Milton Friedman on how New Keynesian Macroeconomics is mostly monetarism

06 Feb 2015 Leave a comment

Is Euroland an optimal currency area?

05 Feb 2015 Leave a comment

in currency unions, Euro crisis, global financial crisis (GFC), macroeconomics, monetary economics Tags: Euroland, optimal currency area

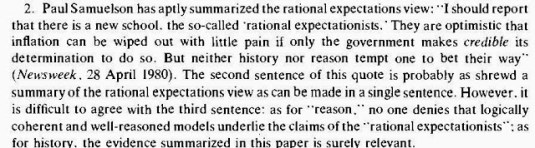

The shrewdest summary of rational expectations economic policy was by Paul Samuelson

02 Feb 2015 Leave a comment

in business cycles, fiscal policy, inflation targeting, macroeconomics, monetary economics Tags: new classical macroeconomics, Paul Samuelson, policy credibility, rational expectations, regime uncertainty, Stephen Williamson, time inconsistency, Tom Sargent

Deflation and Depression: Is There an Empirical Link?

31 Jan 2015 Leave a comment

in budget deficits, business cycles, economic growth, Euro crisis, great depression, great recession, macroeconomics, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: deflation, fiscal policy, liquidity traps, monetary policy, stabilisation policy

Deflation has a bad reputation. People blame deflation for causing the great depression in the 1930s. What worse reputation can you get as a self-respecting macroeconomic phenomena?

The inconvenient truth for this urban legend is empirical evidence of deflation leading to a depression is rather weak.

The most obvious is confounding evidence, is up until the great depression, deflation was commonplace. In the late 19th century, deflation coincided with strong growth, growth so strong that it was called the Industrial Revolution.

For deflation to be a depressing force, something must have happened in the lead up to the Great Depression to change the impact of deflation on economic growth.

Atkeson and Kehoe in the AER looked into the relationship between deflation and depressions and came up empty-handed.

Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

Deflation and Depression: Is There an Empirical Link?

Andrew Atkeson, and Patrick J. Kehoe, 2004.

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates. Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

View original post 1,842 more words

The success of monetarism and the death of the correlation between monetary growth and inflation

30 Jan 2015 1 Comment

in business cycles, econometerics, economics of bureaucracy, economics of information, inflation targeting, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: lags on monetary policy, Levis Kochin, monetary policy

Monetarists blame fluctuations in inflation on excessively volatile growth in monetary aggregates. In 1982, Friedman defined monetarism in an essay on defining monetarism as follows:

Like many other monetarists, I have concluded that the most important thing is to keep monetary policy from doing harm.

We believe that a steady rate of monetary growth would promote economic stability and that a moderate rate of monetary growth would prevent inflation

The U.S. data supported this hypothesis about the volatility of monetary growth and inflationuntil 1982, but since 1983 monetary aggregates have been essentially uncorrelated with subsequent inflation in the U.S.

Levis Kochin pointed out in 1979 that a well designed monetary policy would lead to zero correlation between any measure of monetary policy and subsequent inflation. The reason for this is the correlation between any variable and a constant is zero.

If monetary growth is stable, say, a constant growth rate of 4% per year, as advocated by Milton Friedman, monetary growth will have no correlations with any variable:

Poole (1993, 1994) and Tanner (1993) also argue that one predictable consequence of optimal monetary policy is that the correlation between monetary policy instruments and policy goals will be driven to zero.

Poole further contends that it is obvious to any careful reader of Theil (1964) that optimally variable policy will give rise to a zero correlation between policy and goal variable…

In 1966 Alan Walters, a U.K. monetarist, observed:

If the [monetary] authority was perfectly successful then we should observe variations in the rate of change of the stock of money but not variations in the rate of change of income… [a]ssuming that the authority’s objective is to stabilize the growth of income.

Milton Friedman in 2003, wrote about how the Fed acquired a good thermostat:

The contrast between the periods before and after the middle of the 1980s is remarkable.

Before, it is like a chart of the temperature in a room without a thermostat in a location with very variable climate; after, it is like the temperature in the same room but with a reasonably good though not perfect thermostat, and one that is set to a gradually declining temperature.

Sometime around 1985, the Fed appears to have acquired the thermostat that it had been seeking the whole of its life…

Prior to the 1980s, the Fed got into trouble because it generated wide fluctuations in monetary growth per unit of output. Far from promoting price stability, it was itself a major source of instability as Chart 1 illustrates.

Yet since the mid ’80s, it has managed to control the money supply in such a way as to offset changes not only in output but also in velocity.

Nick Rowe explained the difficulty of causation and correlation under different policy regimes and Milton Friedman’s thermostat superbly as an econometric problem Nick Rowe:

If a house has a good thermostat, we should observe a strong negative correlation between the amount of oil burned in the furnace (M), and the outside temperature (V).

But we should observe no correlation between the amount of oil burned in the furnace (M) and the inside temperature (P). And we should observe no correlation between the outside temperature (V) and the inside temperature (P).

An econometrician, observing the data, concludes that the amount of oil burned had no effect on the inside temperature. Neither did the outside temperature. The only effect of burning oil seemed to be that it reduced the outside temperature. An increase in M will cause a decline in V, and have no effect on P.

A second econometrician, observing the same data, concludes that causality runs in the opposite direction. The only effect of an increase in outside temperature is to reduce the amount of oil burned. An increase in V will cause a decline in M, and have no effect on P.

But both agree that M and V are irrelevant for P. They switch off the furnace, and stop wasting their money on oil.

Subsequent work of Levis Kochin showed that if the effects of fluctuations in monetary aggregates were not precisely known then the optimal policy would produce negative correlations between monetary aggregates and inflation:

The negative correlation results from coefficient uncertainty because the less certain we are about the size of a multiplier, the more cautious we should be in the application of the associated policy instrument.

Therefore, although optimal policy leads to lack of correlation between the goal and control variables if the coefficient is known, it will lead to a negative relationship if there is coefficient uncertainty. The higher the uncertainty, the more cautious will be the optimal policy response. Also, if the control variable can’t be controlled perfectly then the correlation between the goal and the control variable becomes positive i.e., the control errors are random…

Uncertainty about the impact of a policy will stay the hand of any bureaucrat , much less a central banker, as Kochin and his co-author explain:

Uncertainty should lead to less policy action by the policymakers. The less policymakers are informed about the relevant parameters, the less activist the policy should be. With poor information about the effects of policy, very active policy runs a higher danger of introducing unnecessary fluctuations in the economy.

The competing visions of stabilisation policy have been defined by Franco Modigliani and Milton Friedman

26 Jan 2015 Leave a comment

in business cycles, economics of information, history of economic thought, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Franco Modigliani, Keynes in macroeconomics, monetary policy, stabilisation policy, The fatal conceit, The pretence to knowledge

Paul Samuelson and Robert Lucas both agree that economists have solved the problem of economic depressions

24 Jan 2015 Leave a comment

in business cycles, fiscal policy, great depression, great recession, history of economic thought, macroeconomics, monetary economics, Robert E. Lucas Tags: Paul Samuelson, prosperity and depression, The fatal conceit, The pretence to knowledge

Milton Friedman on the lessons of the East Asian financial crisis (and Switzerland going off its peg)

24 Jan 2015 Leave a comment

What’s the difference between inflation and counterfeiting? The Portuguese banknote caper

21 Dec 2014 Leave a comment

in economics of crime, entrepreneurship, monetary economics Tags: Counterfeiting, fraud, swindles

Robert Barro recounts in his macroeconomics textbook a marvellous example where swindlers induced a British manufacturer of bank notes to print and deliver to them 3 million pounds’ worth of Portuguese escudos, which was equivalent to about 1% of Portugal’s nominal GDP in 1926.

This company, Waterlow and Sons Ltd. of London, also printed the legitimate notes for the Bank of Portugal. These bogus notes were,at first pass, indistinguishable from the real thing (except that the serial numbers were duplicates of those from a previous series of legitimate notes).

It was impossible to differentiate between the original and most of the duplicate banknotes because they were printed by the same printer using the same plates. 135,318 of the duplicate notes could be identified as part of the swindle because they were printed on plates not used for any other Portuguese banknotes. These bogus notes printed with the new plates could be differentiated from older legitimate banknotes because of a few marks that could be identified by an expert using a magnifying glass.

Central to the scam was taking advantage of the practice of the privately owned Bank of Portugal of secretly printing banknotes and neither recorded such transactions in the books, nor informing the government of the increase in the number of circulating banknotes.

(At the time, the Bank of England was also privately owned and only in 1921 had it obtained a monopoly on the issue banknotes in England and Wales. The Bank of Scotland still prints Scottish banknotes that are not legal tender in England. Three northern Irish banks still print banknotes that are legal tender in Northern Ireland. The entire northern Irish currency was withdrawn from circulation after a major bank robbery by the IRA a few years ago and replaced with new notes).

After the scheme unravelled, the Bank of Portugal made good on the fraudulent notes by exchanging them for newly printed, valid notes. The fraud may have contributed to the military coup, some six months later.

In the interim, by illegally increasing the monetary base and investing heavily in currency, land, building, and businesses, the swindlers created a boom in the Portuguese economy.

From the standpoint of monetary economics, I cannot think of a more unanticipated monetary shock. Of a surprise burst of monetary inflation and price inflation and led to the writing of books with titles such as The Man who Stole Portugal.

The final part of the swindle was to actually buy a controlling interest in the Bank of Portugal to validate the fraud by erasing all records that might inconvenience the swindlers.

The chief swindler with accomplices set up a bank of his own to facilitate fast distribution of the forged currency. A bank of their own was necessary because they had the modern equivalent of $150 billion to launder.

This Bank of Angola & Metropole set up to launder the bogus notes was also the initial place of suspicion of something fishy going on because it grew so quickly, while taking no deposits. Germans are also involved with this bank. Germany was suspected by the Portuguese government to have ambitions to take over Portuguese Angola, so this attracted additional attention from the authorities.

The chief swindler, Alves Reis, was depicted in a 50-episode TV series in 2000 as well as several books about the fraud over the decades.

At the time of the swindle, Reis was 28 years old engineering dropout from an undistinguished middle-class Lisbon family. He already had a conviction for cheque fraud. As such, one of the greatest swindles of all time was pulled off by a petty conman.

The swindle unravelled because of the duplicate banknote serial numbers, which was an error the swindler made himself. But for that, the swindle would have been immensely difficult to uncover. The swindlers duplicated the existing serial numbers and hoped they were able to successfully release all the banknotes before they were caught.

Reis, the architect of the swindle, work out the sequence of bank governor names and serial numbers used by the Portuguese central bank, but had neglected to eliminate numbers already ordered.

When the British printer realised this, Reis convinced the London firm that the reuse of existing serial numbers for their purported place of circulation in the Portuguese colony of Angola was not a cause for alarm. Fortunately for the swindlers, a letter from the British printers to the Banco de Portugal, in that he spoke about the agreements to print the banknotes for distribution in Angola went missing in the post.

The Bank of Portugal was not supposed to issue its currency in Angola, but often did circulate its currency in Angola.

This was a clever part of the swindle. By pretending that the Bank of Portugal was doing something slightly dodgy but still standard practice, and thus had to do so in secrecy, the swindlers could induce a whole range of other more legitimate people than them to cooperate quietly with what they were doing.

The shady nature of these dealings to surreptitious circulate Bank of Portugal banknotes in Angola stamped with “Angola” was passed over by the British dupes to the swindle as another example of the corruption of Portuguese officials. The stamp “Angola” was so they wouldn’t be confused with notes from the mother country.

In addition, bank notes for the Portuguese colonies were printed at the time by a competitor. The British printer saw this on the quiet contract as an opportunity to take away some of their trade.

The swindlers said that they would take care of stamping “Angola” on the banknotes once they were delivered to them. The swindlers had accomplices in the Portuguese diplomatic service, who issued them with fake diplomatic passports, which was helpful in persuading the British printers to deliver the bogus banknotes personally to them. Consignments were delivered to the swindlers in February, March and November 1925.

the basis of the scam was forging a contract in the name of Banco de Portugal authorising Reis to print banknotes in return for an alleged loan from a consortium to develop Angola. The whole affair had to be kept secret lest Angola fall into further financial difficulties due to rumours of a pending economic ruin.

The London based specialty printer worked, for among other clients, for the English court system and printed the transcripts of its own trial! This printer tried to have the trial postponed for a year while its chief executive completed his one-year term as Lord Mayor of London to save embarrassment.

The British printing company was found liable in subsequent four years of litigation, but the key question for the court was the amount of damages.

- The Bank argued that the damages were £1 million (less funds collected from the swindlers).

- The British printer duped by the swindlers argued was that the only true costs to the Bank were the expenses for paper and printing of the replacement notes.

The House of Lords determined in 1932 that £610,000 was the correct measure. This award of damages was the £1 million less the funds recovered from the swindlers

The proper measure of damages, in the view of the majority of the Law Lords, was the face value expressed in sterling of the genuine currency given in exchange for the spurious notes.

As these damages would be paid initially in British pounds, this damages award was a real windfall for the Bank of Portugal. Worthless Portuguese banknotes exchanged for good British pounds that could buy imports.

The majority decision of the Law Lords was the correct measure of damages because that is what the bank had to outlay to make itself whole again after the breach of contract. The chief swindler got 20 years.

One of the two Law Lords in dissent had another view of the proper measure of damages:

The judgment of Wright J. should be set aside and judgment entered for the Bank for the sum of £8,922

This law lord and an appeal court justice held this view because the swindle cost the Bank of Portugal nothing bar printing costs to replace the spurious banknotes, which were widely accepted as valid currency in a cash economy.

The Bank of Portugal could issue banknotes in any number at little cost to itself up to the limit provided by Portuguese law. Ropke wrote that:

The English courts presently discovered that the case involved issues of unusual subtlety and complexity, adjudication of which necessitated the admission of testimony by leading monetary theorists.

The question before the courts was: how great were the actual losses incurred by the Bank of Portugal?

If it had been postage stamps instead of bank notes in which the swindlers had trafficked, it is perfectly clear that the loss of the Portuguese government would have equalled the total value of the stamps.

With respect to the bank notes, however, no such simple calculation could be made.

Among the many questions which troubled the experts the following stand out as particularly relevant to our study: would the Bank of Portugal have issued the same amount of notes even if the swindlers had not done so?

If not, was the increase in the supply of money resulting from the introduction of the fraudulent notes good or bad for Portugal?

No one disputes, as several of the Law Lords noted, that the theft of a postage stamp must be made good at face value. People hesitate in this case involving swindling access to banknote plates and printing currency for yourself because what exactly was stolen?

When Reis died in 1955 , The Economist said of the counterfeiting scheme:

The perpetrators, however reprehensible their motives, did Portugal a very good turn according to the best Keynesian principles.

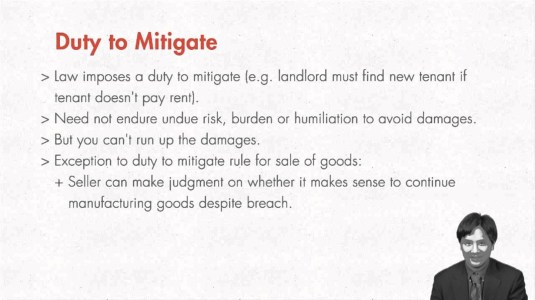

The House of Lords case is a major British legal precedent regarding the duty of the wronged party to mitigate damages in the case of breach of contract.

The House of Lords held that this duty did not apply if it would give your business a bad name in the trade. The Bank of Portugal could have repudiated the duplicate banknotes rather than exchange them for genuine new notes, but chose not to do so because this repudiation of banknotes would have ruined what little reputation it had.

The House of Lords also upheld the right of the wronged party to choose between different methods to mitigate damages from the breach of contract.

Interview with Robert Lucas on the global financial crisis and the great recession

17 Dec 2014 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, monetarism, monetary economics Tags: bank runs, GFC, great depression, great recession, Robert E. Lucas

Milton Friedman’s plucking model of the business cycle

15 Dec 2014 Leave a comment

in macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Austrian business cycle theory, Austrian macroeconomics, business cycle asymmetry, Milton Friedman, plucking model, Roger Garrison

Friedman (1993) proposed a model of the depth of recessions and steepness of recoveries built on two empirical regularities:

- output is on average below a ceiling defined by supply capacity and tends back to this ceiling; and

- large contractions are followed by large expansions and mild contractions are followed by mild expansions.

The strength of a recovery should be positively correlated with depth of the recession but there should be no correlation between expansions and recessions (Friedman 1993; Alchian 1969).

Figure 1 illustrates Friedman’s model, which likens the time path of output to a string on the underside of an upward sloping board that is plucked downward at random intervals to various extents into busts that are followed by booms.

Figure 1: Friedman’s plucking model of the economic fluctuations

Source: Garrison (1996).

The upward sloping board plotted as a thick line in Figure 6 represents a ceiling on feasible output and employment in a given year that is set by resource and technology availabilities. The upward slope of this board accounts for trend real GDP growth over time due to technological progress and other factors.

Output is close to the ceiling shown in Figure 6 except for every now and then when it is plucked downwards by a monetary contraction.

There is no floor on these contractions in output to moderate the depth and violence of contractions, so some recessions are deep and sharp (Hansen and Prescott 2005; Friedman 1993; Goodwin and Sweeney 1993; Sichel 1993).

Contraction depth can vary greatly as is shown by the minor, mild and deep recessions in Figure 1. In each episode of plucking illustrated in Friedman’s model in Figure 1, the rebound mirrors the previous fall in output, but the recovery cannot go beyond the ceiling.

Friedman’s model is a bust-boom model of business cycle fluctuations. The business cycle starts with a bust caused by an adverse policy or other shock and is then followed by a boom as the market self-adjusts and the policy errors are reversed.

Without the initial adverse policy or other shock, there would neither be a bust nor a boom. The economy would track close to the ceiling on output and employment as is shown in Figure 1 by the periods between the plucks.

The correlation between busts and booms arises from the monetary contraction that caused the bust eventually inducing an offsetting correction in monetary policy.

The monetary contraction that pushed or plucked output below the upward sloping ceiling is later followed by a monetary expansion that offset the earlier contraction.

With the amplitude of monetary expansions correlated to offset the prior contractions, GDP growth will have similar plucks or falls and rebounds to the upward sloping output ceiling because of the link albeit with a lag between monetary growth and output fluctuations.

The increases and decreases in monetary growth are independent policy choices with unique causes.

The associated upward and downward movements in GDP growth are not correlated with each other but should be correlated with the prior fluctuations in monetary growth.

There would not be a bust and later boom if there is no monetary contraction to start the cycle. This is why Friedman (1993) proposed that the depths of busts are unrelated to duration and strength of prior economic booms. This upset Austrians such as Roger Garrison:

…Austrians work at a lower level of aggregation in order to allow for the outputs of the two sectors to move relative to one another and even to allow for differential movements within the investment-goods sector…

During a credit-induced boom, investment in the relatively high stages of production is excessive in that resources are drawn away (by an artificially low rate of interest) from the relatively low stages of production and from the final stage, consumption.

The decrease in the amount of resources allocated to the low and final stages is forced saving; the misallocation of resources from low to high stages is malinvestment.

Empirically, a credit-induced boom would be but weakly reflected in the conventional investment aggregate and hardly at all in the Monetarists’ output aggregate, which includes consumption.

The boom for the Austrians refers to something going on largely within the output aggregate.

It is represented in Friedman’s plucking model not by a conspicuous recovery to trend but rather by some period preceding a pluck which Friedman, operating at a higher level of aggregation, presumes to be healthy growth.

The publication of Milton Friedman’s paper in 1993, which recalled an obscure paper he wrote in 1964, lead to a large literature blossoming under the heading business cycle asymmetry.

Milton Friedman – Abolish The Fed

13 Dec 2014 Leave a comment

in macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Milton Friedman, The Fed

Recent Comments