initiative after the 1970s in many countries including New Zealand.

The Labour Government radically reduced the size and role of the state. It corporatised and restructured government departments, often in preparation for privatisation, and sold some state assets to private investors. It abolished many economic controls and removed farming subsidies.

The additional political pressure that the winners had to exert to keep the same dollar gain from income redistribution had to overcome rising pressure from the losers to escape their escalating losses.

Eventually, the fight was no longer worthwhile relative to the alternatives. Taxed, regulated and subsidised groups can find common ground in wealth enhancing policies and an encompassing interest in mitigating any reduction in wealth from income redistribution policies.

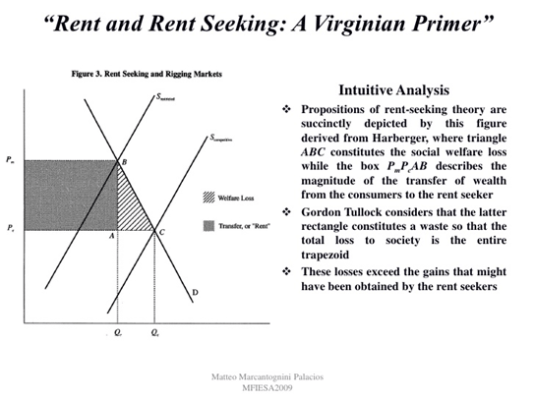

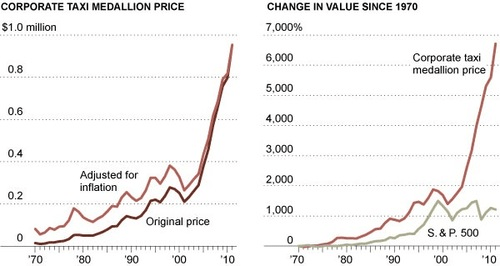

One barrier to reform is the transitional gains trap. The capitalisation of rents from taxi licenses is a classic example of the transitional gains trap.

Those who purchase the medallions from the owners at the time of initial regulation will pay the market rate for them and therefore will not receive any special rents. Yet, they will fight to prevent the taxi medallion system from being eliminated, since these owners will be harmed by such elimination. Thus, the city will be stuck with an inefficient medallion system that will be difficult to eliminate.

Eliminating the medallion program will harm existing taxis, many of whom did not lobby for the system in the first place and do not receive super competitive profits. The resources used in establishing the regulation or other programmes are lost forever.

Termination of a particular regulation or subsidies will nonetheless cause large capital losses for the incumbents. This will motivate incumbents to oppose reforms that jeopardise the income stream that has been previously capitalised (Tullock 1975; McCormick et al. 1984; Tollison and Wagner 1991). Any resources wasted in fighting economic reform must be deducted from the net gains from economic reform.

The literature on the transitional gains trap suggested that economic reform does not necessarily make society better off (Tullock 1975; McCormick et al. 1984; Tollison and Wagner 1991). The rent-seeking costs of the original privileges are capitalised and are lost forever. They are not regained by reform. The transitional gains trap is just a subset of a more general phenomenon indicating that deregulation can never replicate the status quo ante.

Too often it is assumed that deregulation can replicate the status quo ante. The prevailing model of deregulation is essentially a nirvana model, in that the gains from deregulation can essentially be had without cost. Further rent-seeking costs are incurred in lobbying for and against proposed reforms and these too are lost to forever.

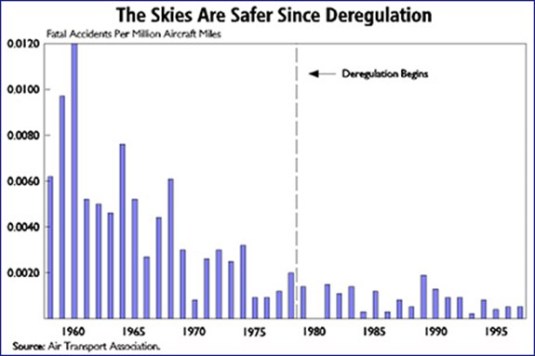

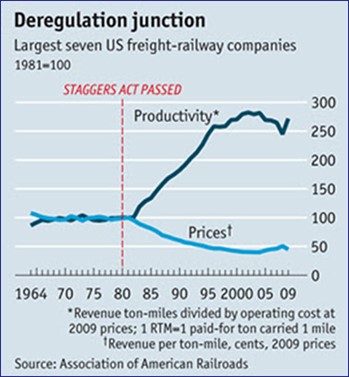

The standard analysis of deregulation too easily treats reform as a return to the status quo ante. Fred McChesney observed

The airline industry of 1999 is not the airline industry of 1978 minus the Civil Aeronautics Board.

The wealth lost in rent seeking is not recovered, or even recoverable by deregulation. Production possibilities have been irretrievably diminished (McCormick et al. 1984; Tollison and Wagner 1991).

Reform is not a free lunch. To the extent that specialised resources were involved in the rent seeking–resources that could have been devoted to amassing specific capital in producing the regulated good–the deregulated relative price must be higher than the pre-regulation or competitive price. The abstract of the relevant article by Tollison and Wagner is as follows:

This paper applies the theory of rent seeking to argue that economic reform, in the sense of correcting past deformities in the economy, does not pay from a social point of view. Economic reform, at best, should focus on the prevention of future deformities.

The analysis is developed in terms of the example of monopoly, but its applicability extends to any example of economic reform. The general principle underlying the analysis is that reform is not a free lunch, all the more so when the costs of the reformer and the resistance of the object of reform are taken into account.

Despite this, new institutions arise when social groups notice opportunities for new gains which are impossible to realise under the prevailing institutional arrangements (Diana Thomas 2009). The chances that new institutional frameworks may develop increase when these alternative technological opportunities and export markets become available.

Reform is more likely when the net benefits of reform become large because there is plenty left over for credible compensation of the losers who could block change (Acemoglu and Robinson 2005; Acemoglu 2008). An example is if taxes or regulation causes cost padding or delay new technologies. Shedding these inefficiencies are potential benefits for all.

The political secret of the East Asian economic miracles was the focus on export led industrialisation. Because the new industries were exporting rather than entering and competing with domestic suppliers to home markets, these domestic special interest groups had no reason to lobby against the establishment of these export industries and otherwise blocked both their entry and the adoption of new technologies. The social change is much more subtle. The local industry is simply had to pay more for contract as the export industries grew and bid away their labour force with higher pay.

Successful subsidised groups are often coalitions of sub-sets of producers, consumers, employees and input suppliers and deregulation is always a possibility if some members can benefit from joining another coalition (Peltzman 1976, 1989). A surprising number of incumbents of regulated and state-owned industries were unprofitable – some close to bankruptcy – because of rising cost structures, the growing losses from mandated services and erosion of rents through non-price competition with existing firms. They would have closed anyway but for bailouts.

The economic reforms that picked up pace around 1980 were a success as Andrei Shleifer’s paper

The Age of Milton Freedom begins

The last quarter century has witnessed remarkable progress of mankind. The world’s per capita inflation-adjusted income rose from $5400 in 1980 to $8500 in 2005.Schooling and life expectancy grew rapidly, while infant mortality and poverty fell just as fast.

Compared to 1980, many more countries in the world are democratic today. The last quarter century also saw wide acceptance of free market policies in both rich and poor countries: from private ownership, to free trade, to responsible budgets, to lower taxes.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments