Data extracted on 25 Jan 2016 01:07 UTC (GMT) from OECD.Stat.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

28 Jan 2016 Leave a comment

in politics - USA, public economics Tags: family tax credit, family tax credits, family taxation, in work tax credit

28 Jan 2016 Leave a comment

in applied price theory, economics of bureaucracy, financial economics, industrial organisation, politics - New Zealand, public economics

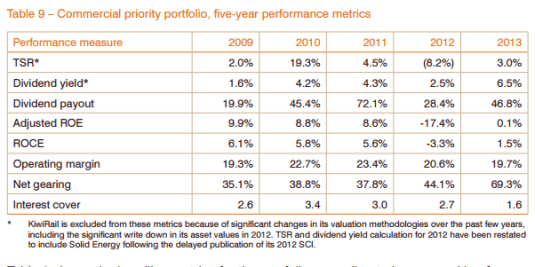

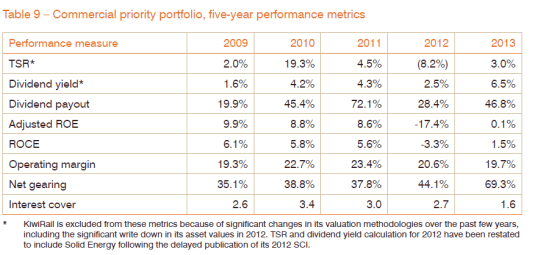

Today the Treasury advised that it no longer calculates an annual rate of return on the portfolio of state owned enterprises as a whole. It no longer publishes an annual portfolio report (APR).

Source: Treasury response to Official Information Act request by Jim Rose, 14 January 2016.

The Treasury regards the crown portfolio report which contains performance indicators on the state owned enterprises portfolio as a whole as too resource intensive.

The Treasury prefers to be more forward-looking in their reporting on a quarterly basis to the Minister of Finance. Unfortunately, the Treasury refused to my requests for access to this forward-looking reporting to the Minister of Finance on commercial-in-confidence grounds.

The forward-looking approach to state-owned enterprise performance is now only by the Treasury and the Minister of Finance. No one else has access to this financial performance information.

It is no longer possible to say using a figure calculated by the Treasury whether the portfolio of state owned enterprises as a whole are a good return to the taxpayer or not. Individual annual reports of the state owned enterprises can be reviewed but the portfolio wide rate of return is no longer available from the Treasury with the associated credibility of the same.

A common argument against state ownership is that as a whole government ownership is a bad investment. Specifically, the portfolio of state owned enterprises struggle to pay a return in excess of the long-term bond rate.

A common argument for continued state ownership is the loss of the dividends from privatisation. The vulgar argument such as by the New Zealand Labor Party and New Zealand Greens is if a state owned enterprise is privatised either partially or fully, the taxpayers no longer receive dividends. The fact that the sale price reflects the present value of future dividends is simply ignored.

Source: Treasury, Crown Portfolio Report 2013.

The sophisticated argument is the assets are under-priced such as for political reasons. Failed privatisations are indeed the best case against state ownership because governments cannot even sell an asset with such any degree of competence.

Governments are so bad as business owners and so incapable of running a commercial process free of politics that governments cannot even sell a state-owned enterprise for a good price under the full glare of the media and public.

Source: Treasury, Crown Portfolio Report 2013.

A reply to the loss of dividends argument is the dividends from the portfolio as a whole do not repay the government debt incurred to fund capital infusions into state-owned enterprises both when initially established and through time. In that case, it is better to leave your money in the bank than in the state of enterprise.

John Quiggin often criticises privatisation on the grounds that state owned enterprises can invest at a cheaper rate because they are financed at the long-term bond rate:

In general, even after allowing for default risk, governments can borrow more cheaply than private firms. This cost saving may or may not outweigh the operational efficiency gains usually associated with private ownership.

It is not possible to scrutinise that argument without an annual rate of return on the portfolio of state owned enterprises as a whole to see if it is true at first pass at least. As the Treasury no longer calculates a rate of return on the portfolio and taxpayers’ equity, that debate comes to something of a crashing halt in New Zealand.

If these state owned enterprises were privately owned and listed on the share market, investors would just look at trends in share prices for daily measure of expected future profitability.

John Quiggin made the best simple summary of the case for privatisation which was the selling the dogs in the portfolio:

The fiscal case for privatisation must be assessed on a case by case basis. It will always be true for example that if a public enterprise is operating at a loss, and can be sold off for a positive price with no strings attached, the government’s fiscal position will benefit from privatisation.

Various early ventures in public ownership, such as the state butcher shops operated in Queensland in the 1920s (apparently a response to concerns about thumbs on scales) met this criterion, and there doesn’t seem to be much interest in repeating this experiment.

Quiggin also made a measured statement of why state ownership should be limited at most to monopolies:

In most sectors of the economy, the higher cost of equity capital is more than offset by the fact that private firms are run more efficiently, and therefore more profitably, than government enterprises.

But enterprises owned by governments are usually capital intensive and often have monopoly power that entails close external regulation, regardless of ownership. In these situations, the scope to increase profitability is limited, and the lower value of the asset to a private owner is reflected in the higher rate of return demanded by equity investors.

Quiggin is wrong about government enterprises have been a lower cost of capital because it contradicts the most fundamental principles of business finance as explained by Sinclair Davidson:

…it is clear that the Grant-Quiggin view violates the Modigliani-Miller theories of corporate finance. The cost of capital is a function of the riskiness of the investment projects and not a function of a firm’s ownership structure.

How the cash flows of a business are divided between owners and creditors does not matter unless that division changes the incentives they have to monitor the performance of the firm and keep it on its toes. Those lower down the pecking order if things go wrong such as owners have much more of an incentive to monitor the success of the business and lift its performance.

Capital structures of firms, the property rights structures of firms, matter precisely because they influence incentives of those with different claims on the cash flows of the firm.

Having to pay debt disciplines managerial slack and ensures that free-cash flows are used to repay debt (or pay dividends) rather than be invested in low quality new ventures. Having to borrow from strangers such as banks ensures regular scrutiny of the soundness and prospects of the company from a fresh set of eyes. Capital structures made up of both debt and equity keeps the firm on its toes.

Unfortunately, in New Zealand it is much more difficult to review the arguments for and against the current size and shape of the state owned enterprise portfolio as for example summarised by John Quiggin:

Technologies and social priorities change over time, with the result that activities suitable for public ownership at one time may be candidates for privatization in another. However, the reverse is equally true. Problems in financial markets or the emergence of new technologies may call for government intervention in activities previously undertaken by private enterprise.

In summary, privatization is valid and important as a policy tool for managing public sector assets effectively, but must be matched by a willingness to undertake new public investment where it is necessary.

As a policy program, the idea of large-scale privatization has had some important successes, but has reached its limits in many cases. Selling income-generating assets is rarely helpful as a way of reducing net debt. The central focus should always be on achieving the right balance between the public and private sectors.

This balancing of public and private ownership is more difficult in New Zealand because portfolio wide rates of return are unavailable unless you calculate them yourself. That must be labour-intensive given the Treasury thought it was too labour-intensive for it to do for itself.

An obvious motive to start a review the extent of state ownership is the portfolio is performing poorly. That warning sign is no longer available because the crown portfolio report is no longer published.

One way to fix an underperforming portfolio is to sell the dogs in the portfolio. One of the first ways owners notice dogs in their portfolio is the portfolio not returning as well as it used too because of the emergence of these dogs so further enquiries are made and explanations sought.

Taxpayers, ministers and parliamentarians are all busy people with little personal stake in the rate of return on the state owned enterprises portfolio.

Taxpayers, ministers and parliamentarians will all first look at the portfolio wide rate of return to see whether more detailed scrutiny of individual investments is required. That quick check against poor value for money and trouble ahead is no longer available on the state owned enterprises portfolio in New Zealand.

27 Jan 2016 Leave a comment

in politics - New Zealand, public economics Tags: Denmark, family tax credits, family taxation, in-work tax credits, Sweden, taxation and labour supply

27 Jan 2016 Leave a comment

in constitutional political economy, fiscal policy, politics - New Zealand, Public Choice

The focus group work of Lord Ashcroft after the 2015 British general election reinforces what was learnt about the New Zealand Labour Party’s drift away from the values of the working class.

Source: The Unexpected Mandate: my review of the 2015 election and the unusual parliament that preceded it – Lord Ashcroft Polls.

In the 2014 election in New Zealand, the Labour Party promised to extend the in work tax credit for families to welfare beneficiaries. This was worth about $60 a week.

The following week was the worst week that Labour Party MPs and party workers experienced in their door-knocking. In their own Heartland electorates, the Labour Party door knockers received a hostile response to that proposal.

Working class Labour voters believe they had earned that family tax credit by working and it should not be paid to people who do not earn it by working.

There is a re-occurring theme among those who stopped voting labour everywhere is that Labour Party is are now too concerned about scroungers and are not interested enough in rewarding strivers, and in particular those who strive to improve themselves in the working class.

Ashcroft’s research after the 2010 British general election found that British voters who had stopped voting Labour after previously supporting it believed that the Labour Party did not have the right answers to important questions. 7 out of 10 of these voters believe that the expenditure cuts of the Conservative party when necessary.

Importantly for labour parties everywhere, two thirds of voters would take a lot of persuading before they voted for the British Labour Party again. Labour would need to change quite fundamentally before they did so again.

Many said they would wait until Labour had been re-elected and served a full term before they themselves considered voting Labour again. That means two thirds of the vote lost by Labour were unwilling to vote Labour again until the 2025 general election. They had really given up on Labour despite their support for it in the past. Issues such as a perception that Labour elected the wrong brother as its leader in 2010 were minor in comparison to this.

Fortunately for the Conservative Party, research among Labour Party members and Labour supporters in the trade unions tells a very different message as to why Labour lost the 2010 British general election.

These Labour Party members and supporters thought the voters were wrong to not vote for them according to the Ashcroft research after the 2010 election:

They thought they had lost because people did not appreciate what Labour had achieved; that voters had been influenced by the right-wing media; and that while Labour’s policies had been right, they had not been well communicated.

More than three quarters thought their party had not deserved to lose, and most rejected the idea that the Labour government had been largely to blame for the economic situation.

They thought the swing voters they had lost (and needed to win back) were ignorant, credulous and selfish. More than half thought the coalition would prove so unpopular that Labour would probably win the 2015 election without having to change very much.

The strength of British Labour in the eyes of many voters is it is seen as compassionate and concerned about fairness. Unfortunately for British Labour, many of the people who do not currently vote for Labour but are receptive to these messages of compassion and fairness re fiscal conservatives according to the Ashcroft research:

I found in my focus groups that this message was best received by those already most inclined to vote for the party.

It was less effective for those who had harder questions, particularly about how all this compassion and decency would be paid for. As one of our participants put it, ‘it’s all well and good to say we’re nicer people and we care about you more, but I want someone who can sort out the country’.

27 Jan 2016 Leave a comment

in labour economics, labour supply, politics - New Zealand, poverty and inequality, public economics Tags: family tax credit, growth of government, negative income tax, size of government, social insurance, universal basic income, welfare state

Things are pretty grim when your ideas for fixing child poverty by throwing a lot more money at the problem are easily outclassed by the Greens in terms of economic rationale, fiscal sense and political practicality.

Source: Greens launch billion dollar plan to reduce child poverty | Green Party of Aotearoa New Zealand.

But that is the case for Gareth Morgan’s proposals for a universal basic income for New Zealand. His proposal for a universal basic income funded by comprehensive capital tax make much less sense than those of the Greens for giving the in work family tax credit for those do not work but are on a welfare benefit.

The Greens have a far superior proposal for reducing child poverty and a far better chance of getting it implemented in parliament. Their proposal is simply to introduce a parental tax credit and give the in work tax credit to those currently on the benefit to increase their incomes.

Gareth Morgan’s solution to child poverty is to give billions of dollars to adults not in poverty and leave those who are in poverty worse off under the universal basic income. It is obvious which of these is more likely to attract political support and provoke resistance from taxpayers and political parties willing to court those are opposed to great big new taxes.

One of the economic reforms in the 1980s and 1990s that saved the welfare state was more efficient taxes and more efficient government spending. The targeting of government social spending reduce growth in the overall tax burden and therefore the political resistance it provoked.

Government spending grew in many countries in the 20th century because of demographic shifts, more efficient taxes, more efficient spending, a shift in the political power from those taxed to those subsidised, shifts in political power among taxed groups, and shifts in political power among subsidised groups. Sam Peltzman argues that:

governments grow where groups which share a common interest in that growth and can perceive and articulate that interest become more numerous.

The median voter in all countries was alive to the power of incentives and to not killing the goose that laid the golden egg. After 1980, the taxed, regulated and subsidised groups had an increased incentive to converge on new lower cost modes of redistribution.

More efficient taxes, more efficient spending, more efficient regulation and a more efficient state sector reduced the burden of taxes on the taxed groups. Most subsidised groups benefited as well because their needs were met in ways that provoked less political opposition.

Gary Becker and Casey Mulligan in Deadweight Costs and the Size of Government (NBER Working Paper Number No. 6789) concluded that flatter and broader taxes encourage bigger government. This is because taxpayers offer less resistance to increases in flat tax rates than to more onerous and less efficient forms of taxation. Any decline in the resistance of taxpayers to taxes leads to larger governments since an endless number of groups lobby to divide up the large revenue base.

An inefficient tax system or spending program from the standpoint of optimal tax theory can improve taxpayer welfare this so-called inefficient system creates additional political pressure for suppressing the growth of government. Inefficient taxes do not raise much revenue and therefore do not support a large sized government.

A switch to more efficient taxes through tax reforms allows governments to raise the same amount or larger amount of revenue for the same level of political resistance from taxpayers. This is because less revenue and output is wasted by discouraging labour supply, investment, savings and investment in capital with high marginal rates of tax on narrower tax basis.

The rising deadweight losses of taxes, transfers and regulation all limit the political value of inefficient redistributive policies. Tax and regulatory policies that are found to significantly cut the total wealth available for redistribution by governments are avoided relative to the germane counter-factual, which are other even costlier modes of redistribution.

Long live the Slopegraph. Long live Edward Tufte. tinyurl.com/naeh7rc http://t.co/C8Lgnupxz9—

Amity Shlaes (@AmityShlaes) May 16, 2015

Everyone can gain from converging on more efficient modes redistribution. The tax burden is less than otherwise. Government spending is more than a wise because taxes are raised with less deadweight social costs.

An improvement in the efficiency of either taxes or spending reduces political pressure from taxed and regulated groups for suppressing the growth of government and thereby increases total tax revenue and spending because there is less political opposition. Improvements in the efficiency of taxes, regulation and in spending reduce political pressure from the taxed and regulated groups in society.

The post-1980 reforms of Thatcher, Reagan, Clinton, Hawke and Keating, Lange and Douglas and others saved the modern welfare state. Their moves towards more efficient taxes and better targeted social spending did reduce growth in government spending but also prevented even larger cuts to social spending since 1980 at the behest of the increasingly restive taxpayer.

Social spending growth did temper after 1980 but the level of spending was larger than otherwise because of the extra revenue raised through more efficient taxes – more efficient taxes which provoked less political opposition.

More efficient taxes, more efficient spending, more efficient regulation and a more efficient state sector reduced the burden on the taxed groups while still supporting extensive but more tempered social spending.

Governments everywhere hit a brick wall in terms of their ability to raise further tax revenues. Political parties of the Left and Right recognised this new reality. Gareth Morgan has not when he proposes a great big new tax to fund his universal basic income.

Billions of extra dollars in revenue must be raised and political resistance provoked to his proposed comprehensive capital tax to fund a universal basic income for those who are not poor. Child poverty is not reduced by a universal basic income because single parents and the children receive no more income support from government than before.

Which has more political legs? The Greens’ proposal to raise taxes by $1 billion to fight child poverty or the proposal by Gareth Morgan to raise taxes by 10 times that and have less impact on child poverty?

The current and future governments of New Zealand have enough on their plate to work out how to fund a universal old age pension and health spending without giving away billions of dollars to the non-poor through an universal basic income.

26 Jan 2016 Leave a comment

in economics of bureaucracy, politics - New Zealand

Bill English, the Minister of Finance, acquiesced to the Treasury killing the publication of the Crown Portfolio Report. This report summarises the performance of the state owned enterprises in New Zealand. This portfolio is a dog of an investment for the taxpayer.

Treasury decided that the best way to deal with this terrible return to the taxpayer on billion tens of billions of dollars in assets, assets struggling to get a return that is above zero much less the long-term bond rate, was to stop publishing this inconvenient data.

Source: Reporting – Portfolio of Commercial Entities — The Treasury – New Zealand

When I have sought the figures on the portfolio rate of return for the last two years through the Official Information Act to bring the table below up-to-date, I am told by Bill English that I can look up the annual reports of 49 state owned enterprises up for myself and do the calculation.

For that reason, the information on portfolio rates of returned for state owned enterprises, which I sought under the Official Information Act was publicly available and therefore the Treasury and the Minister of Finance both had a good reason under the legislation to turn my request down for access to that official information.

To put it mildly, the difference in credibility of a calculation of the rate of return of the portfolio of state owned enterprises made by the Treasury and by an angry blogger are beyond measure.

26 Jan 2016 Leave a comment

in applied price theory, labour supply, law and economics, politics - New Zealand, poverty and inequality, public economics

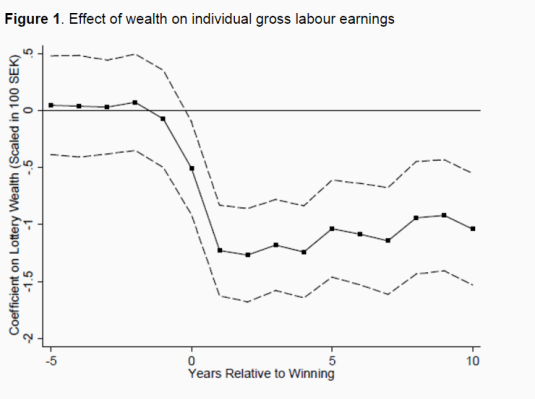

One of the many drawbacks of the universal basic income is it will induce the recipients to cut back on their labour supply. There are studies of this labour supply effect through the study of what happens when people win the lottery – either the big one or a small prize.

Winning the lottery is the equivalent of winning an annuity equal to whatever annual income you can get it current low interest rates and share market returns.

A surprisingly number of people on the Left who deny that taxes have significant labour supply effects will nonetheless accept that winning the lottery will induce people to quit work permanently or cut back at least. The most likely reason is they buy lottery tickets too.

A study has just come out on the labour supply effects of winning the Swedish lottery. The sample in this study was really big: several million Swedish lottery winners.

Sweden seems to be like the USA in that both are awash with interesting economic data to the many other countries do not collect. Moreover, they were able to study these Swedish lottery winners over a 5 to 10-year period. Labour supply detail at that level is like going to heaven for an empirical labour economists.

Source: Labour supply responses of lottery winners | VOX, CEPR’s Policy Portal.

The researchers found that in common with a previous study of the labour supply of lottery winners after their win that there were

modest reductions in labour earnings suggesting every dollar of universal basic income would reduce labour earnings by roughly $0.11.

The new research also found productivity losses of $1.40 for every hundred dollars of lottery winnings and that the partners of the lottery winners cut back on their labour suppliers well. No surprise there. Taking all these labour supply effects into account, our researchers concluded that:

every dollar won in a lottery reduces lifetime after-tax labour earnings of winners by $0.10-$0.20.

All in all, the universal basic income will be a negative productivity shock built on a negative productivity shock. First of all, there is the great big new tax to fund the universal basic income. Then the recipients of the basic income will cut back on their labour supply further compounding the massive social costs of the universal basic income.

A universal basic income is a bad idea from start to finish and that is before you consider the many advantages of encouraging people to work for their living. Working for your living is a central expectation of adult life.

UPDATE: what is the magnitude of this labour supply drop from universal basic income? The usual labour supply effect of a recession as recently summarised by Richard Rogerson is as follows:

Consider by way of comparison the labour market fluctuations associated with the business cycle. Going from normal times to a fairly severe recession is usually associated with a drop in total hours worked of about 3 percent.

A universal basic income will push the New Zealand economy into recession off the back of labour supply effect from the windfall increase in incomes alone. That is before you consider the massive productivity shock pushing the economy down further through a massive increase in the taxation of capital, which is the most inefficient form of taxation.

26 Jan 2016 Leave a comment

in politics - Australia, politics - New Zealand, politics - USA, public economics Tags: Australia, earned income tax credit, family tax credits, family taxation, in-work tax credits, working for families

26 Jan 2016 Leave a comment

in applied price theory, applied welfare economics, economic history, international economics, politics - USA Tags: 2016 presidential election, China, tariffs, trade wars

25 Jan 2016 Leave a comment

in politics - New Zealand, public economics Tags: family tax credits, family taxation, in-work tax credits, taxation and labour supply, working for families

In work tax credits for families in Working For Families certainly makes a difference to the after-tax, after government transfers living standards of the family on an average wage.

Data extracted on 25 Jan 2016 01:07 UTC (GMT) from OECD.Stat.

24 Jan 2016 Leave a comment

in applied price theory, development economics, economic history, economics of bureaucracy, economics of regulation, Marxist economics, politics - USA

23 Jan 2016 Leave a comment

in economics of education, Marxist economics, politics - New Zealand, public economics

23 Jan 2016 Leave a comment

in applied price theory, development economics, economic history, international economic law, international economics, politics - New Zealand, Public Choice

If our friends on the left are to be believed, trade liberalisation is bad unless it involves Cuba, Vietnam, Iraq and other heroes of the anti-west left. The anti-west left is different from the antifascist left and is sometimes known as the renegade left or regressive left.

Access to world markets, and the removal of trade sanctions and travel and investment restrictions are all to the benefit of the Vietnamese, Iraqi and Cuban people in the street and not just their elites in the eyes of the anti-west left. There you have: trade liberalisation is bad because reduced tariffs at home and abroad hurts ordinary people; trade sanctions are bad because they hurt ordinary people by denying them access to import from and exporting into world markets.

Trade sanctions against Iraq were to terrible for the Iraqi people. Removing those trade sanctions and similar sanctions on Cuba and Vietnam, which expanded their ability to export and import was essential to improving the welfare of Iraqis, Cubans and Vietnamese respectively. Two of these three countries are not a democracy with the guarantees elections have in ensuring broad-based benefits but nonetheless greater trade liberalisation was seen as to the advantage of the ordinary people of those dictatorships by the Left.

https://twitter.com/GazaReports/status/686399912485994496

Likewise boycotting, disinvesting and sanctions on Israel will change the Israeli policy because the Israeli people. The logic here is that trade and investment is wealth enhancing, so restricting trade punishes Israelis.

Source: Kennedy, New Zealand Greens: Tipping points – Israel, Palestine, and peace.

A comprehensive study by Kim Elliott, Jeffrey Schott, and Gary Hufbauer looked at whether sanction works. Do they accomplish the goals identified by U.S. policy-makers such as ending apartheid or undermining Libya’s support of terrorism? The study estimated they have succeeded 23 percent of the time. But of course as Kaempfer and Lowenberg say

Sanctions may be imposed not to bring about maximum economic damage to the target, but for expressive or demonstrative purposes. Moreover, the political effects of sanctions on the target nation are sometimes perverse, generating increased levels of political resistance to the sanctioners’ demands.

It is also that case that Kaempfer, Lowenberg and Mertens (2001) found that sanctions generate rents that can be appropriated by a dictator and his cronies and supporters such as those who were close to Saddam. The losses from the sanctions were borne by those who are opposed to the regime. This weakens their capacity to oppose it, leading to the further entrenchment in power of the dictator and his supporters. As Wintrobe explains:

In the public choice approach, sanctions work through their impact on the relative power of interest groups in the target country. An important implication of this approach is that sanctions only work if there is a relatively well organized interest group whose political effectiveness can be enhanced as a consequence of the sanctions.

What is reasonably clear from the literature on the economics of trade sanctions is at ordinary people in both dictatorships and democracies suffer from trade sanctions the most. The political elite can shift the costs of the trade and investment sanctions onto the disenfranchised within their country. Those with political connections have a better chance of minimising the costs and profiting from any windfall rents:

as Galtung (1967) observes, sanctions can be counterproductive by giving rise to a new elite in the target nation that benefits from international isolation. For example, Selden (1999) notes that, in the long run, sanctions often foster the development of domestic industries in the target country, thus reducing the target’s dependence on the outside world and the ability of sanctioners to influence the target’s behaviour through economic coercion…

Damrosch (1993, p. 299) contends that sanctions will almost inevitably benefit an autocratic regime because the regime will always be in a better position than the civilian population to control external transactions and the internal economy. In Damrosch’s view, the creation and enrichment of a criminal class that profiteers from trading bootleg or scarce goods means that even the most skilfully targeted sanctions will serve only to entrench the power of the ruling elite

One of the hopefully unintended consequences of trade and investment sanctions is disinvestment entrenches the position of capitalists in the sanctioned country and raises the rate of return on the capital in the targeted country as Kaempfer and Lowenberg again found:

…disinvestment sanctions can have the perverse effect of enhancing the target country’s ability to pursue its objectionable behaviour. The existing foreign capital stock – the physical plant and capacity previously owned by foreigners – is purchased by domestic capital owners at reduced prices, causing yields to rise and prompting target-country residents to sell foreign assets and substitute into domestic assets with higher rates of return.

The increase in the rate of return due to the acquisition of productive assets at fire-sale prices translates into a windfall gain to domestic capital owners, which increases the tax base available to the government to finance its policies, including those that attracted the sanctions in the first place

So far so good in terms of international economics of the renegade left until we start considering their attitude to trade agreement such as the Trans-Pacific Partnership. The logic of BDS is swept aside as is the rationale for opposing trade sanctions against Iraq, Cuba and Vietnam. Now enhanced opportunities for trade and investment is not in the interests of ordinary people even if they are Vietnamese – the biggest winner from the Trans-Pacific Partnership.

Now increased opportunities to export are a bad thing. Investor state dispute settlement procedures, which were initially proposed by the governments of poor countries such as in South America, which offer a relief to foreign investors against expropriation and discrimination become a bad thing. Safeguards against corrupt and venial developing country politicians, bureaucrats and courts expropriating foreign investors are a bad thing even if you are talking about Vietnam or Cuba.

The Greens are the first to call for trade sanctions as an alternative to military intervention. Trade sanctions on the grounds of human rights violations as far back apartheid in South Africa make no sense unless the reduced access to world markets imposes a cost on a country. In the case of a democracy like Israel, trade sanctions must hurt the man in the street otherwise the sanctions will not shift electoral fortunes.

The last line of defence of the trade sanctions work but trade liberalisation is bad line of thought is most of the profits and losses of both trade sanctions and trade liberalisations fall on the elite. It is a trickle up argument.

The first flow in that argument is the sanctions against apartheid in South Africa and Rhodesia. They were aimed at ordinary people such as those that play and watch cricket, rugby and other sports. The idea is to encourage people to change their political views and votes if they want access to global sport.

Both Rhodesia and South Africa were democracies for whites. White settler politics in Rhodesia was particularly colourful. It was a brave man to make any statement that put him at the risk of being overtaken on his right in white settler politics.

The bigger problem for the trade sanctions are good, trade liberalisation is bad argument comes from the interest group based explanations of industrialisation in Japan and the East Asian Tigers. Economic development often comes to developing countries through export based industrialisation.

The reason that export based industrialisation is a common path to economic development for poor countries is it does not threaten the existing configuration of special interests. It does not involve deregulating any domestic industry. The export industries do not threaten the business interests and profits of existing rent seekers and ruling elites.

Post-war trade liberalisation and tariff cuts gave Korean and the other East Asian Tigers much greater access to major export markets. This allowed export production to expand without limit. This expansion did not threaten local special interests because they kept their privileges and barriers to entry into the domestic markets.

Incumbent suppliers and workers are less likely to be hurt by the adoption of more efficient technologies because output expands greatly through exporting. If a market is small and limited to one country, and output cannot be increased without price cuts, greater production efficiency from a new technology can lead to less employment and business closures. Industry insiders may oppose this. Exporting reduce the incentives for insiders to block more efficient technologies (Parente and Prescott 2005; Holmes and Schmitz 1995; Olson 1982). Distributional coalitions slow down a society’s capacity to adopt new technologies and to reallocate resources in response to changing conditions and thereby reduce the rate of economic growth.

Many other under-developed nations did not grow because institutional sclerosis locked them into yesterday’s technologies and industries with low growth and major declines in relative incomes (Olson 1982, 1984; Heckelman 2007; Bischoff 2007). A growing accumulation of distributional coalitions – institutional sclerosis – slowed down the capacity of these under-developed countries to adopt new technologies and reallocate resources across firms and industries in response to changing conditions and new opportunities (Olson 1982, 1984; Acemoglu and Robinson 2005).

Mancur Olson argued that over time, stable societies accumulate “distributional coalitions,” narrow special-interest organizations that burden the economy with overregulation and opaque forms of wealth redistribution.

Latin America is a good example of stagnation after initial prosperity because of the accumulation of barriers to efficient production. Latin America has many more international and domestic barriers to competition than do Western and the successful East Asian countries (Cole et al. 2005).

Institutional reforms and imported new technologies increased employment and incomes through this explosion in exporting in Japan and the newly industrialised countries in East Asia. This allowed the losers from the economic changes to be compensated directly or with new opportunities in the export sectors (Parente and Prescott 1999, 2005; Olson 1982, 1984; Acemoglu and Robinson 2005).

The argument that trade sanctions are good while trade liberalisation is bad simply does not stand up against the economic history of trade sanctions, trade liberalisation and export-led industrialisation. If they did, the economic histories of Latin America and East Asia would swap. Latin America took the path of import substitution and crony capitalism while East Asia chose export led industrialisation, low taxes and the market economy.

22 Jan 2016 Leave a comment

in labour economics, labour supply, politics - USA, public economics Tags: British economy, Canada, earned income tax credits, family tax credits, family taxation, taxation and labour supply

22 Jan 2016 Leave a comment

in discrimination, economics of love and marriage, gender, human capital, labour economics, occupational choice, politics - New Zealand Tags: asymmetric marriage premium, family wage gap, gender wage gap

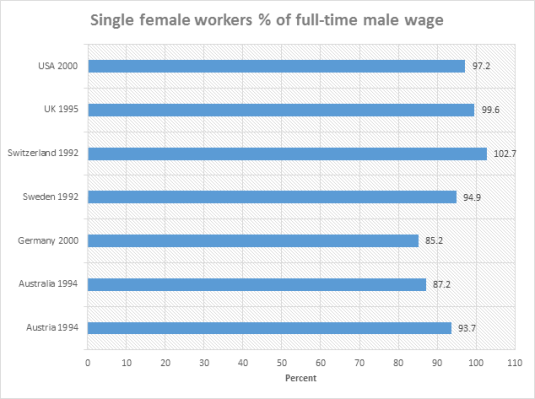

If victory is a zero gender wage gap, some countries have achieved it already for single female workers and long ago according to the data charted below is from the Luxembourg Income Study.

Source: IZA World of Labor – Equal pay legislation and the gender wage gap from the Luxembourg Income Study.

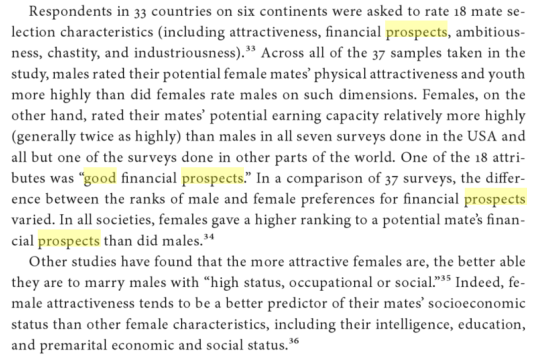

Discrimination cannot explain why the gender wage gap for single female is tiny relative to the family wage gap. As Solomon Polachek explains:

…the wage gap for married workers is between three and 30 times greater compared with single workers.

Employers cannot be to blame for the large difference between the single female worker gender wage gap and the family wage gap.

Aside from explaining why employers only discriminate against married women, you must explain how employers managed to find out which female applicants are married so they can discriminate against them.

Without that vital information on the marital status of female applicants and the presence and number of children as well is their spacing, the vast male chauvinistic conspiracy responsible for the glass ceiling and the sticky floors against promotion does not get off the ground.

How do employers actually pay married women less? Advertising jobs that pay women less has been unlawful for decades. Yet another hurdle to overcome for the vast male chauvinistic conspiracy.

Women move between the large number of jobs as do men accumulating human capital as they go? Somehow employers, including female owned firms, must sabotage the accumulation of human capital by married women as soon as they have children but without paying them lessen in their current jobs or advertising jobs that pay married women less.

The main drivers of the gender wage gap are unknown to employers such as:

These are the main drivers of the gender wage gap – all of which are factors totally unknown to employers and of no relevance to them in making a profit.

Most explanations of the gender wage gap centre around human capital. In anticipation of time outside of the workforce for motherhood, women self-selecting to occupations that penalise career interruptions less.

Women invest in human capital that is more general, human capital that is more mobile between jobs and into spells of part-time work. Women anticipate home time after they have children so they invest in human capital that depreciations at a slower rate during career interruptions. Women also invest less overall in new capital because they expect to spend less time in the labour market.

All of these investments are made by women themselves in anticipation of motherboard rather than employers somehow paying them less after they marry and have children.

The solution to closing the family wage gap requires radical biological changes in who has children. There are more radical changes required than this because mothers actually like babies and enjoy spending time with them rather than going to work.

Equally challenging is the required changes in the dating market. There is an average age difference between boyfriends and girlfriends and husbands and wives of 2 to 3 years. As the husband or boyfriend is a few years older, he has usually accumulated more human capital and is more likely to be at a critical career point for promotion.

Because the husband or boyfriend is 2 to 3 years older, it pays off well in terms of the father investing more in market-related human capital and the mother devoting more time to childcare.

Another major driver of the gender pay gap is the dating market as identified by Richard McKenzie. He pointed out that evolutionary psychology has found that in every culture one of the factors of influencing pairing off in the dating market is that the boyfriend or husband must have good prospects although this preference is weakening over this last century.

One of the reasons for the increase in single parents is that low-paid men are not as inviting prospects as long-term boyfriends or husbands is a few generations ago. There are too few good men.

University educated couples are not called power couples for nothing – their earning power is this stunning compared to going it on your own. The emergence of power couples means that less educated women may prefer to stay single and raise children on their own rather than marry what is left in the marriage pool.

Because of the requirement among women across all cultures that husbands to be must have good prospects, men have an extra incentive to invest in human capital and work harder and longer hours because of the gender specific payoff in the marriage market.

Men will also take more risks than women because risky jobs carry wage premiums. That risk premium is topped up in the mating market terms are marriage prospects because of the higher wages. Women get a wage premium for taking risky jobs but less of a payoff in the mating market for the higher wages. There is an evolutionary psychology explanation for the family wage gap.

All in all, a key requirement for the closing of the family wage gap and what little is left of the gender wage gap is women drop their standards in terms of who they choose as boyfriends and husbands. Not very likely.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments