05 Aug 2015

by Jim Rose

in currency unions, economic growth, economic history, economics of regulation, Euro crisis, fiscal policy

Tags: British disease, British economy, Eurosclerosis, France, Germany, Italy, sick man of Europe, Sweden, Swedosclerosis

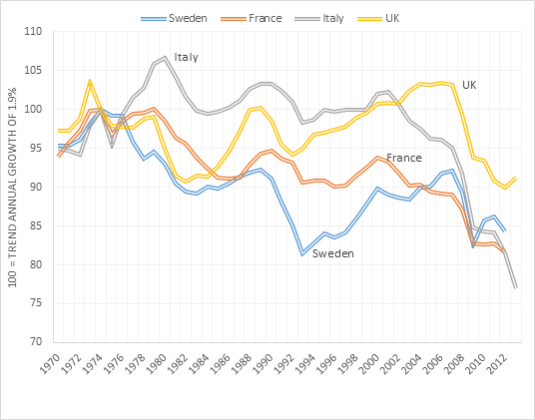

Figure 1 shows stark differences between Sweden, France, Italy and the UK since 1970 in departures from trend growth rates of 1.9% in real GDP per working age person, PPP. Italy did quite OK until 2000 growing at about the trend growth rate of 1.9% after which it fell into a hole so deep that it barely notice the onset of the global financial crisis. Sweden really had been the sick man of Europe until it turned its back on high taxing, welfare state socialism in the early 1990s. France has been in a long decline so much so that the global financial crisis is hard to pick up in the acceleration in its long decline in the mid-1990s. Figure 1 also shows Britain did very well, both under the neoliberal horrors of Thatcherism and the betrayals by Tony Blair of a true Labour Party platform. The UK grew at above the trend annual growth to 1.9% for most of the period from the early 1980s to 2007. The UK has done not so well since the onset of the global financial crisis.

Figure 1: Real GDP per Swede, French, British and Italian aged 15-64, 2014 US$ (converted to 2014 price level with updated 2011 PPPs), 1.9 per cent detrended, 1970-2013

Source: Computed from OECD StatExtract and The Conference Board. 2015. The Conference Board Total Economy Database™, May 2015, http://www.conference-board.org/data/economydatabase/

Note: When the line is flat, the economy is growing at its trend annual growth rate. A falling line means below trend annual growth; a rising line means of above trend annual growth. Detrended with values used by Edward Prescott.

German data was not in figure 1 because German unification threw all of its data into disarray for long-term comparison purposes.

03 Aug 2015

by Jim Rose

in budget deficits, business cycles, currency unions, economic growth, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, great recession, history of economic thought, law and economics, macroeconomics, monetary economics

Tags: bank panics, bank runs, banking crises, currency crises, Thomas Sargent

02 Aug 2015

by Jim Rose

in budget deficits, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great recession, history of economic thought, macroeconomics, monetarism, monetary economics

Tags: Brad Delong, fiscal multiplier, fiscal stimulus, Larry Summers, New Keynesian macroeconomics, Thomas Sargent

01 Aug 2015

by Jim Rose

in inflation targeting, macroeconomics, monetary economics, politics - New Zealand

Tags: central banking, forecasting errors, The fatal conceit, The pretence to knowledge

Anyone who had a good idea about what the the New Zealand dollar should be would be trading on their own account. These super-rich would not be wasting their time giving advice to others. Their time would be too handsomely rewarded for such meagre returns as pontificating to others as to what they should do with their portfolios.

https://twitter.com/JimRose69872629/status/626597273007296514

One of my delights as a bureaucrat was at a meeting between the Reserve Bank of New Zealand and the International Monetary Fund some 15 years or so ago

The Fund asked whether Bank whether it thought the exchange rate was too high, and what their exchange-rate modelling say about this?

- The reply of the Deputy Governor of the Reserve Bank of New Zealand was we don’t have exchange rate model because we don’t think there are any good. Gone are those days.

- The International Monetary Fund team was quite flabbergasted by this response.

At one stage the Fund team tried to draw me into the conversation about the level of New Zealand dollar because I was there representing the New Zealand Treasury. I was only attended as an observer, so naturally my response to their questions was to waffle incoherently. I could have been blunter and simply said the Reserve Bank of New Zealand spoke for New Zealand in this matter, but that would have been impolite.

croaking cassandra

croaking cassandra

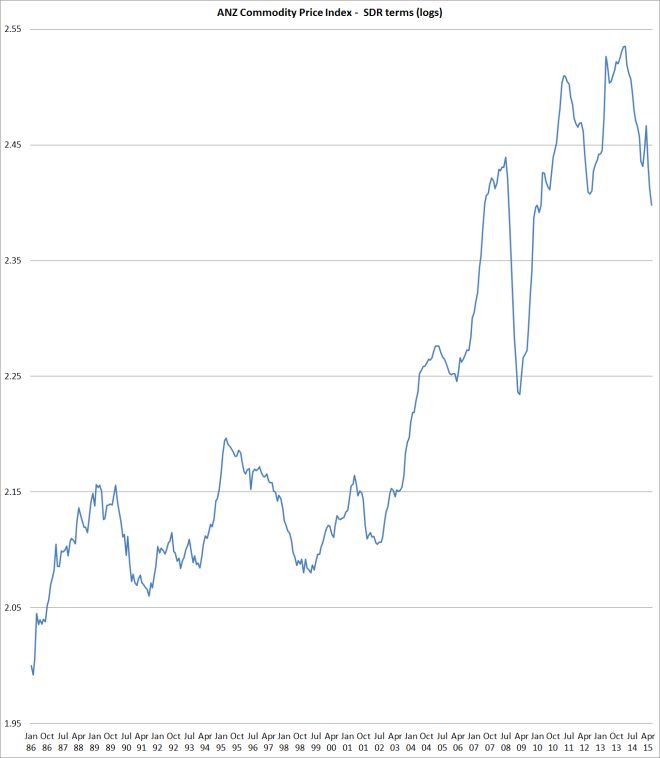

I’ve been continuing to reflect on Graeme Wheeler’s repeated observation that New Zealand’s exchange rate “needs” to come down. I’m still not entirely sure what he means. The exchange rate is an asset price and presumably should reflect all expected future relevant information, not just spot information about current dairy prices. And the market has no particular reason to focus on stabilising the net international investment position at around current levels. Indeed, although it is a convenient reference point, neither does the Reserve Bank.

“Need” or not, I’d have thought it was likely that the exchange rate would fall further.

The ANZ Commodity Price Index, which lags behind (for example) falling GDT and futures dairy prices, has already had one of the larger falls in the history of the series.

Meanwhile, the fall in the exchange rate, while material, remains pretty small by the standards of past New Zealand adjustments…

View original post 165 more words

31 Jul 2015

by Jim Rose

in currency unions, economic growth, Euro crisis, international economics, macroeconomics

Tags: British economy, customs unions, EU, EU membership, free trade areas, international economic integration, preferential trading agreements, regional integration

30 Jul 2015

by Jim Rose

in business cycles, currency unions, economic growth, Euro crisis, job search and matching, labour economics, labour supply, macroeconomics, unemployment

Tags: employment law, employment regulation, EU, Euro sclerosis, Euroland, Eurosclerosis, Japan, labour market regulation

29 Jul 2015

by Jim Rose

in economic history, job search and matching, labour economics, labour supply, law and economics, minimum wage, politics - Australia, politics - New Zealand, politics - USA, unions

Tags: Australia, British economy, employment law, employment law regulation

Major deregulations and re-regulations of the labour market in Australia and New Zealand did not move the employment protection inducts around that much in figure 1. All is been quiet on the labour market regulation front of the UK pretty much since the index was started.

Figure 1: OECD employment protection index (EPI), strictness of employment protection – individual and collective dismissals, USA, UK, Australia and New Zealand, 1990 – 2013

Source: OECD StatExtract.

The Work Choices legislation in Australia in 2006 was looked upon by the OECD as a somewhat minor deregulation not much more in scale than the deregulation introduced in 2008 with the election of the National Party led government.

Nobody told the unions that.

29 Jul 2015

by Jim Rose

in macroeconomics, politics - New Zealand

Tags: central banks, forecasting errors, monetary policy, The pretence to knowledge

I don’t place much weight on criticisms of forecasting errors. If someone is any good at forecasting the economy, they would be fabulously rich through trading on their own account rather than working in a central bank.

The fact that Reserve Banks can’t forecast with any greater accuracy than anybody else is a bit of an indictment considering they have inside knowledge of the future course of monetary policy.

By the way, I wrote my masters sub thesis on official forecasting errors.

croaking cassandra

Plenty of commentaries have remarked on the very low inflation numbers out this morning.

None (that I have seen) has highlighted what a severe commentary these numbers are on the Reserve Bank’s conduct of monetary policy over the last few years.

Reciting the history in numbers gets a little repetitive, but:

• December 2009 was the last time the sectoral factor model measure of core inflation was at or above the target midpoint (2 per cent)

• Annual non-tradables inflation has been lower than at present only briefly, in 2001, when the inflation target itself was 0.5 percentage points lower than it is now.

• Non-tradables inflation is only as high as it is because of the large contribution being made by tobacco tax increases (which aren’t “inflation” in any meaningful sense).

• Even with the rebound in petrol prices, CPI inflation ex tobacco was -0.1 over the last year…

View original post 1,600 more words

28 Jul 2015

by Jim Rose

in Euro crisis, job search and matching, labour economics, law and economics, macroeconomics

Tags: British economy, employment law, employment law regulation, Eurosclerosis, France, Germany, Greece, Italy, Portugal, Spain

Much easier to fire someone in the USA or UK than on continental Europe. Greece and Spain aren’t that bad by continental European standards for employment law protections against dismissals of individuals.

Figure 1: Strictness of employment protection for individual dismissals, 2013

Source: OECD StatExtract.

27 Jul 2015

by Jim Rose

in currency unions, economic history, Euro crisis, fiscal policy, labour economics, labour supply

Tags: ageing society, demographics crisis, economics of retirement, female labour force participation, Greece, Italy, male labour force participation, old age pensions, older workers, Portugal, social insurance, Social Security, Spain, taxation and labour supply

Figure 1 shows a relatively distinct pattern for men in the PIGs. Portugal aside, there has been a long decline retirement ages. This is different to the Anglo-Saxon countries where effective retirement ages have been increasing in recent years for men.

Figure 1: average effective retirement age (5-year averages), men, Portugal, Italy, Greece and Spain, 1970 – 2012

Source: OECD Pensions at a Glance.

Figure 2 shows that apart from Greece, that after a long decline in female effective retirement ages, there was something the rebound, especially in Italy and Portugal. In Greece, the rebound was in the 80s, followed by a resumption of decline from the mid 90s.

Figure 2: average effective retirement age (5-year averages), women, Portugal, Italy, Greece and Spain, 1970 – 2012

Source: OECD Pensions at a Glance.

Previous Older Entries Next Newer Entries

Recent Comments