David Friedman “Global Warming, Population, and the Problem with Externality Arguments”

28 Nov 2017 Leave a comment

in applied price theory, applied welfare economics, environmental economics, global warming Tags: David Friedman, externalities

Visions of Anarchy – James Scott, David Friedman, & Robert Ellickson

12 Dec 2016 Leave a comment

in comparative institutional analysis, constitutional political economy, law and economics Tags: David Friedman, economics of anarchy

@jamespeshaw nails the #TPPA policy trade-off @NZGreens

06 Oct 2015 1 Comment

in applied price theory, applied welfare economics, comparative institutional analysis, economics of regulation, international economic law, international economics, International law, law and economics, politics - Australia, politics - New Zealand, politics - USA, property rights Tags: conspiracy theories, David Friedman, foreign direct investment, free trade agreements, FTI, international investment law, Leftover Left, New Zealand Greens, preferential trading agreements, TPPA, Twitter left

About 1% more GDP but higher drug prices.

Source: No increased medicine costs under TPPA | Stuff.co.nz

.@MSF: Patients and treatment providers in developing countries the big losers of the #TPP bit.ly/TPPconcludes http://t.co/cbikANleyA—

MSF Access Campaign (@MSF_access) October 05, 2015

The next best arguments James Shaw made were xenophobia about foreign investment in land and some vast conspiracy theory regarding endangered dolphins.

When your next best argument is foreigners are coming to buy up all our land, you are playing from a weak populist hand. About half of million New Zealand born live in other countries.

About 80% of these live in Australia, the great majority as residents rather than as citizens. These New Zealanders living in Australia and elsewhere need protection under international agreements to ensure they are not the victim of populist outbreaks against the sale of land to foreigners.

Source: Statistics New Zealand.

In addition, if a foreigner wants to pay over the odds for my house I am glad to separate a fool from his money.

Source: Statistics New Zealand.

New Zealand has a strong interest in protecting the rights of its own expatriates as well as New Zealand foreign investors to buy land in other countries. As David Friedman explains:

Much more commonly, [economic imperialism] is used by Marxists to describe–and attack–foreign investment in “developing” (i.e., poor) nations. The implication of the term is that such investment is only a subtler equivalent of military imperialism–a way by which capitalists in rich and powerful countries control and exploit the inhabitants of poor and weak countries.

There is one interesting feature of such “economic imperialism” that seems to have escaped the notice of most of those who use the term. Developing countries are generally labour rich and capital poor; developed countries are, relatively, capital rich and labour poor. One result is that in developing countries, the return on labour is low and the return on capital is high–wages are low and profits high. That is why they are attractive to foreign investors.

To the extent that foreign investment occurs, it raises the amount of capital in the country, driving wages up and profits down. The effect is exactly analogous to the effect of free migration. If people move from labour-rich countries to labour-poor ones, they drive wages down and rents and profits up in the countries they go to, while having the opposite effect in the countries they come from.

If capital moves from capital-rich countries to capital-poor ones, it drives profits down and wages up in the countries it goes to and has the opposite effect in the countries it comes from. The people who attack “economic imperialism” generally regard themselves as champions of the poor and oppressed.

To the extent that they succeed in preventing foreign investment in poor countries, they are benefiting the capitalists of those countries by holding up profits and injuring the workers by holding down wages. It would be interesting to know how much of the clamour against foreign investment in such countries is due to Marxist ideologues who do not understand this and how much is financed by local capitalists who do.

Zero hour contracts may be outlawed in New Zealand–updated

13 Apr 2015 1 Comment

in entrepreneurship, industrial organisation, labour economics, labour supply, managerial economics, occupational choice, organisational economics, personnel economics, politics - New Zealand, survivor principle, unions Tags: Aaron Director, creative production, David Friedman, inherent inequality of bargaining power between workers and employers, Richard Epstein, Ronald Coase, The fatal conceit, The pretence to knowledge, zero hours contracts

In another triumph of the Socialist Left of the National Party, the supposedly centre-right New Zealand government is considering outlawing zero hours contracts:

ONE News can exclusively reveal the Workplace Relations Minister is leaning towards outlawing the contracts and other employment provisions that he sees as unfair…

The Minister of Workplace Relations said the most punitive aspects of zero-hour contracts will be banned:

Mr Woodhouse has previously said a ban of zero-hour contracts would be an overreaction, but signalled the outlawing of aspects including:

•Restraint of trade clauses that stop someone working for a competing business if an employer does not provide the desired hours of work.

•The cancellation of shifts at short or no notice.

One reason for this is to neutralise a wedge issue with the Labour Party. The labour parties in both New Zealand and United Kingdom plan to outlaw zero hours contracts.

The NZ Labour Party’s Certainty at Work private member’s bill would require employment agreements to include an indication of the hours an employee will have to work to complete tasks expected of them.

Aaron Director pointed out that there are many real world business practices that behave differently from the caricatures in textbooks and arouse suspicious responses from economists (as well as from lay observers including lay observers with no ideological agenda).

Director said that visions of market power dance their heads and some of these suspect practices have been regulated for reasons he attributed in a large part to intellectual laziness. Ronald Coase made the same observation about knee-jerk responses to perplexing new business practices:

One important result of this preoccupation with the monopoly problem is that if an economist finds something—a business practice of one sort or other—that he does not understand, he looks for a monopoly explanation.

And as in this field we are very ignorant, the number of ununderstandable practices tends to be rather large, and the reliance on a monopoly explanation, frequent.

Much of the lasting influence of Aaron Director and of Ronald Coase came from their ability to show that simple judgements about business practices often cannot withstand rigorous scrutiny.

The organisation of and the contracting practices in the labour market is not a complicated despite the best efforts of the Left over Left and unions to pretend that it is so, as Richard Epstein explains:

Labour markets are not characterized by tricky externalities. They do not pollute streams or require the creation of public goods.

They are not characterized by genuine breakdowns in information, as workers are in a position to observe the conditions of their employment on a day-to-day basis.

Left to their own devices, without explicit support from union activities, they will be highly competitive, and thus work hard to allocate scarce human capital to its most productive use.

Workers have the option to quit for higher wages, and employers can always seek out low cost techniques to reduce their labour costs. Any short-term dislocation for firms or individuals is more than offset by the overall increase in the system productivity, spurred in part by clear signals that should increase investments in human capital.

In the UK, the Work Foundation found that 80% of those on zero hours contracts are not looking for another job; only 26% wanted longer hours. This implies that 74% were content with their current work times arrangements.

Labour's zero hours myth breitbart.com/london/2015/04… http://t.co/M8JsW6NWSF—

Alex Wickham (@WikiGuido) April 07, 2015

The inherent inequality of bargaining power between employers and workers and the reserve army of the unemployed must not be all that they are cracked up to be these days if low paid workers have to sign legally enforceable restraint of trade agreements, which is a common complaint about zero hours contracts. The worker does not have guaranteed hours but must promise not to work for someone else in the same line of business.

Obviously, the few members of the reserve army of the unemployed lucky enough to have a low pay, insecure job that offers no regular hours have so many other job options that their employers must get them to agree not to quit and job-hop at will. Jobs must be readily available to low paid workers for otherwise why do employers insist on this restraint of trade in employment agreements?

If there is an inherent inequality of bargaining power between the bosses and the workers, why do employers seek restraint of trade agreements against these downtrodden workers who are supposed to have few options but to accept the miserable zero hours job offer before them?

The question that must always be asked is why do people deemed competent to vote and drive cars sign zero hours contract? What is in it for them – for the worker who signs these contracts – especially for workers who already have a job and are switching to a zero hours contract? David Friedman asked this question about the economics of restraint of trade agreements for employees:

…the employer who insists on an employee signing a non- competition agreement will find that he must pay, in additional wages or other terms of employment, the cost that the agreement imposes upon the employee, as measured by the employee and revealed in his actions.

It follows that the employer will insist on such an agreement only if he believes that its value to him is greater than its cost to the employee… The contract is designed, after all, with the objective of getting the other party to sign it.

If I am designing the contract and offering it to many other parties, that may put me in a position to commit myself to insisting on terms that give me a large fraction of the benefit that the contract produces. But it is still in my interest to maximize the size of that net benefit-which I do by only insisting on terms that are worth at least as much to me as they cost the other party.

If zero hours contracts are as bad as the Left over Left claim, the job quit rates for these contracts should be high, and people moving from existing jobs should be under-represented in this section of the labour force. If a worker already has a job, they have few reasons to sign up to such a purportedly poor job offer. Show me the evidence.

Unless we have a good idea about why firms are moving to zero hours contracts, which we don’t, and why employees sign these contracts rather than work for other employers who offer more regular hours of work, meddling in these still novel to the officious observer arrangements is risky.

David Friedman on global warming, population and problems with the externality argument

02 Mar 2015 Leave a comment

in applied price theory, applied welfare economics, comparative institutional analysis, constitutional political economy, David Friedman, economic history, economics of information, economics of regulation, environmental economics, environmentalism, global warming, law and economics, population economics, property rights Tags: climate alarmism, competition as a discovery procedure, David Friedman, externalities, global warming, population bomb, The fatal conceit, The pretence to knowledge

Why all this sucking up to the dead Saudi dictator?

24 Jan 2015 Leave a comment

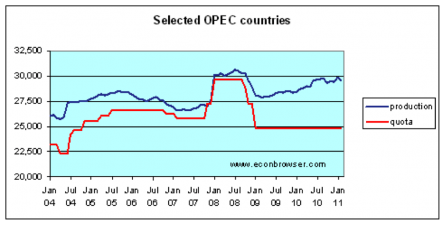

in energy economics, industrial organisation, politics - Australia, politics - USA, resource economics Tags: autocracy, autocratic succession, cartel theory, creative destruction, David Friedman, M. A. Adelman, Middle-East politics, OPEC oil cartel

We are not living in the 70s, but nonetheless the death of the late unlamented Saudi dictator has flags at half-mast and other sycophantic behaviour that hasn’t been seen since the death of the last totalitarian dictator who was something of a player in geopolitics and American foreign policy.

We are not living in the 70s where the West in fear of the OPEC cartel and the behaviour of Saudi Arabia as the swing producer and purported cartel enforcer.

/cdn0.vox-cdn.com/uploads/chorus_asset/file/2908448/oil_price_jan6.0.png)

OPEC and Saudi Arabia are both shadows of the former selves in terms of dominance in the global oil markets. OPEC as a whole represents about one third of global oil production, which was down for a little over 50% in 1973.

Within OPEC, Saudi Arabia As oil reserves that aren’t much bigger than those of either Iran or Venezuela. All of these countries, including Saudi Arabia have large populations and few other ways to servicing needs than from the oil revenues.

Russia is in the same position of needing to pump out as much oil as it can while letting someone else do the hard lifting regarding keeping the price of the oil up by cutting back production. US oil production has been on the rise, and has lessened the need for imported crude oil.

The best place to be in any cartel is outside the cartel selling as much as you can at the cartel price. The next best option is to be a cartel member, pretending to be a loyal while selling under the counter bias, much as you can. Recent discounts given by the Kingdom to some customers have been interpreted as showing a determination to maintain market share. David Friedman explains:

One great weakness of a cartel is that it is better to be out than in. A firm that is not a member is free to produce all it likes and sell it at or just below the cartel’s price.

The only reason for a firm to stay in the cartel and restrict its output is the fear that if it does not, the cartel will be weakened or destroyed and prices will fall.

A large firm may well believe that if it leaves the cartel, the remaining firms will give up; the cartel will collapse and the price will fall back to its competitive level.

But a relatively small firm may decide that its production increase will not be enough to lower prices significantly; even if the cartel threatens to disband if the small firm refuses to keep its output down, it is unlikely to carry out the threat.

Maurice Adelman regards the oil glut as the chronic condition of the world oil market, given the continuous tendency to underestimate reserves and undiscovered oil.

There was a glut 70 years ago, 50 years ago in 1933, 15 years ago in 1970 …But that condition of everlasting glut is periodically broken by dangers of oil shortage.

All cartels break-down and only some get back together. Cartels contain seeds of their own destruction. Cartel members are reducing their output below their existing potential production capacity, and once the market price increases, each member of the cartel has the capacity to raise output relatively easily. Adelman explains:

Opinions vary as to what is the right price for maximum profit, and opec has often had to find its right price through trial and error…

Each opec member could reap a windfall by cheating and producing over quota because the cost of production is so far below the market price. But, if some cartel members were to defect, output would climb and the prices — and windfall profits — would fall.

OPEC members pay scant regard to their actual production quotas and their national production quotas are always increased when push comes to shove. As Bill Allen said:

Long-term survival of the cartel has two fundamental requirements: first, cheating by a member on the stipulated prices, outputs and markets must be detectable; second, detected cheating must be adequately punishable without leading to a break-up of the cartel.

All cartels must decide how to allocate the reduction of output that follows the price increases across members with different costs structures and spare capacity.:

- The tendency is for cartel members to cheat on their production quotas, increasing supply to meet market demand and lowering their price.

- Most cartel agreements are unstable and at the slightest incentive they will quickly disband, and returning the market to competitive conditions.

The exercise of collective market power will not be stable unless sellers agree on prices and production shares; on how to divide the profits; on how to enforce the agreement; on how to deal with cheating; and on how to prevent new entry.

A cartel is in the unenviable position of having to satisfy everyone, for one dissatisfied producer can bring about the feared price competition and the disintegration of the cartel. Thus a successful cartel must follow a policy of continual compromise. Little wonder that John. S McGee wrote that:

The history of cartels is the history of double crossing.

Was it important to suck up to the Saudi dictator because of its role as swing producer in OPEC. In 1983, 1984, and 1986, for example, the Saudis produced only about 3.5 million barrels per day, despite their (then) production capacity of about 10 million barrels per day. Whatever else you can say about those production cutbacks to defend posted OPEC cartel price, they were a long time ago.

Saudi Arabia, Kuwait, and the United Arab Emirates have large reserves relative to the financial needs of their population but what they have is only a small share of global reserves and global production of oil and trivial share if you add global shale production.

With the exception of the wake of the 1979 Iranian upheaval, and market anticipation of a possible destruction of substantial reserves in the 1990–1991 and 2003 Gulf wars, real prices of crude oil fell from 1974 through 2003. Prices increased in 2004 onwards because of demand in Asia.

Bryan Caplan summarised the views of leading oil economist James Hamilton in 2008 as follows:

1. OPEC has almost no effect on world oil prices; most countries produce less than their quota, and when countries want to produce more, their quota goes up.

2. The price of oil follows a random walk. But the oil industry isn’t trying very hard to develop new sources because oil execs believe that the price of oil is mean-reverting (i.e., what goes up must come down). Why are the oil execs so wrong? Hamilton’s guess: They’re putting too much weight on their last big experience with high oil prices in the 70s and 80s.

No amount of cutting can support prices when supply outside OPEC is growing strongly and demand is weak in the wake of the global financial crisis and the slower recoveries both in the USA and Europe. Hamilton’s current view is that:

…of the observed 45% decline in the price of oil, 19 percentage points– more than 2/5– might be reflecting new indications of weakness in the global economy.

Whatever reason people are sucking up to the dead Saudi dictator, they have nothing to do with the global oil market.

Some economics of zero hours contracts – part 1: concepts, definitions and initial puzzles

21 Nov 2014 2 Comments

in labour economics, labour supply, managerial economics, occupational choice, organisational economics, personnel economics, survivor principle Tags: David Friedman, industrial organisation, inequality of bargaining power between employers and workers, labour economics, reserve army of the unemployed, Richard Epstein, Ronald Coase, zero hours contracts

Unions say New Zealand employers are following trends overseas and adopting zero hour contracts: workers have to be available for work, but have no hours guaranteed. Unite Union national director Mike Treen said:

McDonald’s, KFC, Pizza Hut, Starbucks, Burger King, Wendy’s – all of the contracts have no minimum hours, and so people can be – and are – rostered anywhere from three to 40 hours a week, or sometimes 60 hours a week, and it depends a lot on how you get on with your manager.

No official figures are available on the number of people on zero hour contracts in New Zealand, but they are are available in the UK in the chart below. About 250,000 workers in the UK work on zero hours contracts.

These workers agree not to work for anyone else, but are not promised regular work at all with their new employer.

The question that must always be asked is why do people who are deemed competent to vote and drive cars sign zero hours contract? What is in it for them? David Friedman asked this question about the economics of restraint of trade agreements for employees:

…the employer who insists on an employee signing a non- competition agreement will find that he must pay, in additional wages or other terms of employment, the cost that the agreement imposes upon the employee, as measured by the employee and revealed in his actions.

It follows that the employer will insist on such an agreement only if he believes that its value to him is greater than its cost to the employee…

The contract is designed, after all, with the objective of getting the other party to sign it.

If I am designing the contract and offering it to many other parties, that may put me in a position to commit myself to insisting on terms that give me a large fraction of the benefit that the contract produces.

But it is still in my interest to maximize the size of that net benefit-which I do by only insisting on terms that are worth at least as much to me as they cost the other party.

The inherent inequality of bargaining power between employers and workers and the reserve army of the unemployed must not be all that they are cracked up to be these days if low paid workers have to sign legally enforceable restraint of trade agreements.

Obviously, the few members of the reserve army of the unemployed lucky enough to have a low pay, insecure job that offers no regular hours today have so many other job options that their employers must get them to agree not to quit and job-hop at will. Jobs must be readily available to low paid workers for otherwise why do employers insist on this restraint of trade in employment agreements.

Why do workers sign these contracts, which can include a promise of exclusive services – not working for other employers? Several subsequent blog posts will attempt to answer this question

The inherent inequality of bargaining power between employers and workers doesn’t work too well here because the worker is accepting this job as compared to these other options , which may include employment in an existing job.

Once a worker is on-the-job and has accumulated job specific human capital, issues of post-contractual opportunism come up on both sides.

An important function of the employment contract is to prevent attempts to renegotiate terms and conditions once one side of the other has committed to the relationship and will find it costly to go elsewhere.

Zero hours contracts are negotiated upfront, which makes them unappealing to anyone already has a job, unless the terms and conditions of a zero hour contract, including the wages paid are much more appealing than officious observers make out.

Richard Epstein made this point about the general operation of the labour market, which is of relevance to our search to the answers to the questions posed by this blog post:

Labour markets are not characterized by tricky externalities. They do not pollute streams or require the creation of public goods. They are not characterized by genuine breakdowns in information, as workers are in a position to observe the conditions of their employment on a day-to-day basis.

Left to their own devices, without explicit support from union activities, they will be highly competitive, and thus work hard to allocate scarce human capital to its most productive use.

Workers have the option to quit for higher wages, and employers can always seek out low cost techniques to reduce their labour costs.

Any short-term dislocation for firms or individuals is more than offset by the overall increase in the system productivity, spurred in part by clear signals that should increase investments in human capital.

Zero hours contracts are a new labour market phenomena . That is no reason to automatically default to monopoly explanations for their emergence, including their emergence in a highly competitive industries and highly competitive labour markets where employees change jobs regularly.

As Coase said in the context of industrial organisation as a whole and novel business practices in particular:

One important result of this preoccupation with the monopoly problem is that if an economist finds something—a business practice of one sort or other—that he does not understand, he looks for a monopoly explanation. And as in this field we are very ignorant, the number of ununderstandable practices tends to be rather large, and the reliance on a monopoly explanation, frequent.

The next blog post arises out of my first exposure to the labour economics of working arrangements. Specifically, how the fixed costs of employment and the fixed cost of going to work both lead to minimum hours constraints in most employment contracts.

Most of what I know about the labour, personnel and organisational economics of working arrangements was about explaining why employers would expect an employee to work as a minimum number of hours if they were to employ them at all. Always good to start with explanations as to why zero hours should not exist, but they clearly do.

Subsequent blog posts will discuss zero hours contracts in the context of the team production and organisational architecture; and zero hours contracts, equalising differentials and job sorting.

David Friedman on the costs and benefits of prevention and adaptation to global warming

20 Nov 2014 Leave a comment

.@cgiarclimate Debate on climate change always neglect crucial role of CO2 in agriculture @ifadnews @careemergencies http://t.co/Y3Du5YnF56—

Golden Rice Now (@paulevans18) July 17, 2015

Armistice Day: World War I as a bar fight

11 Nov 2014 Leave a comment

in war and peace Tags: Armistice Day, David Friedman, game theory, Thomas Schelling, World War I

Wars are like bar fights. Both are about not backing down. David Friedman explains:

Consider a barroom quarrel that starts with two customers arguing about baseball teams and ends with one dead and the other standing there with a knife in his hand and a dazed expression on his face.

Seen from one standpoint, this is a clear example of irrational and therefore uneconomic behaviour; the killer regrets what he has done as soon as he does it, so he obviously cannot have acted to maximize his own welfare.

Seen from another standpoint, it is the working out of a rational commitment to irrational action–the equivalent, on a small scale, of a doomsday machine going off.

Suppose I am strong, fierce, and known to have a short temper with people who do not do what I want.

I benefit from that reputation; people are careful not to do things that offend me. Actually beating someone up is expensive; he may fight back, and I may get arrested for assault. But if my reputation is bad enough, I may not have to beat anyone up.

To maintain that reputation, I train myself to be short-tempered. I tell myself, and others, that I am a real he-man, and he-men don’t let other people push them around. I gradually expand my definition of “push me around” until it is equivalent to “don’t do what I want.”

We usually describe this as an aggressive personality, but it may make just as much sense to think of it as a deliberate strategy rationally adopted.

Once the strategy is in place, I am no longer free to choose the optimal response in each situation; I have invested too much in my own self-image to be able to back down… Not backing down once deterrence has failed may be irrational, but putting yourself in a situation where you cannot back down is not.

Most of the time I get my own way; once in a while I have to pay for it.

I have no monopoly on my strategy; there are other short-tempered people in the world. I get into a conversation in a bar. The other guy fails to show adequate deference to my opinions. I start pushing. He pushes back. When it is over, one of us is dead.

No-one could back down in 1914. Tom Schelling even said that once a country mobilised for war in 1914, it had no plans at hand on how to stop this mobilisation.

Schelling spent a lot of time on going to war as an emergent process: what a nation does today in a crisis affects what it can be expected to do tomorrow:

A government never knows just how committed it is to action until the occasion when its commitment is challenged.

Schelling argues that nations, like people, are continually engaged in demonstrations of resolve, tests of nerve, and explorations for understandings and many misunderstandings.

That is why there is a genuine risk of major war not from accidents in the military machine but through a diplomatic process of commitment and escalation that is itself unpredictable.

In Schelling’s view, many wars including World War 1 were products of mutual alarm and unpredictable tests of will.

Schelling and others in the 1950s and after studied World War 1 to learn how to not blunder into wars when nuclear weapons now would be used.

When people discuss the futility of World War 1, they under rate the role of unintended consequences and the dark side of human rationality in situations involving collective action.

Wars arise as unintended consequences of mutual alarm and unpredictable tests of will. As such, they are not moral ventures that you can choose to join or not. People blunder into wars.

It is even harder to get out of a war than into one. The problem is credible assurances that the peace is lasting rather than just a chance for the other side to rebuild and come back to attack from a stronger position.

A state would think that another state’s promise not to start another war is credible only if the other state would be better off by keeping such promises not to start another war than by breaking its promise once it has rearmed.

Making sure that Germany and its allies did not restart the war a few years later, fed and rested, is why the peace treaty in 1919 totally disarmed Germany and split-up the other Axis powers.

One side will think that the other’s promise not to re-start a war is credible only if the other state would be better off by keeping its promise not to re-start a war than by breaking its promise.

France fortified its border with Germany in the 1920s because of a lack of trust that the peace would endure. Germany was disarmed after 1918 so that the day which it would be a threat again was well into the future.

An understudied issue is peace feelers in World War 1 such as by the German chancellor in 1916 and the Reichstag peace resolution on 19 July 1917. Pope Benedict XV tried to mediate with his Peace Note of August 1917.

Peace initiatives failed because until the last months of the war, neither side really lost confidence that they could prevail over their opponents.

Both sides suffered from a profound sense of insecurity in an international system characterised by uncertainty, arms races, warfare, and constant intrigue.

Both sides assumed the worst of the other; both trusted in the reduction of their opponents’ military power to keep them safe. As long one side could believe that they had a plausible chance to prevail on the battlefield, they would not abandon their quest to achieve that goal.

From late 1914 to early 1917, the Allies thought the balance of power favoured them because they had access to greater resources than the Central Powers.

German peace feelers when they were winning were based on Germany keeping everything it had conquered up till then. When Germany was in retreat, the German peace feelers were based on going back to the old borders before the war.

With its armies in possession of enemy territory in both the east and west, and the Allies unable to push them out, German leaders saw no reason to offer extensive concessions for peace.

HT: Ross A. Kennedy,

Recent Comments